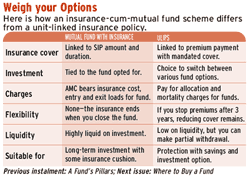

However, investors need to know if this combo pack works for them, and if it does, how it benefits them. The doubt is understandable, especially when insurers are offering products—unit-linked insurance plans (Ulips)—that provide a similar benefit. So which one should a customer opt for?

By default, insurance products are for protection and are long-term in nature, whereas equity mutual fund schemes range from medium- to long-term and are purely for investment and growth. SIPs provide cost averaging over market cycles, making them work the best over long tenures. It is for this reason that a SIP backed by an insurance cover comes with a high exit charge (if one were to exit it early), making it more expensive than a plain equity fund.

If you miss paying even one SIP, you will lose your insurance cover. The basic cover has a cap because the cost is borne by the AMC. In principle, it works on a group insurance format, where the risk is spread across all unitholders (under the fund) who opt for the insurance.

This combo product is more beneficial for those who want to have a relatively less cover due to an income limitation. Hence, one can get insurance by not paying any extra amount. In this option, the mutual funds offer cover for the unpaid instalments of an SIP.

If the term of an SIP is 10 years and if the investor dies after three years, then the unpaid SIP for seven years is covered. The risk cover ends as soon as the SIP stops or any withdrawal is made from the investment. Usually, funds offer a cover through the tenure of the SIP, provided at least three years of instalments have been paid. The cover reduces from the original value to the fund value of the SIP instalments paid.

Though these funds seem tempting, do not invest in them merely to reduce your insurance needs or at the cost of your financial goals.