In the past two years the cost of building a house has doubled, thanks to the spurt in prices of almost all construction material. Whether you can afford a house also depends on how the cost of finances (loan) and your income level have moved.

Income level

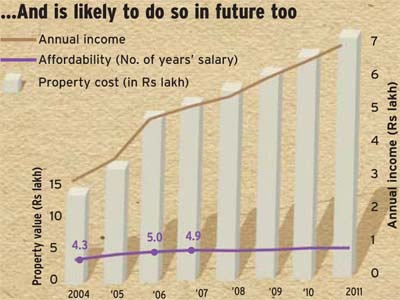

Costs have risen, as have incomes. The impact of the two determines whether affordability has risen or fallen.| How rising income has offset costs... | ||

| SCENARIO II | 2004-5 | 2006-7 |

| Price of a two-bedroom flat | 30,00,000 | 52,50,000 |

| Loan (85% of value) | 25,50,000 | 44,62,500 |

| Monthly take home | 45,000 | 73,125 |

| Interest rate—20-yr loan | 7.5% | 7.5% |

| EMI without change in interest rate | 20,542 | 35,949 |

| EMI as % of monthly salary | 46% | 49% |

| Interest rate | 7.5% | 10.5% |

| EMI accounting for interest rate | 20,542 | 44,552 |

| EMI as % of monthly salary | 46% | 61% |

| Figures in Rs | ||

• After a steep rise in affordability from the mid-1990s up to 2004, the net impact of higher property prices and costlier home loans overtook the gains of higher income

• With growth rate in property prices slowing and interest rates likely to fall, affordability is likely to remain constant in the next 2-3 years

• But be prepared for periodic fluctuations in EMI amount or tenure of your home loan as interest rates move up and down

• Try and part pre-pay loan periodically, especially when interest rates rise

• If you are facing ?grent or buy?h dilemma, consider buying a basic house now (less than your dream home)

• Given the ease and variety of property loans, you can upgrade your house later.either by improving the same or by selling it to buy something bigger and better