Mr Neveright: It's the last minute scramble to save tax. In fact, I advised an ex-colleague to take a money-back insurance policy just yesterday.

Mrs Neveright: I've heard that these policies command a huge premium, don't they?

Mr Neveright: So what? You not only save tax but also get back cash at regular intervals.

Two issues later, Portfolio Doctor's whipping boy, Mr Neveright, agrees that life insurance is indispensable. But all for the wrong reasons. Money Today has said it often enough, and we'll say it again—the purpose of insurance is to provide financial assistance to the dependants of the insured person in case of his untimely death. The tax benefit is just the icing on the cake.

Yet, most Indians continue to subscribe to the Neveright logic and remain underinsured. According to the Insurance Regulatory and Development Authority of India (Irda), the total sum assured (life cover) in the country as on 31 March 2009 was Rs 29,13,703 crore, and it was spread across 29 crore life insurance policies. This means that the average sum assured per policy works out to just over Rs 1 lakh. This does not imply that every person is covered only for Rs 1 lakh as people usually buy more than one policy. However, it emphasises the fact that protection is not the most important reason for buying insurance. If it were, customers would not agree to such a low cover.

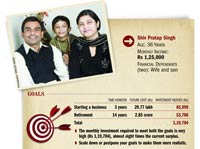

Though insurance needs are specific to an individual, the rule of thumb is that the insurance amount should replace your income, repay all your outstanding dues and allow your dependants to maintain their current standard of living. Ideally, one should have a cover that is at least five to six times one's annual income.

The first thing to do before buying a policy is to assess your insurance needs by considering the big picture. You should factor in the daily expenses of your family, account for inflation, life-stage expenses like your child's education and marriage, and other bigticket expenses as well as any existing debt. Also, a working spouse need not translate to a fool-proof safety net. In dual income households, it is the combined salary that should be taken into account while calculating the amount of cover you need.

Now, for the big question: which policy should you take? A term assurance policy is your best bet as long as the primary motive is adequate coverage. Yes, there is no wad of cash at the end of such pure protection plans if you survive the term, but don't let this disappoint you. This policy is not only cheaper than the investment insurance ones, such as unit-linked insurance plans (Ulips), but also promises a higher cover. The cost of a term assurance cover of Rs 20 lakh for 25 years for a 35-year-old, along with an accidental death and disability cover of Rs 6 lakh, works out to Rs 8,700, inclusive of all taxes. A similar cover in the case of an endowment plan would cost around Rs 80,000 a year.Don't think that the premium paid on a term plan is a waste because it doesn't have a maturity value. Mortality charges are deducted in all insurance policies. This means that a part of the premium for your Ulip, endowment or moneyback policy is used to pay for the insurance cover.

The Neverights were also wrong in their assumption that a higher premium outgo promises adequate insurance cover. It might do so, but only if the policy is a pure term cover. In other policies, such as endowment or money-back plans and Ulips, there is also an investment component. While this pushes up the premium, most people would not be able to afford the cover they actually need. A customer can save on premium by taking a term assurance policy and invest the money in more lucrative options, such as equity mutual funds and the Public Provident Fund, to reap higher rewards.

It's advisable to take insurance for the longest term possible, which is 30 years. Don't be tempted to opt for a shorter tenure just because the premium is lower. If, at 30, you take a 20-year cover, the policy term would end when you are 50 years old, leaving you defenceless when you are close to retirement. Taking a new policy at that age would mean an extremely high premium outflow. Worse, if you have developed a medical condition in the interim or suffer from some disease, you may be denied insurance completely.So, instead of calculating insurance needs from the point of view of the premium you have to pay, focus on the sum assured. When you go to a showroom to buy a shirt, do you pick one that has a poor fit just because it suits your wallet? No, you wouldn't. So, why should an insurance plan be any different?