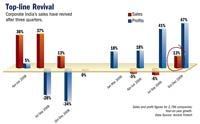

Corporate India has delivered what its peers in the developed world could not—growth. While companies in the US and Europe struggle to sustain sales and revenues, Indian companies have resumed double-digit growth rates. The trend is clearly visible in the recently declared third quarter (October-December) results. Based on the results of 2,796 companies till 4 February, the year-on-year sales, on an average, went up by 13.2 per cent. This may not seem like a high figure in normal times, but it is the first time in 2009 and the current financial year that these companies have reported a positive growth in sales (or top line). The profit for the same set of companies registered a robust growth of 47 per cent.

To put things in perspective, we need to consider the performance of corporate India in the recent past. Things had started deteriorating in January 2009, when economic activity slowed down and companies struggled to sustain sales and revenues. This continued till September, forcing companies to cut costs and rationalise operational expenses. Though these measures helped them improve their efficiencies, sales remained constant or fell in some cases. The same universe of 2,796 companies saw a sales de-growth of 6.4 per cent in the July-September quarter.

The trend reversed only after nine months (in the October-December quarter). Increased government spending and a revival in economic activity helped the companies arrest falling sales and, therefore, improve revenues. "After three quarters of disappointment, things are finally looking up, as there has been a concerted recovery in top-line growth," says Kunj Bansal, CIO, Sanlam Investment Management.

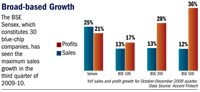

The fact that the 30 blue-chip companies comprising the BSE Sensex have also seen their sales grow by an average of 25 per cent proves that this performance is not a flash in the pan. The last time these companies saw such a sales growth was in the July-September quarter of 2008. "Most of the results met the expectations in the case of the Nifty companies; earnings growth was around 19 per cent and margin expansion was also visible," says D.D. Sharma, senior vice-president, research, Anand Rathi Financial Services.However, this recovery is not as broad-based as one would have expected. Most experts claim that it is only sectoral. Between 8 January and 6 February 2010, when the 2,796 companies declared their results, the benchmark Sensex lost 1,624 points or 9.3 per cent. This was due to the subdued performance of some key momentum sectors such as telecom, engineering and banking. "The results are a mixed bag. Although the aggregate earnings growth was as anticipated, a large number of companies did not meet our expectations," says Bansal. The foremost were telecom, pharmaceuticals, real estate and capital goods companies.

The performers

IT companies, which were not expected to perform well, surprised everyone with a good set of numbers. The three biggest players, TCS, Infosys and Wipro, reported a strong sequential growth in revenues and profits. Adding to the good news, the managements of all three companies have confirmed a positive business environment and expect better business in the coming quarters. In a recent statement, Azim Premji, chairman of Wipro, said, "We have seen a positive demand environment, which has driven a broadbased sequential growth across all our verticals, service lines and geographies. In 2010, we expect IT budgets to be flat or marginally positive."

Auto and auto ancillary industries were also among the star performers. Buoyed by low interest rates, as well as competition in the auto loan segment, and low raw material costs, companies like Maruti Suzuki, Hero Honda and Bajaj Auto registered a robust growth in sales and profits. Maruti Suzuki, India's largest passenger car maker, saw a 62 per cent jump in net sales and a 15.1 per cent growth in operating profits in the third quarter.

The laggards

Sectors like telecommunications and pharmaceuticals disappointed with a subdued performance. At a consolidated level, both Bharti Airtel and Reliance Communications saw a de-growth in revenues due to stiffer competition. While Bharti Airtel's gross revenues fell by 0.7 per cent on a sequential basis (QoQ), Reliance Communication's net revenues dropped by 6.8 per cent. "The telecom sector is witnessing intense competition due to the launch of services by new players. The pressure on tariffs and average revenue per unit is expected to continue in the next few quarters," says Amit K. Ahire, an analyst with Ambit Capital.

In the pharmaceutical industry, Dishman, Divis Laboratories and Sun Pharmaceuticals couldn't live up to expectations. Both these companies reported a 21-26 per cent drop in revenues. Sun Pharmaceuticals failed to enthuse investors due to the weak business reported by its subsidiary in the US.

Will the good times last?

Though the much-awaited pick-up in business seems to have begun (at least for some core sectors), analysts are concerned about the sustainability of this growth and margins. In most of these sectors, companies managed to pass on the rise in input costs to consumers without squeezing their margins. However, as industrial production gathers pace, commodity prices and interest costs are expected to rise further. This will increase the pressure on margins, but companies cannot increase prices indefinitely.

"In most cases, the healthy topline was due to the rising final product prices. Volume growth wasn't better except in the auto and cement sectors," says Sharma.

High interest costs are expected to impact small companies more than their bigger peers as the latter can raise low-cost funds through qualified institutional placements, external commercial borrowings and foreign currency convertible bonds. "We remain positive on the earnings front and the top-line will be robust, but managing the costs will be a key challenge," says Ashu Madan, president, equity broking, Religare Securities.

Another concern haunting analysts is the sustainability of growth in sales. While IT and automobile companies have reported good numbers, the sectors driven by domestic consumption, such as banking and capital goods, are yet to see a concerted recovery in earnings. "We believe that the current downtrend (correction) in the markets is due to concerns of slowdown in the overall growth momentum because of tightening interest rates," says Sarbjit Kour Nangra, vice-president, research, Angel Broking.

In fact, biggies like the State Bank of India (SBI), which is India's largest lender, and engineering firm Larsen & Toubro (L&T) also turned up discouraging figures. Due to the poor performance of its engineering and construction unit, L&T's standalone net sales went down by 6.1 per cent, while SBI saw its interest income decline by 1.4 per cent compared to the previous year. On the bright side, most analysts expect the current underperforming sectors (banking, pharmaceuticals and capital goods) to jump on to the growth bandwagon in the fourth quarter.

The macro-economic scenario is challenging for the corporate sector, with rising bond yields and an uptick in commodities. Both these factors are likely to squeeze margins and dent the corporate earnings growth rate.

After a stellar performance in 2009 (Sensex was up 81 per cent), analysts expect the markets to take a breather in the first half of 2010. Says Ashok Jainani, VP, research and market strategy, Khandwala Securities: "Inflation has reached a level where it threatens demand generation. In this situation, it is difficult to expect the market to repeat its 2009 performance by doubling in the new year. Unless these challenges are overcome, the Sensex is likely to remain in the range of 14,900 and 19,500 in 2010."

The bottom line for investors: wait for the next quarter's results for a confirmation on the pick-up.