Money Today experts answer your personal finance queries -

INVESTING Q. I am 27 years old and my savings have been reduced after failed equity investments. I have no dependants and can invest up to Rs 20,000 per month. I have lost confidence in my ability to invest in equities. What could be an alternative? I plan to retire by about 65 years. - VK Kumar, e-mailA. Investing in equity markets requires precision and research and a portfolio should be adequately diversified. Considering your age and that you have no dependants, you can take risk initially and move to balanced and debt instruments later on. Invest in mutual fund scheme through a systematic investment plan (SIP), which will help you to mitigate the risk. Here is a portfolio you can consider now.

Q. I was born in India but am a resident of Malaysia. I had bought an apartment in Pune in 1983 under Section 31 (1) of the Foreign Exchange Regulation Act, 1973 (FERA), with RBI approval. An RBI notification later (FERA 152/93-RB dated 26-05-1993) granted foreign citizens of Indian origin permission to acquire and sell property. I sold the flat in 1997 without RBI's permission, a condition for approval, based on this notification. Foreign exchange regulations have changed considerably. Section 31 is no longer applicable. If I want to buy the same property today, what will be the process? Does it change if the buyer and seller are related? -Chitranand Kumar, HyderabadA. Acquisition of property in India by persons resident outside the country, including foreign nationals, is regulated by Section 6 (3) (i) of the Foreign Exchange Management Act (FEMA), 1999, as well as by the regulations included in notification number FEMA 21/2000-RB, dated 3 May 2000, which is the latest amendment.

As per the permissions granted, non-resident Indians (NRI) and persons of Indian origin (PIO) can purchase property in India. But, the permission for the purchase of property covers only residential and commercial property and not purchase of agricultural land, plantations and farm houses in the country. Also, as per the law, an NRI or PIO can buy property from anyone in India irrespective of the relation between the parties.

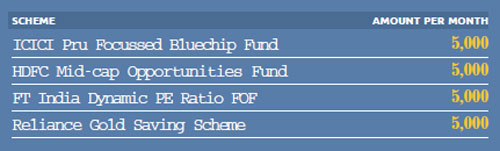

Q. I am 28 years old and have systematic investment plans (SIPs) in DSP BlackRock Top 100 Equity Growth (Rs 1,000 since December 2010), Franklin India Bluechip Growth (Rs 1,000 since January 2011) and IDFC Premier Equity Growth (Rs 2,000 since January 2012). I also have been putting Rs 5,000 in National Pension System (NPS) since April 2011. I want to plan for my retirement at about 60 years. My monthly expenses are about Rs 30,000 in today's value. I have up to Rs 2 lakh in bank fixed deposits (FDs). I can invest another Rs 10,000 per month. I have two life plans maturing in 2039. What would be my best options? -Priyank Mathur, MumbaiA. Your existing portfolio is sufficiently diversified for now. But, we would recommend you add debt mutual fund schemes or bonds. You can also consider adding a gold scheme (inverse correlation with equities) to limit the number of mutual funds. It is also recommended you include one balanced mutual fund scheme. This will help mitigate risks.

Considering retirement age as 60 years, these asset allocations should be what you need. Your requirement of Rs 30,000 will be about Rs 1.9 lakh by the time you retire considering inflation. If we consider the growth rate of 10 per cent per annum on your investments, then your contribution, including the additional Rs 10,000, should give you about Rs 5 crore by the time you retire.

Q. What would be the best fixed-income or stable investment instruments to balance my equity portfolio? I have almost 65 per cent of my investments in equities and equity mutual funds. I am 26 years old and spend about Rs 30,000 per month, inclusive of all my expenses. -JR Akshay, e-mailA. Considering your existing investment (65 per cent in equities), we assume the remaining is in debt. You can take a higher risk at this age and reduce as you grow older. As for investments that provide fixed or stable returns, we would recommend bonds, especially tax-free bonds, for which the interest payout is not subject to tax. There are chances of capital appreciation as well if the price of the bond is higher than the purchase cost. However, capital gains will be taxed depending on if it is short-term to long-term gains.

INSURANCEQ. I switched jobs in the previous financial year. Coincidently, the group health insurance provided by the new employer is from the same company with which I have an individual health plan. So, what will the claim procedure be in case of an emergency? -K Mohan Menon, KolkataA. ABefore you have the need to make a claim using either of the insurance plans, review the contribution clauses of both policies to know what payout ratios exist for each. You will know which policy would be best to claim certain expenses after reviewing the respective clauses on inclusions, waiting periods, etc. Of course, it will help the claims process to be as transparent as possible and inform the company of the multiple policies. Also, it is prudent of you to have a personal health policy along with the group cover.

