SSKI India Research is very bullish on the pharma sector: “The Indian pharma sector is poised to turn a corner on the back of excellent growth in first nine month of 2006-7. The midterm growth prospects remain intact on continued momentum in generic exports, domestic recovery and scaling up of contract research and manufacturing services (CRAMS). Enhanced focus on non-regulated markets is enabling companies to manage pricing challenges in developed markets. We expect strong revenue growth, and scale effects, to cause margin expansion. However, higher R&D costs and M&A related charges may impact near-term profitability. We upgrade our sector stance to ‘Outperformer’. Sun, DRL, NPIL and Dishman are our top picks.

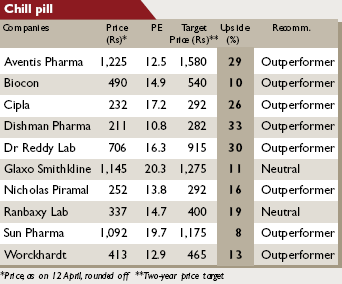

Sun Pharma: Sun’s strategy of growing its Indian and US businesses is yielding good results. While focus on chronic segments is driving the domestic business, abbreviated new drug application (ANDA) filings are a platform for the US business. Valuations of 23.8 times 2007-8 consolidated earnings remain attractive. ‘Outperformer’ with a price target of Rs 1,175.

Dr Reddy Labs: DRL follows a strategy of investing heavily in discovery R&D and building a diversified global generics business. DRL is building capabilities in biologicals and specialty drugs. Valuations of 18.6 times 2007-8 earnings are attractive. ‘Outperformer’ with a price target of Rs 915. DRL is our top pick.

Nicholas Piramal: NPIL’s growth strategy involves partnering global innovators for custom manufacturing services (CMS). NPIL has unique capabilities across the formulations value chain. CMS revenues will exceed $200m in 2006-7. We see accelerated growth. We estimate 24% CAGR in revenues and 48% CAGR in earnings over 2006-09. Maintain ‘Outperformer’ with a price target of Rs 292.

Dishman Pharma: Dishman focuses on contract manufacturing of patented drugs and is among the leading CRAMS players. We expect 47% CAGR in earnings over 2006-09. Maintain ‘Outperformer’ with a price target of Rs 282.

Cipla: We estimate a 28% CAGR in Cipla's earnings over 2006-09, driven by higher formulation exports. We do have concerns on a potential slowdown in exports. However, valuations of 20.3 times 2007-8 earnings are attractive. ‘Outperformer’ with a price target of Rs 292.