There's a saying among savvy investors: Be greedy when others are fearful, or buy when others are selling. Despite the stock market mayhem, this may be the right time to buy. But you have to be careful and choosy. Here’s why experts feel that the 10 stocks mentioned below can offer attractive returns over the next 2-3 years.

For one, their valuations are at mouth-watering levels. Take ICICI Bank’s market cap, which is less than its current net worth, or Bhel, which has enough orders to keep the company busy for the next 4-5 years. So there are hidden opportunities to exploit in this ‘depressive’ market. The micro-fundamentals of these companies have not deteriorated, only their share prices have tumbled.

Secondly, you can now buy more for the same price. These 10 stocks are likely to lead the rally when the market recovers. During the bear market in 2000, Larsen & Toubro lost 60% of its value, but the investors who picked up the stock at those levels would have gained 16 times had they sold off the shares a few weeks ago. So if you have money and the guts to play the markets now, go for it. But at your own risk.

ICICI BANK

ENAM: TARGET PRICE RS 800

>> Fee income likely to grow at 25-30% in coming quarters.

>> Cost-cutting measures expected to help bottom line.

>> Fall in G-Sec yields to help recover marked-to-market losses.

IDFC SSKI: TARGET PRICE RS 930

>> Growth in current & savings accounts ratio will be the key.

>> Once the bank shows restraint in growth, the change in investor sentiment will lead to re-rating of the stock.

PRABHUDAS LILLADHER: TARGET PRICE RS 615

>> Current share price already discounts maximum possible defaults in foreign investment portfolio.

>> Stock trading at record low of 1.0 times 2009-10 book value.

IIFL: TARGET PRICE RS 910

>> Q2 profits grew 77% without material rise in bad debts.

>> Raising profit growth estimates by 4.4% to 39% despite an expected slowdown in the second half of the current year.

PRABHUDAS LILLADHER: TARGET PRICE RS 850

>> 91% jump in Q2 fee income has been a positive surprise.

>> Net non-performing assets as a percentage of net customer assets stabilised at 0.43% against 0.47% in previous quarter.

MOTILAL OSWAL: TARGET PRICE RS 973

>> Post-Q2 results, we increase earnings estimates by 11% for 2008-9 and by 4% for 2009-10 financial years.

>> Strong asset quality—high rated loans up from 78% to 84%.

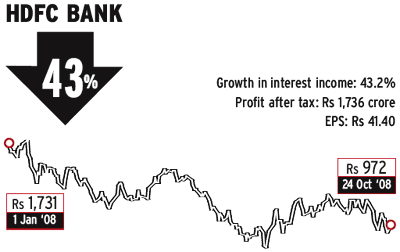

HDFC BANK

IDFC SSKI: TARGET PRICE RS 1,385

>> Earnings expected to rise by 38% on strong core income.

>> Stock quoting at attractive valuation of 2.8 times 2009-10 estimated adjusted book value.

MOTILAL OSWAL: TARGET PRICE RS 1,400

>> Strong loan growth with greater emphasis on the retail segment and high fee income will aid earnings growth momentum.

>> We expect RoA to remain high at 1.3-1.4%.

MACQUARIE RESEARCH: TARGET PRICE RS 1,439

>> High interest rate will help maintain NIMs at above 4%.

>> Over the medium term, the current and savings accounts ratio should improve marginally.

CENTRUM RESEARCH: TARGET PRICE RS 1,030

>> Bharti’s core strategy of enhancing network coverage and strengthening rural reach will help sustain its position.

>> Bharti Infratel and Indus Tower will be key catalysts.

ASIT C. MEHTA: TARGET PRICE RS 1,010

>> With strong earnings visibility and excellent execution record, Bharti will continue to be the market leader, with 25% market share by the end of 2009-10.

MOTILAL OSWAL: TARGET PRICE RS 1,020

>> Bharti Airtel offers highest earnings visibility in the sector.

>> Valuations at 9.9x 2008-9E and 7.9x 2009-10E EV/EBITDA are attractive considering 2-year EBITDA CAGR of around 31%.

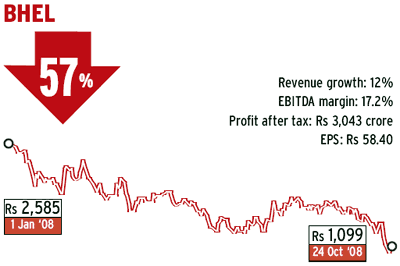

IL&FS INVESTSMART: TARGET PRICE RS 2,067

>> New initiatives like coach building, electrical locomotives and drilling rigs to help realise long-term goals.

