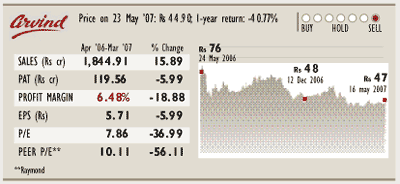

Arvind Mills Enam

Arvind Mills Enam

Securities is cautious and maintains its negative rating : “Arvind Mills reported standalone revenues of Rs 4.8 billion (increase of 35% YoY), EBIDTA of Rs 67.2 crore (declined by 26%) and PAT of Rs 40 million (declined by 85%) in Q4, 2006-7.

Volumes declined by 15% YoY to 81 million metres and realisations were down by 5% YoY to Rs 94 per metre for 2006-7.

Realisations improved to Rs 100 a metre (up 6%) in Q4, 2006-7, as the management opted out of the CENVAT scheme. We expect the supply overhang to continue and have forecasted denim realisations at Rs 93 a metre in 2007-8 earnings. Depleting low-cost cotton inventory and higher cotton costs are expected to exert pressure on margins in H2, 2007-8. The management also expects rupee appreciation to impact margins by 2-3%.

With a continuing supply glut in the denim markets and higher cotton costs expected next season, the management has guided for further margin contraction in H2, 2007-8. At CMP (Rs 45), the stock trades at 23 times 2007-8 earnings (EPS of Rs 1.9) and 12 times 2008-9 earnings (EPS of Rs 3.8). We reiterate our sector ‘Underperformer’ rating.”

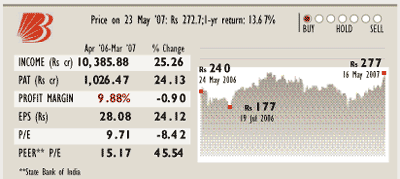

Bank of Baroda SSKI

Bank of Baroda SSKI

Capital is bullish on the PSU bank: “Bank of Baroda (BoB) has reported net profit of Rs 246 crore (17.7% YoY growth) for Q4, 2006-7. The deposit growth was 33% YoY. The reported net interest income (NII) has increased by 27.1% YoY.

Reported margins in Q4, 2006-7 have improved by 21 basis points (bps). Asset quality of BoB has improved with net NPA ratio coming down to 0.6% of March 2007. Capital adequacy is comfortable with overall CAR at 11.8% and tier-I CAR at 8.7%.

Global cost of deposits has increased by 49 basis points (bps) YoY. While reported margins are up YoY as well as QoQ, adjusting for one timers, margins are down by 13 bps YoY. With excess SLR reducing to only 1.6% and a competitive scenario in mobilising deposits, we believe incrementally, it will be difficult for BoB to protect its margins.

On back of moderation in margin expectations we have reduced our net profit estimates by 3.5% and 3.8% for 2007-8 and 2008-9 respectively. However, there could be some earning surprises coming in from higher than expected recoveries going forward. We maintain our ‘Outpeformer’ rating on the stock.”

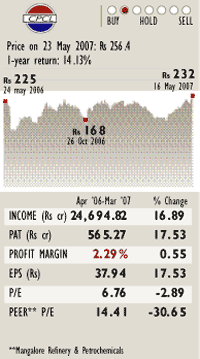

Chennai Petroleum

Chennai Petroleum

Edelweiss Securities upgrades the stock for the company: “Chennai Petroleum’s (CPCL) Q4, 2006-7 numbers were above expectations. The company’s net revenue in Q4, 2006-7 was Rs 5,720 crore, lower sequentially, mainly due to a 3.2% decrease in crude prices in Q4, 2006-7. The reported EBITDA of Rs 400 crore, up 194% YoY and 230% QoQ, mainly due to a rebound in refining margins in Q4, 2006-7.

Gross refining margins (GRMs) increased to $6.42 a barrel in Q4, 2006-7 from $ 2.65 a barrel in Q4, 2005-6 and $ 2.95 a barrel in Q3, 2006-7.

The EPS increased to Rs 12.7 a share in Q4, 2006-7 from Rs 2.4 a share in Q4, 2005-6 and Rs 1.6 a share in Q3, 2006-7, mainly due to increase in gross profit margins, which increased to 9.2% from 5.6% in Q4, 2005-6 and 4.6% in Q3, 2006-7. We estimate CPCL to report GRMs of $4.97 a barrel in 2007-8, up from our previous estimate of $ 4.23 a barrel.

We are revising our 2007-8 and 2008-9 EPS estimates upwards by 16% and 34% to Rs 34.7 a share and Rs 35.2 a share, respectively. We believe that time and cost overruns in new refinery capacity addition worldwide will help sustain GRMs.

We are upgrading the stock as at CMP of Rs 231, the stock trades at 6.7 times and 6.6 times our 2007-8 and 2008-9 EPS estimates with a 2007-8 dividend yield of 5.3%. On an EV/EBITDA basis, CPCL trades at 4.5 times and 4.0 times our 2007-8 and 2008-9 estimates. ‘Buy’.”

