Investors as a tribe want their investments to resemble a Twenty20 match — stack up the returns fast and get out. But it’s the long-term investments, the Test matches of the financial world if you will, that generate the best returns. That’s because if there’s a day of bad weather, the Twenty20 fixture will have to be scrapped; in a Test match, you may still have another day of play.

Investors are beginning to see the virtues of staying invested for the long term, and are realising that it doesn’t pay to leave the field at the first sign of bad weather. They already knew the value of carefully selecting the team, otherwise known as their portfolio. What is important is to periodically review the constituents of the portfolio to see if all members are performing as they should. The Money Today-Value Research ranking of the best mutual funds is an attempt to take stock of a fund’s performance over the past year and compare it with other funds as well as its own previous performance.

| Click to see performance of top mutual funds |

In this story, we look at the best funds in the past one year across various categories. We also look at the common mistakes that investors make when the market goes through a bad patch or when there’s a bull run—that surge of irrational exuberance that investors feel when they see the benchmark indices touching new highs every day. To arrive at the best funds for 2008-9, we analysed the existing portfolios of the schemes and were more than convinced that equity mutual funds perform differently in different time periods. There is more to constructing an all-weather portfolio than just looking at best returns.

Investment Checklist |

|---|

| Set a financial goal or an investing plan before you buy a fund. |

| Clearly assess your risk tolerance and match it with the fund’s profile. |

| Track your investment periodically and make suitable changes. |

| Be clear about when you want to exit. Don’t let short-term volatility guide your decision. |

When building a mutual fund portfolio, investors must consider three factors: liquidity, income and growth. A well-planned portfolio will include investments to meet these three considerations and the flexibility to move easily between them as the circumstances change. Taxation is the fourth consideration and successful investors ensure that their investments minimise their tax liability by focusing on tax efficient funds and strategies. They also rebalance their portfolios on a regular basis, generally depending on their life stage.

Before getting into the nitty-gritty of constructing an all-weather portfolio, it helps to know how the equity mutual funds are classified and how their performance is impacted by market conditions. There are various types of funds, ranging from the least risky liquid fund to the riskiest sector funds. One way to construct a shock-proof portfolio is to opt for diversified funds. However, over the past few years, the equity funds category has evolved and it’s unfair to slot a contra fund with an ELSS or a dividend yield fund under the broad head of diversified equity funds. To make the universe of 342 equity mutual funds more meaningful and investor-friendly, we worked with Value Research to study data of the past few years to arrive at a new classification for equity funds.

Common mistakes by investors |

|---|

| Small investors often fall into investing traps and take the wrong decisions. Here are five common mistakes they made in the past year and what they can do now to correct them. |

| Overwhelmed by news Just because the Sensex delivered about 40% annualised returns during 2003-7, it does not mean that the future returns will be similar. Mutual funds trail index movements. Impact: The average diversified equity category gained 25% in 2006-7, but it lost 16% in 2008. Recourse: Temper your expectations and match them with the track record of the fund. |

| Succumbing to noise When the annual limit on investing abroad was raised to $2,00,000 (over Rs 90 lakh), there was a spate of new funds focusing on foreign investments. Impact: If you bought into Birla Special Situations Fund launched in January 2008 instead of the existing Fidelity India Special Situations Fund, your losses in the past one year would have been bigger. Fidelity lost 4.26% while Birla lost 8.44%. Recourse: Invest in a new fund only if it offers something that existing funds with a proven record don’t provide. |

| Investing blindly Investing is good but a dozen funds in a portfolio only add to the clutter and paperwork. Impact: A portfolio of Magnum Global, Magnum Contra, Magnum Emerging Business Fund and HDFC Premier Multi-Cap means you have almost the same large-cap stocks across the four funds. Recourse: Choose funds according to the goal they were bought for or the time frame that you intend to remain invested. |

| Indecision to exit or stay invested Most funds offer exit points to investors. But indecision and the greed to earn more can make one hold a fund for far too long. Impact: JM Basic did spectacularly in 2006-7 but got battered in 2008. In the past three months it has returned 132%. Make use of such opportunities to exit. Sometimes it makes sense to cut your losses and exit a fund when it starts to underperform. Recourse: Track performance and exit when your target is met. |

| Discontinuing investments While most investors bought into SIPs when the market was going up, the real gains kick in when the averaging is done in a falling market. Impact: Stopping SIPs is a bad decision. You not only miss the bus but are also deprived of the benefit of buying low and averaging. Recourse: Continue with SIPs as these are tools for long-term regular investing and wealth creation. |

