A guide to mutual fund investing that will help you avoid common mistakes and ensure consistent wealth creation.

WHAT ARE MUTUAL FUNDS?

A mutual fund is an investment scheme, wherein several people can put their money in a variety of options like stocks, bonds or securities and other instruments. Unlike most options, mutual funds have lower entry barriers.

Why invest in them

When you invest in a mutual fund, you’re pooling money along with other people. This enables a variety of investments at a relatively low cost. Another advantage is that a professional manager takes the decisions for you about specific investments. Mutual funds are widely available through banks, financial planners, brokerage firms and other investment firms. You can buy or sell funds at any time, which offers convenience, flexibility and liquidity. The biggest advantage is asset diversification. Not all investments perform equally well at a given time as they react differently to world events, economic factors and business prospects. So when one investment is down, another could be up. Having several investments offsets the impact of poor performers and offers the benefit of the earning potential of the rest.

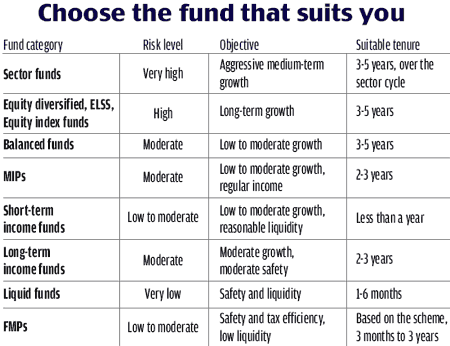

How to pick the right fund

Today, investors are spoilt for choice as the market offers a plethora of funds. The variety often makes it difficult for them to select a fund that suits their needs. To help pick the right fund, consider these three steps:

Step 1: Decide your investment objective and risk profile

The investment objectives of the fund should coincide with those of the investor. These include tax planning, regular income, high returns and long-term planning, like children’s education. While equity funds are more tax-efficient compared with debt funds, short-term debt funds aim at regular income, whereas closed-ended equity funds aim at long-term capital appreciation. The fund should also meet the investor’s risk tolerance level.

Step 2: Fund performance and management

Though a fund’s past performance does not define its future, it’s important to study it with respect to its benchmark or with similar funds. The comparison should be with the same category of funds. The fund’s past performance also helps assess the quality of fund management and the skills of the fund manager. His stock-picking ability and market timing can be judged by comparing the fund’s performance with its chosen benchmark.

Step 3: Fund costs and loads

The operating cost of running a fund includes marketing and selling expenses, audit fees, custodian fees, etc. These can be gauged from the expense ratio, which is reported in the fund’s annual report and should be compared with similar funds. Other important factors are the entry and exit loads, which are charged to recover the commissions of agents and distributors. The loads are deducted from the NAV of the scheme, which reduces the number of units for the investor. The investor should compare the loads among similar funds.

WHAT IS AN SIP?

We all know that we need to invest regularly in order to set aside a portion of our earnings for future needs like buying a house or car, children’s education and marriages, and our own retirement. Unfortunately, most of us end up making sporadic investments, which help little in achieving our financial goals. When it comes to investing in the stock market, we often wait to collect a large amount of money so that we can invest it at one go. However, recurring household expenses erode the money we would have saved for investments and the result is that we end up compromising on our financial goals.

Systematic Investment Plan (SIP) is a financial planning tool which helps invest in the stock markets through small, periodic instalments. For instance, you can invest as little as Rs 100 on a monthly basis. Moreover, you can select the tenure of your instalments. SIPs help you set aside a fixed amount every month for investments, thus contributing towards your financial goals.

Why go for SIPs

Equity markets are inherently volatile and move up and down due to a combination of factors, which include government policies, corporate profits, global markets and interest rates. The investors who put in a lump sum are often caught on the wrong foot if the markets dip. On the other hand, SIPs help investors tide over the volatility by averaging out the cost (see SIP Advantage).

There’s another advantage. People fail to invest because of a variety of reasons. Either their agent fails to turn up, or they don’t have the time to visit a broker. Some forget to carry a cheque, others run out of cheques. All these issues are taken care of by SIPs because the investor gives post-dated cheques or instructs the bank to debit the SIP amount from his account. So, even if you forget to invest, your bank doesn’t.

SIPs yield the best results if a person continues to invest even during the downturns. Often, investors are so affected by a bearish market that they stop investing. This is a mistake because market dips are often the best time to buy cheap and average out your purchase price.

Caveat: In case of an SIP, your money gets invested on a specified date of the month, irrespective of the market conditions. However, this should not worry long-term investors.

If SIPs are the intelligent and affordable way of investing in mutual funds, systematic transfer plans (STPs) and systematic withdrawal plans (SWPs) are equally helpful in achieving your financial goals.

The Takeaway

The SIP investor gains by averaging out the cost of purchase. In the table, the average cost is Rs 17.90, even though in four out of the six months, the NAV is higher. The SIPs were beneficial during the downturn (April-May).

SWPs

This is the exact opposite of an SIP. In case of an SWP, a fixed amount is redeemed on a pre-determined day of the month and paid to the investor. These are useful for those who need a steady stream of income. Just as one can contribute a fixed sum in an SIP, the SWPs allow investors to customise the cash flow according to their needs.

