|

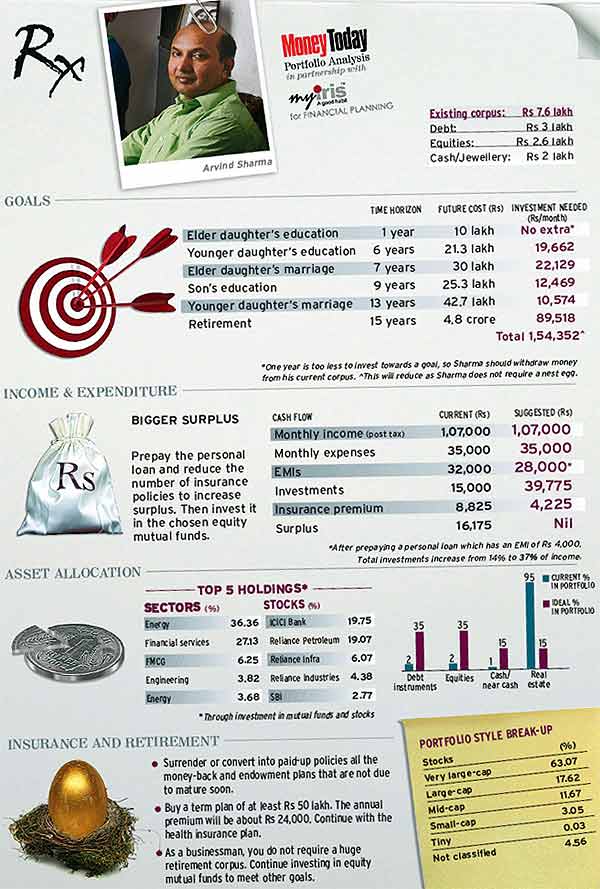

| Name: Arvind Sharma |

| Age: 43 Years |

| Monthly Income: RS 1,07,000 (post tax) |

| Financial Dependants: Three (Children) |

Clean. It's not an adjective that is commonly used for describing financial portfolios (unless it refers to record-keeping). For Arvind Sharma's finances though, it is an apt descriptor. His investments are diversified across all asset classes, there is minimal clutter of 'exotic' products and his cash flow has enough elbowroom. So do we have any work this time?

Yes, indeed, and quite a bit. It's easy to guess why if you compare Sharma's monthly investment of Rs 15,000 with Iris' estimate of how much he needs to achieve his goals—about Rs 1.5 lakh a month, or 10 times the current amount.

Before we begin to nip and tuck, it is imperative to discuss the first stage of financial planning, fixing goals, in some detail.

Recently, too many of our patients have approached us with aspirations that are higher than their income capacity. One reason could be that they are unable to grasp how the inflation monster pumps up the tame Rs 5 lakh to about Rs 9 lakh in 15 years. It is too much to ask of ordinary investors to calculate the future cost of goals accurately, but a rough idea will help to make their decisions realistic.

Another reason, and this is the most terrifying, is when investors assume huge jumps in income. This year should be an eye-opener for all those who count their chickens much before they hatch.

Finally, you could simply be dreaming. In the financial world, it is a costly exercise. Your planner may be forced to take drastic measures like an extremely high equity exposure to fulfil these 'dreams'.

In 43-year-old Sharma's case, it is neither over-expectation nor daydreaming. The primary reason for contacting us, he says, was the feeling that he won't be able to meet his goals. Is this true?

Maybe not. As Sharma is a businessman, he will not retire early and is likely to work till his heath permits. This almost erases the need for a nest egg, which reduces the required monthly investment to Rs 64,834. Besides, there is scope for downsizing other goals and Sharma must do it to bring the target closer to the surplus we can squeeze out.

A co-founder of a pest control company, Sharma has an average monthly income of Rs 70,000. This is padded up by his wife's salary of Rs 10,000 as a store in-charge and a rent of Rs 27,000 from the first and second floors of his house. His expenses are reasonable, Rs 35,000 a month, which is just 33% of his total income.

The EMIs of car, home and personal loans skim another Rs 32,000 from his kitty. His SIPs totalling Rs 15,000 in three funds, plus the average insurance premium for eight policies, reduces the monthly surplus to Rs 16,175.

As always, first let's try to increase the surplus. Sharma's personal loan charges an interest rate of 16% and its EMI is Rs 4,000. This is almost double the rate at which his debt investments like fixed deposits and bonds are earning. So he must withdraw money from them and repay the outstanding amount of Rs 1.41 lakh.

Sharma's insurance collection comprises only endowment and money-back policies, which cover him for Rs 8.8 lakh at a whopping cost of Rs 92,111 a year. We can't blame him as most policies pre-date the launch of term plans in India.

He must buy a term plan worth at least Rs 50 lakh. The annual premium will be about Rs 24,000. Next, he should either surrender or convert into paid-up policies all the insurance plans that are not due for maturity in the next four-five years. This move will release about Rs 6,600 a month, and along with the personal loan EMI, increase his monthly surplus to Rs 26,775.

Adding it up with his current investments, the total monthly investments swell to Rs 39,775, closer to the required figure. The entire surplus must be poured into equity mutual funds after building an emergency corpus.

Some of the debt funds in his portfolio can double up as his emergency corpus. Iris gives a thumbs up to IDFC Dynamic Bond fund, which is one of the few debt funds that are actively managed. DSP BR GSF Long Duration may be retained for the same purpose unless Sharma is a stickler for 'the less the merrier' (a philosophy that this magazine endorses).

An ELSS is unnecessary as his home loan EMI of Rs 21,000 exhausts the Rs 1 lakh exemption limit. Reliance Diversified Power is a sector fund that is risky for his requirement. Sundaram BNP Select Focus has been booted out because the function of adding zing to his collection is performed by Reliance Growth, a mid-cap fund. The other equity diversified funds like DSP BR Top 100, Kotak 30 and Reliance Equity are sound choices. After a very long time we are not adding anything new to a fund portfolio.

The three stocks in his kitty, ICICI Bank, Reliance Infrastructure and Reliance Petroleum, are an eye sore. This is one section of Sharma's portfolio which has no strategy. Therefore, he should sell them and stick to the known territory: mutual funds.

Finally, we laud Sharma's move of buying a health insurance policy that provides a cover of Rs 9.5 lakh to his family. This indicates foresight, which is the key to financial success.