Most investors associate systematic investment plans, or SIPs, with shares and equity mutual funds. SIPs for

fixed income investments are rarely heard of. However, they can be as effective as equity SIPs.

"Investing in equity/debt through SIPs ensures discipline. This enables you to invest regularly without bothering about timing the market," says Jaya Prakash K, head, products, Franklin Templeton Investments India. "As it is, many Indians are familiar with regular fixed income investments in the form of recurring deposits," he says.

Experts recommend SIPs as they allow

investors to manage market volatility . Buying at market highs as well as lows averages out returns and gives stability to the portfolio. This can work for fixed income investments as well.

"There is volatility in the fixed income market as well, albeit lower than in the equity market," says Himanshu Pandya, senior vice president and head of products & communication, ICICI Prudential AMC.

Debt mutual funds are of three types - money market funds, duration funds and credit funds. Money market funds invest mainly in the overnight call money market and hence are the least risky. "Duration funds such as income funds do not take credit risk but carry high duration risk, while credit funds such as corporate bond

funds are high on credit risk but maintain a tight duration of, say, two to three years," says Pandya.

For instance, a credit fund like ICICI Prudential Regular Savings Plan invests up to 40% funds in AApaper, and hence carries a high credit risk. On the other hand, ICICI Prudential Income Fund, a duration fund, buys papers with tenures as high as 11 years and as low as two to three years. This means your returns will depend upon the time of entry and exit. "All fixed income funds have risks attached to them. Unless you want to park your money for a few days or weeks, systematic investing is ideal," says Pandya of ICICI Prudential AMC.

Credit risk involves default by the borrower. Investors are compensated for taking this risk in the form of interest payments. That is why credit risk is tied to the potential return on investment. Duration risk is the sensitivity of a bond's price to interest rate changes. Duration is expressed in years. The longer a bond's duration, the greater is its sensitivity to interest rates changes.

INTEREST RATE VOLATILITYPast experience shows that interest rates do not move in a straight line. "In fact, interest rate cycles have become much shorter since 2008, and in that sense, interest rate volatility has increased. In the past, rate cycles used to run for four to five years. This is now down to one to two years," says Jaya Prakash of Franklin Templeton.

In the last 10 years, the 10-year G-Sec yield has hit a low of 5% and a high of 9%. At present, it is 7.3%. In 2008-09, within a gap of six months, the Reserve Bank of India, or RBI, cut the repo rate by 425 bps; 10-year G-Sec yields fell from 9.3% to 5%. Thereafter, between March 2009 and December 2010, there was a secular bear market in which rates kept rising and yields went up to 8%, back to the 2005 levels (See chart on 10-year G-Sec yields).

In the last few months, yields have fallen from 8% to 7.3%. This is reflecting in the short-term performance of debt funds. For instance, ICICI Prudential's Dynamic Bond Fund returned 10% cent between 31 March 2012 and 31 March 2013; the SIP return during the period was 15%. However, Pandya says that looking at the oneyear return of a SIP can be misleading as interest rates have started falling only in the last few months.

Since the start of the year, the 10-year G-Sec yield has fallen from 8.2% to 7.3% as the RBI cut interest rates by 75 bps. Hence, in a SIP, investments made in the last few months would have done quite well.

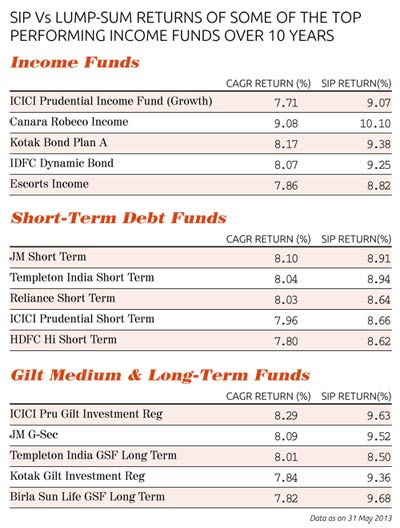

Over the long term, SIPs give better returns than lump-sum investments. This can be seen in the performance of income funds over the last 10 years. For instance, ICICI Prudential Income Fund has returned 1.36% more through the SIP route, followed by Kotak Bond Fund, where SIP has returned 1.2% more. This difference is more pronounced in some gilt funds as they hold longer duration bonds. Birla Sun Life Gilt Long Term Plan's SIP has returned 9.7% a year on a compounded basis compared to the 7.8% returned by the lump-sum investment. This is followed by Kotak Gilt Investment Plan.

IS IT A GOOD TIME FOR SIPs?"The decision to invest should be based upon market conditions. If you have enough cash flow and are not trying to outguess the market, you must invest regularly," says Jaya Prakash. SIPs enable you to hedge the risk of getting the timing wrong. It is also a good option for people with regular income who want to allocate a fixed amount for debt instruments every month.

Further, the choice of funds should be based on one's risk appetite and investment objective. A gilt fund, for instance, may not be suitable for someone who is 55 years of age and wants to avoid volatility. Hence, choose the right fund with help from your advisor and then go for a SIP.

"Having said that, SIPs might not make sense for ultra-shortterm funds, and investors can look at funds with an investment horizon of more than a year," says Jaya Prakash. Also, the market conditions have changed quite a bit over the last few years. In the past, one associated interest rate cycles primarily with changes in the long end of the curve, but nowadays systemic liquidity and other factors impact the short end of the curve as well.

Over the next one to two years, Pandya expects interest rates to fall 150 bps and G-Sec yields by 100 bps to 150 bps. However, he does not expect the 10-year G-Sec to move from 7% to 5% in a linear manner; he expects a lot of volatility along the way. "Investors can take advantage of this volatility by investing systematically," he says.

"Notwithstanding the recent monetary easing and continued weak macro environment, the outlook remains a bit uncertain given that the RBI continues to be concerned about inflation and the current account deficit," says Jaya Prakash.

So, with so many factors having a bearing on interest rates, expect a lot of volatility in the coming months. In such a situation, SIPs may be your best bet.