| |

|---|---|

| Name | Subramanian (right) and Visalakshi Nachiappan |

| Age | 34 and 33 Years |

| Monthly income | RS 38,000 (post tax) |

| Financial dependants | one (son) |

Now for some bad news, Nachiappan's portfolio is very slim. His investments in debt and equities total about Rs 4 lakh only. This, despite the fact that he and his wife Visalakshi, 33, have been working for more than 13 years. Visalakshi is a teacher and brings home Rs 18,000 a month. Subramanian adds another Rs 20,000 to the kitty. Their monthly expenditure is about Rs 12,000-a reasonable 31.6% of the couple's income.

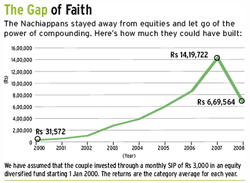

Subramanian started his investing journey alongside his career. So the reason for his scrawny stockpile is not ignorance, but bad experience. Between 1996 and 2000, he bought stocks avidly. However, the Ketan Parekh scam eroded the value of his stocks by nearly 90%. Subramanian was bitten once and has been shy since. For a while, he steered clear of equities altogether.

It took a bull run of three years to convert Subramanian. He bought stocks and funds in March 2008 when the market dip was considered to be temporary. This gap of eight years has cost the couple dearly and they have lost out on the advantages of the power of compounding.

This is also why the monthly investment required for meeting the couple's goals is high. Iris estimates it to be about Rs 44,000-15% more than the Nachiappans' total income. Before we tell them where to invest, let's try to bring this figure down.

First on the to-do list should be the postponement of goals like the foreign trip. This will reduce the burden on their cash flow. The most significant relief can come from the lowering of the required retirement corpus. As Visalakshi is employed in a government school, she is entitled to a pension if she continues with the job. We suggest that she stick with it till retirement as a pension equivalent to her last drawn salary will mean that the couple can make do comfortably with half the projected nest egg of Rs 1.8 crore.

After deducting the average premium of Rs 2,216 for Nachiappan's life insurance policies and a Rs 1,000 SIP in JM Small and Mid Cap fund, the couple's monthly cash flow generates a handsome surplus of Rs 22,784. Obviously, they are still not investing what they save. The couple has a high risk appetite and must exploit it by investing the entire amount in the equity market.

Within equities, the way to go is SIPs in mutual funds. Iris suggests that Subramanian exit all the existing funds. SBI Bluechip is not the best performer among equity diversified funds and should be replaced by HDFC Top 200. To sync their tax saving with the plan, they should go for an SIP in HDFC Tax Advantage, Templeton India Taxshield or ICICI Prudential Taxplan.

We suggest that the couple avoid investing in mid- and small-cap funds as their portfolio is very rudimentary and does not require the diversification provided by such funds.

Direct equities is an absolute no no for Subramanian. His track record in stock-picking is bad. Two of the four stocks that he had chosen in the late '90s-Orient Technologies and Crescent Communications-are no longer listed. The other two, HFCL and Silverline Technologies, are trading at single-digit prices. The three stocks currently in his collection, Reliance Communications, Dish TV and India Cements do not follow any investing principle. Subramanian bought them on the recommendation of his brokers and father. As he does not have the time and acumen for dabbling in stocks, he need not take the risk.

For insurance, Subramanian has chosen a combination of four term plans and one money-back policy. Together, they cover him for Rs 4 lakh. This is an inadequate cover. Subramanian should surrender the money-back policy and buy a term plan that covers him for at least Rs 20 lakh. Visalakshi should also buy a term plan of the same amount. The annual premium will be about Rs 6,500 each. Subramanian has made a wise move by buying a health insurance plan. Iris suggests that he switch to a public sector insurer after the current plan expires as these companies are more agreeable to extending the cover beyond the age of 60 years.

In the first half of this year, the couple plans to buy an apartment worth Rs 20 lakh. This is in addition to a plot valued at Rs 1.6 lakh that they have in Chennai. The EMI for the home loan will be about Rs 17,000. This will reduce the couple's surplus, but we suggest that they continue to invest in the recommended funds.