The number of shares traded in a day is an

important criterion for investing in a stock. This is because good liquidity can make it easy for an investor to sell whenever he wants to.

However, some fund managers take a contrarian call on this. They buy a few illiquid stocks in the belief that these are gems whose value the market will discover in due time, giving them stellar returns.

Stock exchanges release a list of illiquid stocks every quarter based on criteria decided by them and the market regulator. The latest list, for the September quarter, mentions 38 stocks that are held by mutual funds.

"Fund managers are least bothered about liquidity as they are long-terms investors," says SP Tulsiyan, an independent research analyst.

According to the list, mutual funds held illiquid securities worth Rs 1,582 crore on November 3, 0.2 per cent of the industry's assets under management of Rs 7,47,332 crore.

These stocks, most of which are not

tracked by brokerage houses due to low public float, may turn out to be multi-baggers in the coming years.

"Many such illiquid stocks are of companies with high promoter holding. A few also belong to multinational companies. The financial performance of these companies is not bad. The stocks are illiquid just because of low public holding," says Tulsiyan. Experts say many of these companies are also delisting candidates.

Out of 38 stocks held by mutual funds that are hardly traded, Sanofi is the number one, with mutual funds investing as much as Rs 563 crore in it, followed by Vardhaman Textiles (Rs 305 crore) and Wabco India (Rs 270 crore).

LOW VOLUMES, HIGH INTERESTIn nine out of the 38 stocks, the amount invested by the funds is more than Rs 25 crore. Let's see if they are worthy of your money, say experts.

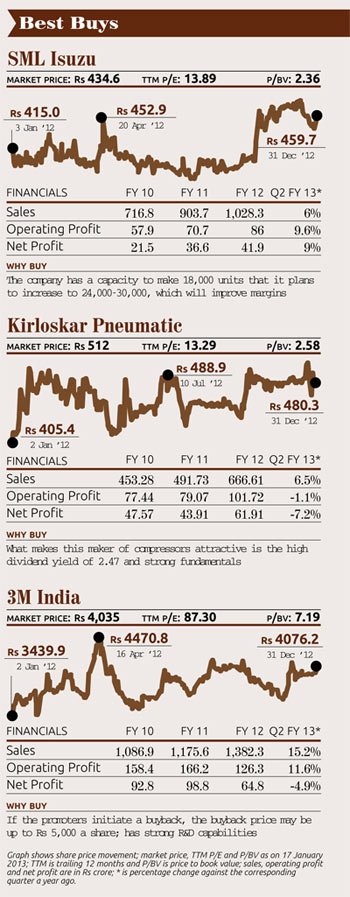

SML Isuzu:Sumitomo Corporation and Isuzu Motors hold a 54.96 per cent stake in the commercial vehicle maker, formerly known as Swaraj Mazda. Isuzu, the largest commercial vehicle maker in Japan with a strong global presence, raised its stake in SML Isuzu by over 5 per cent around May.

"There has been a lack of clear leadership and guidance at the top level and that's why the company has been languishing," says Kartik Mehta, assistant vice president, research, Sushil Financial Services.

Mehta has a target of Rs 472 for the stock. On December 26, it was at Rs 448. It's a good and compact company, he says. The company has a capacity to make 18,000 units that it plans to increase to 24,000-30,000 units, which will improve margins considerably, says Mehta.

The company has a good record of paying dividends. The stock can be bought at Rs 400-420, says Mehta.

Kirloskar Pneumatic:What makes this maker of compressors attractive is the dividend yield of 2.47. Dividend yield shows how much a company pays as dividend every year relative to its stock price. The stock rose 16 per cent in the first 11 months of 2012. The company posted a net profit of Rs 61.9 crore in 2011-12, 40 per cent more than Rs 43.91 crore in 2010-11.

"The fundamentals are good. Net sales and profit after tax are expected to grow at 20 per cent a year. It's a debtfree company with high promoter holding. About 20 per cent stake is held by institutions, leading to low public float. It's worth a buy at every decline. We expect the stock to reach Rs 700 in the long run," says Sunil Pachisia, vice president, Pratibhuti Viniyog, a brokerage that caters to institutional investors. It was at Rs 492 on December 26.

3M India:The technology company caters to health care, oil & gas, construction, safety and retail industries. It has invested a lot in research & development (R&D) centres. While it has not been paying dividends regularly, its major attraction is the shareholding pattern. About 76 per cent is held by the parent, 3M Company, and 14.7 per cent by institutional investors and corporate bodies. The remaining 10 per cent is with individual shareholders, trusts and non-resident Indians. The company, say experts, is a perfect delisting candidate as the parent wants to increase its stake.

"If they initiate a buyback, the buyback price may be up to Rs 5,000 a share," says Tulsiyan. It's a good bet for the long term but not for investors who want very good gains in a year or two.