It was easy to segregate the thematic and stated fund objective categories; the challenge lay in making three variants out of the broad equity diversified category. To match investor needs, these have been classified as large-cap funds (where the portfolio concentration has more than 70% large-cap stocks) large- and mid-cap funds (where the large-cap concentration is 40-70%) and the mid- and small-cap funds (where the large-cap concentration in the portfolio is under 40%). We arrived at these categories after analysing the average monthly portfolio concentrations over the past 18 months. This classification should help investors analyse equity diversified funds easily, keeping their investment objectives in mind. In all, nine categories of funds have been chosen and the best within these are ranked in the following pages.

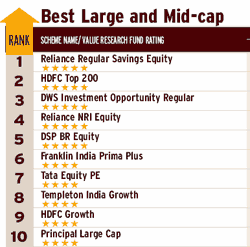

Our rankings have two specific objectives: the more obvious one is to show you which funds have performed the best during the past one year. The second objective is to identify your best bets in this market depending on your life-stage. If you are an existing investor, use this opportunity to rebalance your portfolio—exit the duds and invest in the promising stars. To the new investor, this is not overwhelming data. Just remember, you should exercise care while picking a mutual fund. Your choice will have a significant impact on how your financial goals are met. We have different priorities, responsibilities and financial goals at different stages of our lives. Adjust your target allocations when there are major changes in your personal circumstances, not when there are changes in the markets. For instance, if you are in your 20s, single and ready to risk a lot to gain a lot, an aggressive portfolio makes sense. A combination of large- and mid-cap funds and mid and small-cap ones should work for you. The portfolio of the top 10 large and mid-cap funds is heavy on large-cap stocks, with energy, financial services and FMCG constituting close to 50% of the portfolio. The stocks include Piramal Healthcare, Jain Irrigation Systems and Reliance Infrastructure. Overall, these funds have fared badly in the past one year, but they promise healthy growth over three years (the best performing fund has earned annualised returns of almost 20% during the past three years). The best performing scheme over a five-year cycle, DSP BlackRock Equity Fund, has earned annualised returns of 33.4%, indicating the benefits of staying invested for a longer period.

The funds in the mid- and small-cap category have lost more in the past one year, largely because of the nature of their holdings. IDFC Premier Equity lost 9% in the past one year but over a three-year period it earned an annualised return of 16%. This is not spectacular, but the fund offered exit options at higher returns during the market upswing between 2006 and 2007. The funds in this category invest in volatile and cyclical stocks such as Shree Renuka Sugar, Balrampur Chini and Orient Papers.

To build an aggressive portfolio, it’s a good idea to also include opportunities funds which focus on ultra large-cap stocks such as Reliance Industries, State Bank of India, Bhel and Hindustan Unilever. Both the DBS Chola Opportunities Fund and the UTI Opportunities Fund have a significant exposure to ultra-large cap stocks.

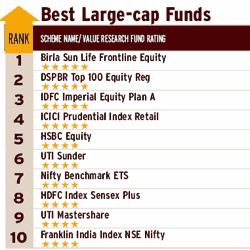

The focus on high risk is usually diluted as an investor grows older and takes on more responsibilities. He begins to look for growth as well as protection and his portfolio tends to be skewed towards large-cap funds with a small dose of mid-caps and a 10% allocation to dividend and contra funds. The top funds in the large-cap space, such as Birla Sun Life Frontline Equity and DSP BR Top 100 Equity, have a high allocation to large-cap stocks such as Infosys, Bharti Airtel and Reliance Industries.

