Six trading sessions is all it's taken the BSE Sensex to hop, skip and jump from 16k to 17k! While I am convinced about the India story, I must also confess that I have been left breathless by the sheer momentum. As your money manager, I am faced with a predictable dilemma: is this time for caution or euphoria?

The estimated Sensex EPS for 2008-9 is Rs 950-1,000 per share, which implies that the market is trading at a one-year forward P/E multiple of 18 times already. It’s 18 months to March 2009, really. Should I get cautious or should I join the euphoria (and run the risk of investing at an intermediate peak)?

For one, there’s no denying the momentum: FIIs investments are in an overdrive, rising rupee will make imports cheaper and unleash a fresh round of consumption. Government finances are better, interest rates seem to have peaked and infrastructure spending will further accelerate.

For one, there’s no denying the momentum: FIIs investments are in an overdrive, rising rupee will make imports cheaper and unleash a fresh round of consumption. Government finances are better, interest rates seem to have peaked and infrastructure spending will further accelerate.

However, IT is sputtering under currency pressures and wage hikes. Earnings and P/E contractions are likely, and can wipe out market cap when they work in tandem. Not only IT and ITeS, all export-led businesses (textiles, gems and jewellery, engineering, automobiles, pharma, chemicals, ores and metals) will come under pressure.

It’s in these perplexing and challenging conditions that we have taken some bold and some cautious actions for our model portfolios.

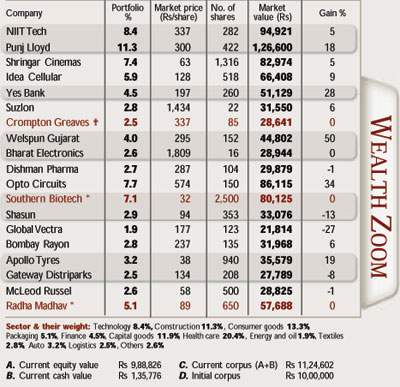

In Wealth Zoom we have actually bought two new items, both apparently risky small-caps. These are the two stories where your fund manager’s allegedly superior research may prove itself: Radha Madhav and Southern Online Biotechnologies.

The first named has a small balance sheet size (a shade over Rs 100 crore), and is into multi-layer packaging films and solutions for the FMCG industry. It went public in late 2005 at Rs 20 per share, and did not really achieve much by way of reported financials till the quarter ended June 2007, when topline and margin both went ballistic.

More interestingly, this “small” company is investing over Rs 170 crore into pharma packaging that promises to ramp up revenues from Rs 150-odd crore annually into the over Rs 400-crore league. The money has been raised at Rs 63 per share already. And if margins stay around the 25% levels seen in the June quarter, we might have a big winner on our hands.

Southern Online Biotech is a similar story, arguably at an earlier stage. This is a small, insignificant ISP company that is barely breaking even for the past four years. It has done what many others are only creating slide shows for: it has set up a bio-diesel plant!

In fact, this initial 40 kilolitre per day capacity is already operating in fits and starts, some 60 km outside Hyderabad.

The big whammy might well come from its seven times expansion at a greenfield location, details of which are yet to pan out. We’ve added 2,500 shares of this Hyderabadi gem to your Zoom portfolio, working out to 7 per cent of the portfolio.

On the sales side, we’ve sold Valecha Engineering at Rs 300.95, not terribly enthused by its rather opaque annual report and muted 2006-7 numbers. An uninspiring 1:2 bonus announcement has not lifted sagging spirits in this counter. We earned more than 25% on this trade, and were happy to get out.

With close to 40% return in three months, we have reduced our holding by half in Crompton Greaves. On the other hand, we’ve sold all our 72 shares in Northgate. This might look like bad timing but the IT sector is facing strong headwinds.

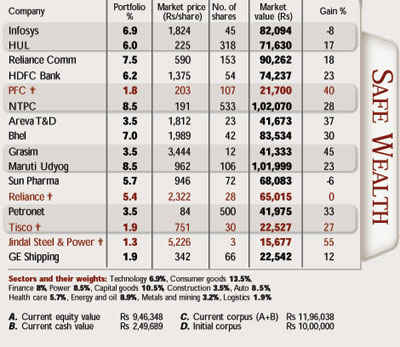

The large-cap bias in the market uptick has been partly captured by Safe Wealth, and it has done much better than Wealth Zoom. It is here that our selling is a little more widespread.

We’ve finally closed our position in GMR Infrastructure, where our last 27 shares have given us a 47% returns in just over 90 days! And since our top pick Reliance has gained 39% in the same period, prudence demands that we sell 20 of the 48 shares that you saw on last week’s scorecard. Reliance is now a relatively safer 5.4% of Safe Wealth.

Tisco, Jindal Steel and Power Finance are the three other counters where we have chosen to book partial profits, by selling around half our holdings in them. While we believe in the long-term viability of these businesses, we feel that the recent run up is a little bit of a blowout.

Last fortnight we ran out of space for reviewing our picks in energy/oil, metals, textiles, auto, logistics and chemicals (others). Our decision to prune the portfolios has resulted in this exercise being postponed again. Gather your ideas in these sectors and share them with us.

-Dipen Sheth