In equity investment, the risk faced by a stock can be due to internal and external factors. Internal factors are the company’s fundamentals like sales, profits and quality of management, while external factors are macro-economic issues such as regulations, currency uncertainties, etc. Internal (or unsystematic) risks can be minimised through diversification, but external (or market) risk cannot be eliminated. Market risk has significant implications as it can drive the stock prices either way in the short term. The intensity of price movement, known as volatility, is measured by a financial tool called beta. It measures the sensitivity of a stock to the overall market movement.

Valued Information

Beta analyses the market risk of a stock with respect to benchmark indices like the Nifty, Sensex and BSE 100. The value of beta can be positive or negative. If it is positive, it means the stock is moving with the market, and vice versa. For example, if the beta of a stock is +2, it implies that the average intensity of stock movement is twice that of the market. So, if the market moves by 10%, on an average, the stock will move by 20%. The value of beta is calculated by dividing the degree of association between the stock and the index (covariance) by the degree of variation within the index (variance). Variance and covariance are calculated by considering the percentage change in prices.

Best Of Highs And Lows

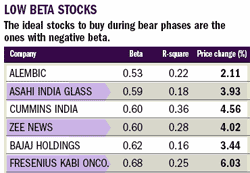

Investors should maintain an optimal ratio of low and high beta stocks in their portfolios. Stocks with a beta value of 0-1 are called low beta or less volatile stocks, whereas stocks with a beta value greater than one are called high beta or more volatile stocks. High beta stocks are suitable for aggressive investors, while conservative investors should go for low beta stocks. In a bull phase, high beta stocks can deliver high returns, but during a bear phase low beta stocks are more useful as their relative movement is less than that of the market. Though the ideal stocks to buy during bear phases are the ones with negative beta, such stocks are few in number (see tables above).

Combo Deal

If you want better results while calulating beta, always analyse it along with the coefficient of determination, also known as r-square. The value of the coefficient of determination ranges from zero to one and it shows the percentage of the total risk of a stock that is due to market-related factors. For example, an r-square of 0.6 implies that 60% of the stock’s total risk is due to market factors. The dependability of beta may be questionable unless it is accompanied by a sufficiently high value of r-square. The closer the value of r-square to 1, the higher the reliability of beta. Both these statistics are available on the BSE and NSE Websites for Nifty, Nifty Junior and Sensex stocks.