Two good fund baskets in a row is a happy coincidence. In our experience, the collection of funds is the prime problem with most portfolios. The funds are either in excess, or are inappropriate to the risk profile of the investor, or have duplication of equity exposure. So when we analysed the finances of Arvind Sharma in the previous fortnight and found that his basket required only minor trimming, it was a rare occurrence. To discover that the next patient, 31-year-old Vijay Sharma, has also made wise choices and has a fund collection that doesn't need to be touched, seems too good to be true.

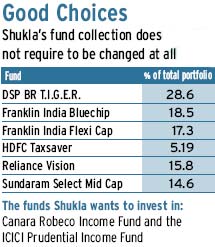

Shukla, a team leader in an engineering company, has invested in just six funds, which include an ELSS, three large-cap funds and two mid-cap funds. This combination of funds suits his high-risk appetite. Moreover, there is minimum duplication of equity and Shukla has chosen from the top-performing funds in their respective categories.

All seemed perfect till we asked Shukla how he had chosen the funds. Instead of professing a deep understanding of the dynamics of the market, he admitted that the selection of funds was based on inputs from a friend who "spends close to three hours every day studying the markets and various companies".

Such diligence in tracking the markets gives him the required credentials in Shukla's eyes and he follows the advice of his friend religiously. Shukla doesn't do any research on investments except to look at the "returns of the past three years which must be about 25%".

This faith, as we have pointed out, has proved to be very profitable for him. But it is rife with danger. Shukla's ignorance about the nature of funds, the various parameters for judging their performance and the dynamics of the market can nullify the effect of choosing good funds.

For instance, he may exit the fund which should be held for the long term or skew the risk profile of his portfolio by over-investing in one fund. In case a good fund becomes a slack performer, he will be unable to identify the reason and, hence, will not be able to take remedial steps.

Ignorance about financial matters cannot be excused. So, though, Shukla has been lucky to be advised by a well-informed friend, it cannot be the basis for a successful financial plan. This magazine has always said that investors must equip themselves with the knowledge about their finances even if they have enlisted the help of a planner. So before we begin analysing Shukla's finances, we suggest that he invest time in brushing up his personal finance IQ.

Shukla brings home a monthly pay cheque of Rs 67,000 (post tax). He is single and does not spend lavishly, restricting the monthly expenses to Rs 10,000, or 15% of his income. In 2006, Shukla bought an apartment in Bengaluru financed by a home loan of about Rs 16 lakh at 8.5% interest rate. The monthly EMI of the home loan skims away Rs 13,247 from his income. In the same year, he had taken a personal loan at about 13% interest, for which he pays an EMI of Rs 5,300. The outstanding amount for the personal loan is Rs 75,000.

After subtracting these EMIs, SIPs of Rs 6,000 in the five funds and the average insurance premium of Rs 3,440 a month, Shukla's cash flow generates a handsome surplus of about Rs 22,000. What does he do with the money? "It is usually in my savings bank account," says Shukla, who is sitting on about Rs 2 lakh cash stacked away in his account.

As we have said so often in this space, money idling in a savings account is eroding in value. Even though inflation is touted to be 0.26%, the CPI-UNME, more relevant to the urban consumer, is still around 9.9%. Therefore, assuming status quo for one year, the purchasing power of Rs 2 lakh will shrink by 6.4% to Rs 1.87 lakh.

So, the top priority must be to withdraw money from his bank account and invest it. Where should Shukla put this money? In equities, of course, specifically in equity mutual funds. Shukla knows just the ones that are appropriate for his risk profile and goals.

This brings us to the Rs 1.45 lakh that he needs to invest every month. Even though Shukla saves a tidy sum, it falls short of the required monthly investment by a whopping Rs 1.23 lakh. In such a case, it is imperative that we closely scrutinise the targets of the financial plan to ascertain how realistic they are.

Shukla wants to pursue his MBA in the next two years, for which he requires about Rs 22.5 lakh. For this, he must invest Rs 82,491 a month. This goal seems to be unachievable at first glance, but Shukla will probably take an education loan, which will drastically reduce the required monthly investment.

The next goal, of starting a business by the end of 10 years, is a huge strain on his finances as it requires a monthly investment of Rs 29,354— more than his current surplus. There is nothing left for building his nest egg, which needs an investment of Rs 33,091 a month.

Clearly, Shukla must prioritise his goals and downsize or postpone some of them. He may have to choose one over the other, which is actually easy as a successful business would mean that Shukla's retirement will be pushed back till his health permits. This automatically erases the need for a large retirement corpus.

A striking feature of his goals is the absence of the more common ones, such as buying a house, marriage, etc. By purchasing an apartment early in life, Shukla has done away with a costly goal. He expects his parents to pay for his marriage, so this is also not on his list. Shukla thinks it is too early to plan for the expenses of children, so they too do not feature in his goals.

Having discussed the possibility of downsizing his goals, we will now approach the problem of the requirement of a very high monthly investment from another angle: by trying to increase his monthly surplus.

For this, our first target is the personal loan EMI. We suggest that Shukla use a part of the Rs 2 lakh twiddling its thumbs in his savings account to repay the outstanding personal loan of Rs 75,000. He could also have withdrawn money from his debt instruments for this purpose as they earn an interest much lower than the 13% personal loan rate. However, as the difference between the borrowing and earning rate is maximum for the savings account, we prefer it.

Another way to increase Shukla's monthly surplus is by converting his endowment plan to a fully paid-up policy. The plan is very expensive and provides a cover of Rs 8 lakh at an annual premium of about Rs 41,000. To compensate for the loss in cover, Shukla can buy a term plan of Rs 10 lakh for 20 years. The annual premium will be about Rs 2,800. These two moves, prepaying his personal loan and converting the endowment plan to a fully paidup policy, will add Rs 8,740 to his surplus. As recommended earlier, he should invest this sum in equity mutual funds.

In addition to the current funds, Shukla wants to invest in the Canara Robeco Income fund and the ICICI Prudential Income fund. This is because he has learnt from the media that income funds perform better during recession.

While his statement is an indictment of the irresponsibility of certain sections of the media, it is also another reminder of Shukla's lack of financial acumen. Income funds have been performing well recently, but this has no relation to the slowdown in the economy, rather to the falling interest rates (see Demystifying Income Funds).

No financial decision should be based on the lure of such short-term benefits. Moreover, Shukla's portfolio does not need an income fund. If he wants to build an emergency fund, a better option is to invest in a liquid fund as it provides the benefits of both accessibility and returns which are a little higher than those from a savings account.

Another reason for investing in these funds is that Shukla wants to increase the amount of his SIPs. This is also our suggestion, but he need not invest in new funds. Iris clearly recommends increasing investment in the top funds in his portfolio, instead of adding other funds that will destroy the perfect blend of his fund collection and make it unwieldy.

Perhaps Shukla's wisest move has been to stay away from direct equity. He understands that dabbling in stocks requires time and financial acumen, which he does not have. Shukla's aim should be to prevent his strong financial position from being diluted by his ignorance rather than experimenting with risky investments. He can take a tip from our ex-patient Ashfaque Ahamed (see Reviewing Past Patients).

![]()