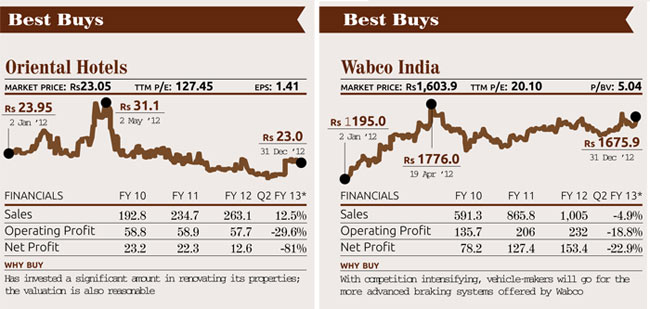

Oriental Hotels:Part of Taj Hotels and Resorts, Oriental Hotels operates in the southern region of India. The company may face challenges in the short term due to low demand but the stock can give good returns if one keeps it for long, say experts. This is because it has invested a significant amount in renovating its properties. The stock has languished this year and is available at a good valuation. Retail investors with a horizon of more than three-four years can buy it current levels, say experts.

Kirloskar Industries:Held by funds under schemes such as Principal Dividend Yield, Reliance Equity Opportunities Fund and UTI Infrastructure Fund, the company has been posting good growth in bottom line over the past three years. The company, which runs seven windmills in Maharashtra, has been paying dividends regularly.

"It has made a substantial investment in windmill projects. So, one must have a very long perspective for investing in this stock. It is not advised for retail investors," says Pachisia of Pratibhuti Viniyog.

Maharashtra Seamless:Mutual funds and institutional investors had invested over Rs 135 crore in this Jindal group company as on November 3. The largest manufacturer of seamless pipes and tubes in India has a robust business model, say market experts.

"Maharashtra Seamless is an industry leader with 37-42 per cent share of the seamless pipe market. The management has invested a significant amount in R&D and increasing presence in South America and Canada. It is aiming to earn 30 per cent revenue from exports compared to 10 per cent at present. Also, the company has a debt of just Rs 20 crore, which gives it space to expand," says Soumyadip Raha, an analyst at Kolkata-based research firm Microsec Securities.

Raha has set a target of Rs 433 for the stock. It was at Rs 280 on December 26. The company will be the biggest beneficiary of pickup in the infrastructure sector. Another indication of growth prospects is the recent orders bagged by BHEL, its biggest client.

"This may translate into some orders for the company as well," says Raha.

Wabco India:The unit of Clayton Dewandre Holdings is a market leader in airbrake systems for medium and heavy commercial vehicles. It commands an 85 per cent share of the braking applications market and has been able to clock over 18 per cent compounded annual growth between 2007-08 and 2011-12. It has many products that it has not yet started offering to Indian automobile makers. However, with competition in the commercial vehicle segment intensifying, many manufacturers are looking to offer more advanced products, which is likely to improve the demand for Wabco's offerings. The government is also putting a thrust on vehicle safety by making it mandatory for school buses and commercial vehicles carrying hazardous goods to have anti-lock braking systems.

"The company is technically sound with its parent being a global leader in braking applications. There has been a focus on emerging markets as the US and European markets are maturing. The only way to grow revenue and profitability is to turn to emerging markets such as India and China," says Mehta of Sushil Financial Services.

The company looks a good investment bet as more and more vehicle makers adopt more advanced technologies. "Wabco is a preferred vendor to Daimler for braking and control systems and will be one of the biggest beneficiaries of Daimler's move to start operations in India from 2013-14," says Pachisia.

However, while it's a long-term story yet to be played out fully, the stock can be bought on dips, with Rs 1,400 being a good entry point, says Mehta. It was at Rs 1,695 on December 13.

Sanofi India:The pharmaceutical company is the most preferred by mutual funds, which had invested Rs 563 crore in it as on November 3. The company is debt-free and has good cash reserves. The promoters hold 60.4 per cent while 27.7 per cent is owned by institutional investors and 6 per cent by corporate bodies. "The company is aggressive, as seen by recent acquisition of brands. It also plans to enter the animal health-care business," says Pachisia of Pratibhuti Viniyog.

"We expect the company's net sales to log 17 per cent compounded annual growth between 2011 and 2013, driven by the domestic formulation business. We expect net sales to post 17 per cent compounded annual growth to Rs 1,682 crore and earnings per share to register 12 per cent compounded annual growth to Rs 104.4 between 2011 and 2013," says Sarabjit Nangra, vice president, research, Angel Broking. She says the stock is expensive at current levels. However, experts say that any 5-10 per cent correction is a good entry point for long-term investors.

Vardhman Textiles:The largest spinning company in India has 22 manufacturing facilities. It makes fibre, yarn, sewing thread and fabrics. Promoters hold over 61 per cent while domestic institutional investors hold nearly 23 per cent in the company. One reason experts prefer Vardhman is that there are not many spinning companies in India that are listed. Also, spinning companies have been doing well of late due to fall in cotton prices and good demand in both export and domestic markets.

However, it faces threats from the policies of Gujarat and Maharashtra governments, which offer power subsidy and tax incentives for the industry, and excess capacity.

"The company plans heavy capital expenditure in a year. So, investors with a long horizon can lock into the stock at Rs 220-225 levels compared with the current level of around Rs 250," says Pachisia.