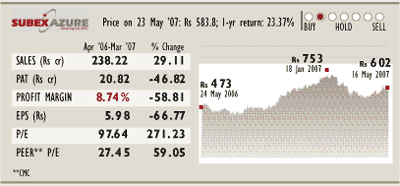

Subex Azure IL&FS

Investsmart continues to remain bullish: “Subex reported product revenue of Rs 57.9 crore in Q4, 2006-7, as against Rs 75.8 crore in Q3, 2006-7, a decline of 23.6% on account of 51% sequential decline in licensing fee.

Investsmart continues to remain bullish: “Subex reported product revenue of Rs 57.9 crore in Q4, 2006-7, as against Rs 75.8 crore in Q3, 2006-7, a decline of 23.6% on account of 51% sequential decline in licensing fee.

The company reported a loss of Rs 1.8 crore at the EBITDA level in Q4, 2006-7 as against a profit of Rs 22 crore in Q3, 2006-7 due to higher provisioning of bad debts and redundancy cost of Rs 24 crore.

However, due to forex gains of Rs 20.4 crore and deferred tax credit of Rs 15.44 crore, the net income increased by 44.4% to Rs 27.6 crore.

We expect Subex to post consolidated revenue of Rs 745 crore in 2007-8 and Rs 948 crore in 2008-9; the product division is likely to contribute Rs 620 crore and Rs 810 crore to the company’s revenue respectively. We believe that the revenue is achievable on the back of strong order backlog and order pipeline. We also expect Subex to post net profit of Rs 150.9 crore and Rs 220.5 crore in 2007-8 and 2008-9, implying an EPS of Rs 43.4 and Rs 63.4 respectively, a two-year (2007-9 earnings) CAGR of 80.6%.

Currently, the stock is quoting at 15.2 times 2007-8 earnings and 10.4 times 2008-9 earnings. We remain bullish on the stock and maintain ‘Buy’.”

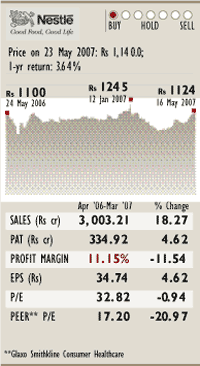

Nestle India

Nestle India

Prabhudas Lilladher is bullish about growth prospects of the packaged food MNC: “Nestle’s gross sales during Jan-Mar 2007 recorded 24.7% YoY growth to Rs 863 crore. This was on the back of a 21.3% YoY growth in domestic sales to Rs 810 crore and a strong growth of 69.9% YoY in exports to Rs 86.2 crore.

Domestic sales during the quarter has been primarily driven by strong volume growth. Additionally, higher realisations through price hikes and a better product mix have contributed to the sales growth. The strong growth in domestic sales is being driven by innovations and higher thrust on nutrition, health and wellness.

Operating margins improved by 92 basis points (bps) to 20.7% against our expectations of 20%. Led by strong growth in sales and improvement in profitability, PBT during the quarter grew by 36.2% to Rs 168 crore. However, PAT has witnessed a 17.5% YoY growth to Rs 86 crore against our expectations of Rs 88.7 crore. This could be attributed to the higher effective tax rate.

Nestle has commenced Jan-Dec 2007 with a strong performance during Jan-Mar 2007. Through stronggrowth in volumes, Nestle has overcome the continuing pressure from input cost and has improved its profitability. We have revised our EPS estimates for Jan-Dec 2007 and Jan-Dec 2008 by 2.9% and 2.7% respectively to Rs 42 and Rs 48.3.

At the CMP of Rs 1,070, the stock is trading at 25.4 times Jan- Dec 2007 earnings and at 22.1 times Jan-Dec 2008 earnings. We thus continue to maintain ‘Outperformer’.”

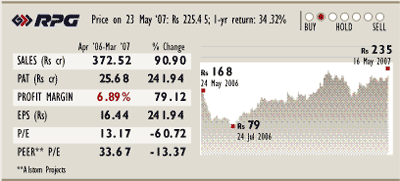

RPG Transmission

Edelweiss Securities maintains a buy rating on the transmission firm: “RPG Transmission (RPGT) declared impressive Q4 results with profitability positively despite subpar revenue performance.

Edelweiss Securities maintains a buy rating on the transmission firm: “RPG Transmission (RPGT) declared impressive Q4 results with profitability positively despite subpar revenue performance.

Q4, 2006- 7 revenues were up by approximately 4% YoY at Rs 1 crore (Rs 370 crore for 2006-7). EBITDA was up by approximately 9% YoY, at Rs 11.9 crore (Rs 42.7 crore for 2006-7), while net profit was up 166% YoY, at Rs 10 crore (Rs 25.7 crore for 2006-7) for the quarter.

RPGT’s at-par capability with sector peers in terms of pre-qualifications and a robust macro scenario is likely to drive strong revenue growth at a CAGR of approximately 33% from 2007-9 earnings.

Revenue growth and enhanced profitability coupled with improving working capital metrics and low capital expenditure are likely to result in positive free cash flow and improving return ratios leading us to repose faith in the company’s growth and earnings.

We are increasing our net profit estimates by 13% and 2% to Rs 33.7 crore and Rs 42.6 crore in 2007-8 and 2008-9, respectively, on account of significant improvement in margins. On our EPS estimate of Rs 22 and Rs 27 for 2007-8 and 2008-9, respectively, RPGT trades at a P/E of 10 times and 8 times, respectively. We continue to maintain our ‘Buy’ recommendation.”