When professors Thomas Stanley and William Danko set out to research wealthy Americans, they interviewed residents of the most affluent parts of Atlanta, Georgia (the corporate headquarter of 14 Fortune 500 giants including Coca-Cola).

They found that many highincome people had low net-worths while many middle-income people had attained millionaire status by saving and investing judiciously.

The professors developed a thumb rule to determine if an individual was generating wealth commensurate with income: multiply age by pre-tax annual income and divide by a factor of 10 to arrive at the minimum net-worth target. For example, a 35- year-old with Rs 20 lakh income should possess a net worth of at least Rs 70 lakh.

If it wasn’t for the fact that the Paridas live in Delhi, they could be easily classified as one of the high-income, low net-worth American couples that Stanley- Danko encountered. Between them, banker Jaya and Nihar, who is general manager in an MNC, have an annual income well in excess of Rs 20 lakh. They are both in their mid- 30s and they have only one dependent in their six-year-old daughter, Kavya.

Using the Stanley-Danko formula, their net worth clear of loans and liens should come to over Rs 70 lakh. Their total assets amount to about Rs 85 lakh—but there are total outstanding longterm loans of about Rs 29 lakh on those assets. Once we calculate the asset value after deducting the loans, their net worth amounts to a little less than Rs 55 lakh—which is significantly lower than it should be.

Of course, the Paridas are scarcely badly off. But they could be a lot better off if they had been more judicious in their investments. Compared to their earnings, Jaya and Nihar have worryingly low investments.

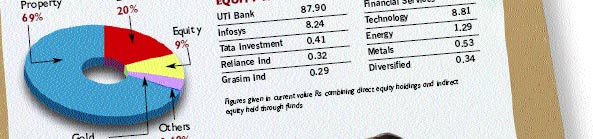

Jaya has an annual salary of Rs 10 lakh, which is roughly equivalent to her husband’s. Where investments are concerned, she seems to be prudent. She has invested in NSCs, jewellery and infrastructure bonds, apart from picking up one mutual fund—Franklin Templeton Growth. She also owns stocks of UTI Bank, Infosys and Petronet. Though the choice of scrips is good, the investment is concentrated (see table).

Nihar seems to have sworn off investments in debt and equity. But he did partner Jaya in buying a flat that is now worth nearly Rs 55 lakh. They have also picked up insurance cover worth Rs 43 lakh in a combination of term and moneyback policies. Of this, about Rs 25 lakh is invested in policies in the name of their daughter. The Paridas are currently servicing three loans. They have taken two car loans of Rs 11 lakh and a home loan of Rs 20 lakh. The outstanding amount on all loans is roughly Rs 29 lakh. So while the Paridas are well-off, a sound financial plan is the need of the hour. If they save and invest intelligently, they could amass a huge wealth over a fairly short period of time.

First, they should estimate the amount of money they want to keep in liquid assets, that is in cash and cash equivalents. As a thumb rule, we recommend keeping an amount equal to at least six months’ worth of expenses. This will help tide over any emergency. If they foresee some specific expenses in the short term, that amount should be added to the above figure. The remaining part of their savings should be channeled into various fixed-income and market-linked instruments.

The couple has a high-risk taking profile. They are young, earning well and have just one dependent. Therefore, they should opt for a higher equity allocation. Using another thumb rule, their asset allocation should be roughly 65% to equity and about 35% to debt—the debt allocation should be roughly equal to your age.

This can be achieved through a portfolio of equityoriented mutual funds. We suggest they follow the mutual fund ratings that appear every three months in MONEY TODAY to pick funds from equity diversified, tax planning and hybrid equityoriented funds. It is advisable to invest in these funds only if they don’t intend to withdraw for the next three years or so. Investments in equity give the best returns only in the long term. For investments of a shorter duration, debt-oriented funds like monthly income plans, fixed maturity plans or other fixed income instruments like bank fixed deposits (which are yielding handsome interest these days) should be preferred.

For the high income levels that they have they are inadequately insured. They must scale up their insurance by about Rs 20 lakh each. For outstanding liabilities one of them can take a term plan of over 10 years for Rs 25 lakh. Both seem to carry no health insurance. A cover of Rs 5 lakh each is also an intelligent step.

It is also important that the couple exhaust the Rs 1 lakh limit for each under Section 80C to save tax by investing in specified instruments. The most common ones are tax-planning funds, NSC, PPF, LIC premium. Jaya and Nihar are also planning to purchase property in NCR for purely investment purposes. They must be careful and research before buying. Real estate has already seen tremendous appreciation in the past two years and many experts warn against buying property right now. They must also assess their own loan repayment capacities, since they already have substantial commitments. Therefore, making an investment in real estate may not be a good idea at this time.