STPs

In case of STPs, a fixed sum is switched from one fund to another every month. This is useful for investors with a large investible corpus and those who want to have a taste of equity by incurring minimum risk. Simply put, an STP combines an SWP and SIP. For instance, one can put a lump sum in a debt fund with an STP that transfers a small amount in an equity fund every month. This takes care of checking on the risk appetite of the investor.

Checklist

MUTUAL FIND MISTAKES TO AVOID

The key to successful mutual fund investing is not to avoid risks altogether, but to recognise them. Most investment mistakes are committed out of ignorance, laziness or inertia, and can offset the best laid financial plans. Though the errors can be expensive, they are simple to understand and overcome. Here are five common mistakes that every investor should steer clear of:

Mistake 1: Buying a fund or an NFO because of its low NAV

A new fund with an NAV of Rs 10 is not cheaper than a five-year-old fund with an earning history that reflects 15% annual returns. Most often investors buy funds based on the quoted NAV. The mistake is in not realising that high or low, a fund’s NAV at the time of purchase has no bearing on the returns. Remember, returns are defined by the performance of the instruments the fund invests in. If your fund manager is competent, he will pick potential winners and your fund’s NAV will rise. If he’s not good, your fund will lag behind.

Mistake 2: Portfolio churning

A mutual fund is often actively managed. So if an investor churns the portfolio too often, he should be aware of the entry load, exit load and tax implications. Though the entry load is waived by AMCs if one makes a direct investment, the taxman is not so liberal. There is no tax on profits from equity mutual funds if the holding period is more than a year. But if you sell within a year of purchase, the profit is taxed at 10%. The tax treatment varies across fund types.

Mistake 3: Investing and forgetting

If too much churning is bad for your portfolio, so is excessive passiveness. Most people tend to invest and forget. If you don’t monitor your investments, you may not know if the fund’s performance is slipping. Track your fund and review it quarterly or twice a year to check its progress. Compare its performance with its peers and the benchmark it is following. If a fund fares poorly over two or three quarters, it’s better to switch to a better option.

Mistake 4: Investing without a plan

Most Indians are good savers, not good investors. The difference lies in the lack of purpose or plan for savings. Begin by prioritising your needs and setting short-, medium- and long-term investment goals. This will help you select funds that are structured to serve the given purpose. Investment objectives can also be classified into safety, steady income or growth, which spells out the route for your plan.

Mistake 5: Not investing when markets dip

The investors who shied away from the markets a few months ago, when the indices were low, failed to make the most of opportunities. Investing systematically over market cycles evens out and improves the returns. SIPs imbibe discipline in investing regardless of the direction that the market takes.

FUND MYTHS

Myths can be injurious to your financial health. So, it is important to know your mutual funds and sift the facts from fables before you invest in them. Here are five myths that do not come with proven hypothesis.

Myth 1: Investing in mutual funds means investing in equities

Myth Buster: There are different types of funds with varying investment mandates—and not all provide equity exposure.

Mutual funds invest in various asset classes, and equity is just one of them. They also invest in debt instruments. Each plan is bound by the investment objectives outlined in the prospectus, which decides the security class(es) it can invest in. Based on asset classes, funds are broadly classified as equity, debt and balanced.

Myth 2: Large funds give big returns

Myth Buster: The chances of large corpuses giving higher returns are lesser than those by small corpuses.

Funds with the largest assets under management (AUM) don’t necessarily give good returns. Managing a large corpus is difficult because of the limited stock universe, making it difficult for to get out of the portfolio bias and be efficient in smaller funds.

Myth 3: Rankings are forever

Myth Buster: Short-term toppers may not hold good in the long run.

Money Today’s annual fund rankings stand testimony to the fact that fund-toppers in a particular year do not necessarily figure in the top rankings the next year. In fact, they may be among the worst performers. The disclaimer, ‘Mutual fund investment is subject to market risks’ is introduced to bust this myth.

Myth 4: Debt funds always outperform bank deposits

Myth Buster: Debt funds are taxefficient and so earn better than FDs.

This myth has arisen primarily due to the positioning of debt funds as a superior alternative to fixedincome securities like bank deposits. However, it is incorrect to compare a debt fund with a bank deposit as both have different risk profiles. While periodic interest payments and principal repayment are assured from a bank deposit, the same is not true of debt funds. Returns from debt funds can be higher or lower than those from bank deposits; it depends on how well a fund manages its portfolio. So the possibility of higher returns from debt funds comes with a higher risk.

Myth 5: Balanced funds invest equally in debt and equity

Myth Buster: Balanced funds have a mix of debt and equity that can be skewed towards either.

Balanced funds come with a rider: the fund manager can alter the mix between the two asset classes within the upper limits set for their allocation. It’s common for funds to maintain an equity holding of above 50% in debt funds and make the best of interest rate fluctuations by checking on NAV volatility. Remember, companies go to great lengths to create brand names in a mostly homogeneous industry. The performance of most funds in a particular style or category tends to fall within a narrow range of returns over the medium to long term. This is so because of the finite selection of stocks in each category. Nevertheless, fund companies will say anything to make them stand out.