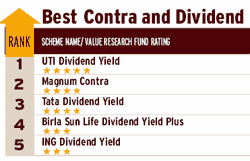

Dividend yield funds ensure stability and fuel growth, while contra funds neutralise the impact of wild market swings by betting against the market. Both UTI Dividend Yield and Magnum Contra have earned annualised returns of over 13% in the past three years, while restricting the past one year loss to under 4%.

After marriage, comes the next phase— becoming responsible for children. This is perhaps the longest life-stage and can last up to 20 years. Now, the focus of the portfolio shifts to stable growth and tax optimisation. Equity-oriented balanced funds and tax-saving ELSS are recommended. The high equity exposure of these funds provides the growth while the debt component cushions volatility. The best performing hybrid fund, Reliance Regular Savings Balanced, posted a gain of 11.16% in the past one year, when equity funds across all categories reported losses. The fund’s portfolio includes stocks with low volatility, including Reliance Industries, Larsen & Toubro, Infosys and Bharti Airtel.

Tax-saving funds reduce tax liability, and, thanks to the three-year lock-in, earn good returns. The top two ELSS funds earned over 15% over the past three years, with Canara Robeco Equity Tax Saver posting a 6.5% gain in the past one year.

The trickiest stage is the last 10 earning years before retirement. It’s time to rebalance past holdings to a conservative portfolio that focuses on monthly income plans (MIP) and debt plans that bring stability in the portfolio and also give regular income. The top three MIPs, Birla Sun Life, DBS Chola and Reliance, have all earned annualised returns of over 11% in the past three years while four of the top 10 MIPs earned over 10% in the past one year.

Finally, what do you do with your portfolio once you retire? Allow the corpus to grow and generate regular income. A mix of MIPs and debt funds is good for this purpose. A good debt fund should earn equal to or more than a bank fixed deposit. HDFC Mutual Fund has two short-term debt schemes in the top 10 that have earned over 13% returns in the past one year.

Whatever your life-stage, it’s important to rebalance your portfolio as you move on in life from one stage to another. Remember, there are no top mutual funds for all times. A prudent course is to build a robust, allweather portfolio by evaluating funds in each category, focusing on the long-term track record and considering how the funds have fared in different market conditions.

How the rankings were arrived at

RISK SCORE GRADING |

|---|

| High | Top 10% |

| Above average | Next 22.5% |

| Average | Next 35% |

| Below average | Next 22.5% |

| Low Bottom | 10% |

There are great years and so-so years, and then there was last year. Handing out honours for the top 2008-9 fund performance is akin to rewarding the one who lost the least. A lot has changed since our last annual ranking of mutual funds in June 2008 and a lot has been written about these changes. The third Money Today-Value Research ranking of best mutual funds cuts through the clutter to bring you the most promising fund picks across nine categories.

Evaluating funds: For equity and hybrid funds, the ratings are based on the risk grade of each fund compared with other funds in the category over the past three years. For debt funds, the ratings take into account the 18-month weekly risk-adjusted performance compared with other funds in the category. Value Research does not rate equity or hybrid funds less than three years old and debt funds less than 18 months old. Also, a category must have at least 10 funds for it to be rated.

STAR RATING CHART |

|---|

| * * * * * | Top 10% |

| * * * * | Next 22.5% |

| * * * | Middle 35% |

| * * | Next 22.5% |

| * | Bottom 10% |

Measuring risk: The Value Research risk grade of funds is different from the conventional risk and volatility measures like standard deviation and beta as they indicate only downside volatility. The fund risk grade not only takes into account absolute losses but also the periods when the fund underperforms a risk-free investment. The rationale: you can always earn a risk-free return from a bank deposit. The risk of investing in a fund not only includes the possibility of losing money but also the chance of earning less than you would on a guaranteed investment. To calculate fund risk, monthly/weekly fund returns are compared with the monthly risk-free return for equity and hybrid funds and weekly risk-free return for debt funds. Risk-free return is defined as SBI’s 45-180 day term deposit rate. For all months/weeks that the fund underperformed the risk-free return, the magnitude of the underperformance is added. This gives the average underperformance and how the fund performed vis-à-vis its category average. The relative performance of the fund is expressed as a risk score (see table), which captures the fund’s risk of loss.