Q. I am planning to buy a personal accident cover. I have a term plan that offers it as a rider. I also know of credit card companies that provide this policy. Are these plans different? Which one should I pick? -Sandeep Srinivasan, New Delhi

A. You can get a personal accident cover as an independent policy from a general insurer, as a rider under a life insurance plan or as part of benefits offered with a credit card. What is important, is the nature of cover offered under each option.

A stand-alone cover from a general insurer and health insurance firms offer additional benefits along with the standard death benefit, such as benefits for permanent full or partial disability, temporary disability, medical expenses, etc. You can also choose the cover amount.

Accident covers offered as a rider to a life insurance policy usually only offer death cover with additional coverage for permanent full disability in some cases. However, the cover would be based on value of the life insurance plan. Coverage offered with a credit card is basically a group insurance plan for all members who avail the card. It would be available only as long as the card is active.

Q. I have a family floater health plan, which also covers my parents. The premium is Rs 25,000. How much can I claim as deduction (as per Section 80D of the Income Tax Act, deductions of Rs 15,000 for self and Rs 15,000 for parents are allowed). This premium also includes Rs 1,000 for a personal accident rider. Is this sum exempted as well? -David D'Sa, Goa

A. Under Section 80D of the I-Tax Act, 1961, the premium paid for a health insurance policy can be deducted from a person's total earnings for the year. The amount of deduction available on a health insurance policy for self, spouse and dependent children is up to Rs 15,000. A further deduction of Rs 20,000 is available for paying the premium for coverage for one's parents. Hence, the premium of Rs 25,000 for yourself and your parents is deductible. The premium for the rider, of Rs. 1,000, for the personal accident rider is also deductible as per the same regulation.

REAL ESTATEQ. I bought a flat A for Rs 28 lakh in April 2008. I sold it in August 2012 for Rs 32.51 lakh. The stamp duty and registration fee was borne by the buyer. Will I incur short-term capital gains tax? What is the purchase cost and sale cost of the apartment to calculate profit or loss? - Gaurav Tangri, DehradunA. The registration date is relevant for computing capital gain, not the possession date. Considreing the registration date as April 2008, the apartment was held for over 3 years. Hence, it is long-term capital gain and indexation benefit will be allowed on the purchase cost. Purchase cost will be Rs 28 lakh and the indexed cost is (28x852)/582, which is Rs 40.99 lakh. Your profit or loss will be computed as: Sale consideration-Rs 32.51 lakh, minus indexed cost- Rs 40.99 lakh and so a net loss of Rs 8.48 lakh.

Q. I wish to buy a property in the next few months. However, I do not know if I can build a house immediately. Is it necessary that I construct a house on the plot within a certain period? -Ravi Mishra, e-mailA. There are no conditions on when you should construct a house if you buy property without a loan or if it was not specifically allotted for this purpose by a development authority.

However, If you have taken a composite loan, i.e. for purchase of property and construction of a house, the bank would have imposed a condition requiring you to start construction within a reasonable period.

If you do not start construction within this period, the bank will treat you as a defaulter as per the loan agreement. You will have to repay the full loan immediately and pay a higher interest on the amount since inception. This will aslo affect your credit history and your credit score with credit information companies such as CIBIL.

A composite loan is a better option than a plot loan. Loan financing goes up to 80-90 per cent (60-65 per cent on plot loan) and you get tax benefits as well.

TAXATIONQ. I have been trading shares since 2007 but I have not shown it in my tax returns as I have always incurred a loss. What can I do to file returns on these transactions? Will I incur a penalty if I do so? -P Alurkar, BengaluruA. No, there is no penalty for not disclosing losses. However, you should know that share losses can be carried forward up to 8 years for adjustment to save tax.

Q. My paternal aunt wishes to gift agricultural land to me. This land was inherited by her from my grandfather. What are the tax implications on this gift? -Deepak Jain, e-mailA. There is not tax on the gift that you will get from your paternal aunt. No income tax is levied on a gift received from relatives. The term 'relative' includes: (1) spouse, (2) a sibling, (3) siblings of your spouse, (4) an uncle or aunt, (5) a lineal ascendant or descendent, (6) a lineal ascendant or descendent of the spouse and spouses of the persons referred to in (2) to (6).

Anil Rego, CEO, Right Horizons has tackled financial planning; Harsh Roongta, CEO, Apnapaisa.com has responded to the real estate financing query; Antony Jacob, CEO, Apollo Munich Health Insurance has answered insurance queries; and Taxspanner.com has provided tax solutions.