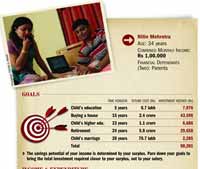

Mrs Neveright: What are you so upset about?

Mr Neveright: Can you believe that our neighbour's son, the 30-year-old executive, is already planning for retirement? And when I suggested that all he has to do is to put aside money in the Provident Fund, perhaps the Public Provident Fund as well, he just mumbled something about stocks and asset allocation. Stocks! Didn't the recent carnage teach him anything?

What is wrong with the Neverights' latest logic? Two things. First, they advocate putting all the eggs in one basket. They then make matters worse by picking the wrong basket for someone who can afford to take risk and build a decent nest egg. A foolish move, right? Yet, most Indians are guilty of not paying adequate attention to asset allocation. Even those who do their financial planning by the book—make a list of goals, identify the investible surplus and outline an investment plan to help reach the goals—often miss the big picture.

On paper, every investor knows that the four main investment vehicles that comprise his portfolio are equities, gold and cash, bonds and real estate. Says Sandesh Kirkire, CEO, Kotak Asset Management company: "To define it simply, asset allocation is the process of adjusting the relative proportion of different asset classes in an investment portfolio. It is based on the fact that both the probable return and volatility of each asset class are different." However, any long-term planning can be affected by how and which instrument you use to deal with the immediate circumstances. A bull run on Dalal Street? You are tempted to break a couple of fixed deposits and pick some stocks. A bear market? You follow the crowds and blindly bet on debt. Says Vikaas Sachdeva, country head, business development, Bharti Axa Investment Managers: "Most people sold equities in 2008 and bought in 2009, whereas they should have done just the reverse." Apart from the fact that you may be barking up the wrong tree, such a single-minded focus on individual instruments means that the proportion of each asset class in the overall investment plan is overlooked.

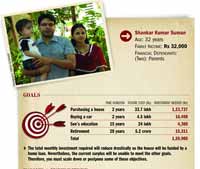

A carefully charted asset allocation plan is one way of ensuring that you aren't compelled to play a lemming. The main question that needs to be asked is—how much of my income should I allocate to each category? Life would have been so much simpler if there were a standard answer, a one-size-fits-all solution. Unfortunately, there are no shortcuts. The choice and proportion of each asset class depends on a host of factors, including the age of investor, his income level, risk appetite and number of dependants. It boils down to balancing the period till retirement with the amount of risk you can stomach. Here are some thumb rules that can act as guidelines to help you determine the best asset allocation mix.Equity: Your exposure to this instrument should ideally depend on your age; the younger you are, the longer the time you have to ride out any volatility. According to financial planners, subtract your age from 80 and the difference is the desired percentage of allocation to equities in your portfolio. If you are 32 years old, according to this calculation, you should invest about 48 per cent in equities. Also, people often treat equities as a short-term bet, whereas these only work to your advantage if you have a long-term horizon, at least three to five years, but the longer the better. Over a 25-year period, an equity fund is sure to give higher returns than most debt instruments. This implies that options like the Provident Fund and the PPF, which are seen as the best options to plan for retirement despite the 8-8.5 per cent returns, should not constitute the biggest chunk of your portfolio when you are young. Equities give alised returns of around 12 per cent. Over a 25-year time frame, even a 2 per cent annualised difference can result in 35 per cent lesser funds in your nest egg. If you don't understand market dynamics, mutual funds can be a better route.

Debt: In this category, the choice of a financial product depends on one's tax slab, degree of security, expected return and the period after which the money is required. Most people wrongly enter debt with a long-term tenure. Instead, you should increase your exposure to this category after you hit middle age.

Gold/cash: Experts recommend that investors should keep aside about 5-15 per cent of their stockpile for this category. Choose from coins, ETFs and jewellery to invest in gold. Says Kirkire: "By combining asset classes in different proportions, it is possible to modify a portfolio's overall volatility and return." The key is to stick with the allocation plan, making consistent contributions no matter what, and rebalancing it annually. Yes, it's sleepinducing, but a little effort on your part today can ensure that you sleep easy tomorrow.