Star rating: The Value Research fund rating is determined by subtracting the fund’s risk score from its return score. Then the final score is assigned a star rating according to the distribution on the right.

PORTFOLIOS ACCORDING TO AGE

Single

Portfolio Type: Aggressive

At this stage, different investors have different goals—saving for a house, wedding or even higher education. However, all of them have a common thread, that of making the most of one’s income. An aggressive portfolio is best suited for such investment goals.

Asset Allocation: 90% equity, 10% debt

Scheme Name And Allocation:

Reliance Regular Savings Equity (20%) | Equity: Large and mid-cap

IDFC Premier Equity Plan A (20%) | Equity: Mid and small-cap

Sundaram BNP Paribas S.M.I.L.E. Reg (20%) | Equity: Mid and small-cap

DBS Chola Opportunities (15%) | Equity: Opportunities

UTI Opportunities (15%) | Equity: Opportunities

DSP BR Short-term (10%) | Debt: Medium-term

Married

Portfolio Type: Growth

This is a phase when one’s income increases and so do financial responsibilities. Such a portfolio would also suit someone shifting from double income to a single income or someone looking to capitalise on his/her current financial position without any significant risk.

Asset Allocation: 80% equity, 20% debt

Scheme Name And Allocation:

Birla Sun Life Frontline Equity (25%) | Equity: Large-cap

DSP BR Top 100 Equity Reg (25%) | Equity: Large-cap

HDFC Top 200 (10%) | Equity: Large and mid-cap

DWS Investment Opportunity Regular (10%) | Equity: Large and mid-cap

UTI Dividend Yield (10%) | Equity: Dividend Yield / Contra

Canara Robeco Income (10%) | Debt: Medium-term

DSP BR Short-term (10%) | Debt: Short-term

Married With Kids

Portfolio Type: Growth with stability

The longest phase of one’s life, this phase poses the challenges of seeking growth with stability to fall back on. The various situations that life can pose are a change in job, children growing up, higher financial commitment or going through a divorce.

Allocation: 65-70% equity, 30-35% debt

Scheme Name And Allocation:

Reliance Regular Savings Balanced (25%) | Hybrid: Equity-oriented

Birla Sun Life Freedom (25%) | Hybrid: Equity-oriented

DSP BR Balanced (25%) | Hybrid: Equity-oriented

FT India Balanced (25%) | Hybrid: Equity-oriented

Pre-retirement/Retirement

Portfolio Type: Conservative

The 10 years before retirement is the phase when children become self-sufficient. At this stage, a conservative portfolio is ideal. This also works for someone whose income or assets may have increased.

Asset Allocation: 30-40% equity, 60-70% debt / 15-20% equity, 80-85% debt

Scheme Name And Allocation (Pre-Retirement):

Canara Robeco Income (20%) | Debt: Medium-term

Birla Sun Life Dynamic Bond Ret (20%) | Debt: Medium-term

DSP BR Short-term (10%) | Debt: Medium-term

Birla Sun Life Freedom (20%) | Hybrid: Equity-oriented

DSP BR Balanced (20%) | Hybrid: Equity-oriented

FT India Balanced (10%) | Hybrid: Equity-oriented

Scheme Name And Allocation (Retirement):

Birla Sun Life Frontline Equity (12.5%) | Debt: Medium-term

UTI Dividend Yield (7.5%) | Debt: Medium-term

UTI Floating Rate ST (15%) | Debt: Medium-term

Canara Robeco Income (20%) | Hybrid: Equity-oriented

Birla Sun Life Dynamic Bond Ret (20%) | Hybrid: Equity-oriented

DSP BR Short-term (15%) | Hybrid: Equity-oriented

Templeton India MMA (10%) | Hybrid: Equity-oriented