When Sushil Kumar Aggarwal, a Jammubased businessman, wrote in with his problem in July, it seemed to be another case of a small investor getting overly worried because of short-term market movements. This first-time equity investor’s portfolio was down 16% and he wanted to know whether he should continue with his funds.

Before assuring him that equity markets are inherently volatile and that things will stabilise in the long term, Babar Zaidi analysed Aggarwal’s portfolio — and found a minefield of investing mistakes. Not only was his choice of mutual fund schemes ill-advised, even the strategy was flawed. The man appeared to be the epitome of how not to invest in funds.

Sadly, Aggarwal represents the average Indian mutual fund investor. His errors are elementary - the cardinal sins of mutual fund investing, so to say - but are very common. In answering Aggarwal’s problems, we highlight these frequent mistakes and offer solutions to rectify them.

Problem: Investing in new funds led to big losses

Had Aggarwal invested in the top rated equity mutual funds instead of new fund offers (NFOs), his loss— over Rs 1 lakh—would have been much lesser at Rs 11,000.

Aggarwal has invested Rs 6.46 lakh in six mutual funds in the past two years. Four of these were NFOs, in which he poured Rs 5 lakh. In doing so, he made the common mistake of buying a fund because it was priced cheap at Rs 10 compared with higher NAVs of the existing schemes. This is a fallacy because it doesn’t matter whether a mutual fund’s NAV is Rs 10 or Rs 100. The funds will use your money to buy the same shares from the same market. What matters is the stock picking and risk management skills of the fund manager. Instead of buying untested NFOs, Aggarwal should have simply opted for the best rated diversified equity funds. We found that if he had invested in six top rated diversified equity funds (see box) on the same days that he bought the NFOs, his losses would have been lower by almost 90%. One should invest in an NFO only if the fund is offering something remarkably different from an existing scheme with a good track record.

Solution: Finding the best funds is not rocket science. The MONEY TODAYValue Research annual ranking of best mutual funds (see MT, 25 June 2009) can help identify the top schemes.

Problem: Lump-sum entry was costly

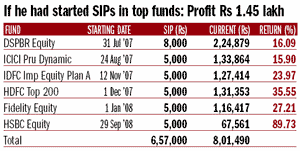

Investing small amounts in the best rated diversified equity mutual funds through SIPs would have earned him a profit of Rs 1.45 lakh.

All of Aggarwal’s investments have been as a lump sum. The first one in July 2007 was worth Rs 2 lakh. Over the next five months, he put in another Rs 4 lakh in tranches of Rs 1 lakh each. This is not the best way to invest in equities, especially for first-time investors such as Aggarwal. For small investors, the best strategy is to invest small amounts regularly. In a falling market, this helps bring down the cost of purchase. Our back-testing research shows that had Aggarwal invested in SIPs in the best rated equity funds, he would have earned a profit instead of the loss he is currently saddled with.

Solution: Invest through systematic investment plans. If you have a large sum, put it in a debt fund and start a systematic transfer plan to an equity fund.

Problem: High risk, low returns

Aggarwal took on more risk than he could stomach. His exposure to equities should have been smaller.

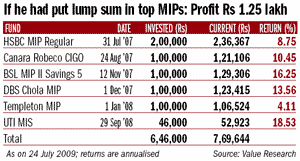

Aggarwal jumped on to the equity bandwagon at the fag end of the bull run. His funds are lined with risky stocks: mid-caps account for over 22%, small-caps, more than 8%, while almost 4% is invested in foreign stocks. Aggarwal didn’t need to take on this risk. Had he opted for the top rated MIPs instead, he would have earned a profit of 20%.

Solution: Ascertain your risk appetite before investing. For risk-averse investors such as Aggarwal, a good monthly income plan would have been more suitable.

Problem: Sector, thematic funds offered little diversification

The energy and financial services sectors account for nearly 50% of Aggarwal’s portfolio, while hot sectors such as tech and FMCG have a combined exposure of only 6%.

Diversification is a conspicuous absentee in Aggarwal’s portfolio. Two of the six schemes are infrastructure funds, two are energy funds and one is a lifestyle fund. The sectoral bias skews the portfolio, concentrating the risk and limiting the potential gains from other sectors. The small 2.5% exposure to the tech sector means that the current rally in tech stocks hasn’t helped the portfolio too much. The FMCG sector, considered one of the best bets right now, forms only 3.5% of the corpus. There is also some uncalled for diversification in the portfolio. Besides, one of the funds invests in overseas markets. The Tata Indo Global Infrastructure Fund has almost 25% of its assets invested in foreign companies. The fund has lost 32% since Aggarwal bought it in November 2007.

Solution: Thematic and sectoral funds are for more evolved investors. First-timers like Aggarwal should buy index funds or diversified equity funds. He should consider exiting the sector funds.