>> The stock is trading at significant discount to our DCF valuation.

PRABHUDAS LILLADHER: TARGET PRICE RS 1,880

>> Bhel has developed 600 MW packs to compete with Chinese players, which has ensured better order book position.

>> Management doesn’t see any raw material price pressure.

IIFL: TARGET PRICE RS 2,037

>> Capacity expansion and introduction of new products makes Bhel confident of achieving revenue of Rs 45,000 crore by 2012.

>> Current order book ratio of 4.2x provides robust growth visibility.

BNP PARIBAS: TARGET PRICE RS 1,118

>> New order inflows have led to order estimate of Rs 44,300 crore.

>> Estimate 10% order growth in 2009-10. Strong order book will support 35.4% revenue growth in E&C segment in 2008-9.

IDFC SSKI: TARGET PRICE RS 1,168

>> Given its strong balance sheet, L&T is comfortably placed.

>> L&T’s diversified capabilities and multiple stream of revenues make it the largest infrastructure player in the country.

IIFL: TARGET PRICE RS 3,553

>> Operating cash flow to remain robust over 2008-10.

>> An expanding presence in West Asia should help cushion the impact of any slowdown in orders in the domestic market.

IDFC SSKI: TARGET PRICE RS 947

>> Based on Hero Honda’s strong performance and an expected volume trigger from the Sixth Pay Commission, we increase volume growth estimates to 9.8% from 6.9%.

BNP PARIBAS: TARGET PRICE RS 884

>> Increased production at Haridwar plant will help it improve margins due to fiscal benefits by the state government.

>> A 100 bps margin improvement will drive a 10% EPS growth.

IIFL: TARGET PRICE RS 920

>> In 2007-8, volume growth outpaced that of the industry.

>> Launch of the Hunk helped gain ground in premium segment.

>> Overall, Hero Honda gained more than 650 bps market share.

ICICI DIRECT: TARGET PRICE RS 1,449

>> Stock factors in all the concerns of financial turmoil.

>> The target price, according to us, is fairly reasonable considering the current uncertain environment.

INDIA INFOLINE: TARGET PRICE RS 1,259

>> The company has still not witnessed any client-specific issues.

>> This will limit any further material downside in stock price and lend stability over the next 4-6 months.

PRABHUDAS LILLADHER: TARGET PRICE RS 1,443

>> While deteriorating macro-environment, volatile rupee and management’s stand seem to urge caution, we believe the current market price captures most of these risks.

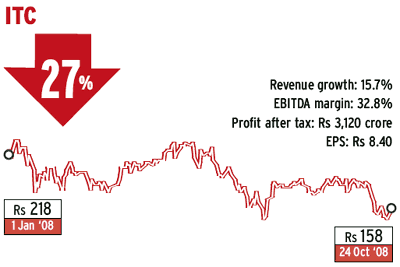

CREDIT SUISSE: TARGET PRICE RS 250

>> Recent rise in product price were well-absorbed by the market.

>> As the company is not too worried about policy environment, we expect its cigarettes business to grow by 25%.

IIFL: TARGET PRICE RS 218

>> No significant increase in losses is expected from FMCG business.

>> The risk-reward ratio has turned favourable for ITC, with likely positive surprises in cigarette volumes and FMCG businesses.

JM FINANCIAL: TARGET PRICE RS 230

>> Despite defensives being in demand, the market ignored ITC due to worries on phasing out of non-filter cigarettes. Expected losses in FMCG segment already factored in the share price.

IDFC SSKI: TARGET PRICE RS 1,566

>> Sun Pharma is our preferred business model in pharma space.

>> Visibility on Taro’s acquisition closure and its financial health on any big product launch will be key triggers for upgrades.

MACQUARIE RESEARCH: TARGET PRICE RS 1,840

>> Sun Pharma is the leader in chronic therapies at home.

>> Selective forays in profitable emerging markets will drive global expansion with margins intact.

BNP PARIBAS: TARGET PRICE RS 1,695

>> The ANDA pipeline which provides exclusive opportunities, and synergies emanating from the acquisition of Taro, are potential drivers for future earnings.