The past 12 months have seen the worst drop in the Indian stock markets. This, then, is obviously the wrong time to talk about the next bullish phase. So why are we doing it? The answer is simple. Most analysts feel that the current bear phase may be over by the end of 2009, or early 2010. Which is why you need to be in the right frame of mind to ride the coming bull wave. But are you sure that the upturn will follow the predictions of the experts? What if it starts earlier, say, by August this year? Or later, only in the second half of 2010?

Year | Rise in the Sensex |

|---|---|

Jan ‘91-Apr ‘92 | 215% |

Aug ‘93-Sep ‘94 | 69% |

Oct ‘98-Feb ‘00 | 58% |

May ‘03-Jan ‘04 | 109% |

So you have three options. One is to sit quietly with your decimated portfolio and pray for the good times to return quickly. Two, follow the oft-given advice these days. "If you believe the world doesn't end that often, and good companies don't disappear, I think it is actually a good time to invest," says Amitabh Chakraborty, president (equity), Religare Capital Markets.

What's the third choice? Read this cover package carefully. Historically, a mix of micro and macro indicators has influenced stock market movements. There may be no cause-and-effect link between these factors and the rise in the Sensex. But there's a lag effect: the indicators move positively before stocks begin their northward movement. If you, as an investor, track these parameters closely, you may be in an almost perfect position to spot the next boom before others get to know of it.

Money Today presents 10 'hope' indicators to know when the current bear phase will end. Our only submission is not to be swayed by one or two indicators. Ideally, all of them, or at least a majority of them, should be pointing in the same direction. Since this recession is unique, you may not hit the bull's eye with our analysis. But you will definitely be close to the mark.

| New governments and their impact on the Sensex | ||

|---|---|---|

| 6 months | 1 year | |

| 21 June 1991 (P.V. Narasimha Rao) | 37.57 | 126.28 |

| 31 October 1984 (Rajiv Gandhi) | 44.49 | 77.8 |

| 22 May 2004 (Manmohan Singh) | 16.41 | 27.65 |

| 14 January 1980 (Indira Gandhi) | 3.01 | 20.4 |

| 1 June 1996 (H.D. Deve Gowda) | -26.08 | NA |

| 21 April 1997 (I.K. Gujral) | -0.35 | NA |

| 19 March 1998 (A.B. Vajpayee) | -19.11 | -3.88 |

| Figures are the percentage change in the Sensex after the swearing in of the new government; Market data: Capitaline | ||

Since 1980, each time that a seemingly stable government has come to power, the Sensex has invariably zoomed within the first 12 months. In some cases, the gains have been spectacular: as high as over 125%, as was the case in 1991, when the Congress came to power. Even when the late Rajiv Gandhi assumed office in 1984 with a huge majority, the BSE index rose by 45% within six months, and by nearly 80% in a year’s time. Maybe it’s just the ‘Congress’ effect because the Sensex rose again in 1980 (late Indira Gandhi assumed office) and 2004 (Manmohan Singhled UPA came to power).

Obviously, when investors felt that a weak coalition was in control of the economy, as was the case with V.P. Singh in 1989, and the Deve Gowda-led United Front government in 1996, they gave the stock markets a thumbs down. The only exception in the past three decades has been in 1998 when the NDA took charge and completed its full term.

The Sensex moved down during the 1998-2004 phase, but this may have been caused by a series of negatives such as the international sanctions after the nuclear tests at Pokhran (1998), the Kargil war (1999), and the bursting of the dotcom bubble (2000).Clearly, the markets are energised by a government that is more likely to last for a five-year tenure.

However, the markets do react to mid-term policy decisions. For instance in May 2004, when investors realised that the UPA was unlikely to privatise the PSUs, they pushed the Sensex down by 11.1% over the weekend (14-17 May). Similarly, when the annual budgets have been growth-oriented, as was the case in 1992 (Manmohan Singh was the FM) and 1997 (P. Chidambaram delivered the ‘dream’ budget), stock prices shot up smartly.

With elections less than two months away (April-May 2009), it is time for the investors to figure out the stability of the new government. If a strong Congress-led coalition wins, the Sensex may go up again. The BJP-led NDA may also have the same effect. In the end, it will depend on the impact the policymakers have on the GDP growth.

A consistent GDP growth of over 6% and a rising index of industrial production (IIP), coupled with the expectations of their sustainability in the near future, are likely to push up the stock markets. Explains Saurabh Mukherjea, head of Indian equities, Noble: “The recovery in stock prices is not expected until there is a pick-up in the annual GDP growth rates. If we look across 10-, 15-and 20-year time scales, we find that the markets fail to recover as long as the GDP growth stays below the 6% mark.” So, in case we witness around 6% growth during this fiscal, as has been predicted by leading Indian and foreign analysts, this parameter may become a crucial one in influencing the timing of the next boom.

| Why GDP and IIP matter | |||

|---|---|---|---|

| Two years of rising GDP and IIP, especially a GDP growth of more than 6%, left its impact on the bourses in 2003-4 when the Sensex gained 81% after two years of losses. | |||

| Year | GDP growth | IIP growth | Sensex returns |

| 2001-2 | 2.68 | 4.35 | -2.72 |

| 2002-3 | 5.76 | 5.81 | -12.90 |

| 2003-4 | 6.94 | 8.52 | 81.46 |

| 2004-5 | 8.37 | 7.45 | 13.10 |

| 2005-6P | 8.19 | 9.40 | 70.78 |

| All figures in %; Sources: RBI, CSO and Capitaline | |||

In the recent past, the IIP figure dipped by 2% in December 2008, which was the largest contraction since February 1993, and the second time in the October-December period. Predicts Robert Prior-Wandesforde, senior Asian economist, HSBC: “Looking ahead, we can expect at least another couple of months of industrial contraction, with the overall GDP growth also set to soften further in the first half of 2009, eventually falling below 6%.” He, however, feels that the second half of this year is likely to be better, when factors such as fiscal easing, dropping of commodity prices, additional oil and gas output and regional trade recovery, among others, begin to impact the Indian economy positively.

According to Rohini Malkani, economist, Citi India, “Given the coming general elections, the government will be coming out with an interim budget, instead of a regular one. One can safely say that the poor economic data will be used as a reason for additional spending or tax cuts.” Therefore, the policies of the new government will be crucial for the IIP and GDP turnaround. This can happen only if we have a stable government that comes to power and lasts for at least four years.

In some cases, the economic growth can take place despite inaction on the part of the government. For example, good monsoons and high agricultural productivity have the ability to add several percentage points to the GDP growth rates. In fact, India has mostly seen higher growth only when agriculture too has done well. Similarly, once the contribution from the services sector grows, as it has done in the past, the dependence on manufacturing and agriculture will reduce further. This will aid growth since the services sector is likely to expand in a new consumerist India.

But even if there’s a resurgence in macro indicators such as IIP and GDP, the investors will have to analyse the data for India Inc’s quarterly results before making up their minds to invest additional amounts in the country’s stock market.

Past data suggests that unless 70% of the companies in the BSE 500 universe deliver positive growth in net profits for six to eight quarters, market sentiments remain depressed and bearish. More importantly, since the 30 Sensex stocks comprise nearly half of the BSE’s overall market capitalisation, the earnings growth of these large caps has to be in double digits over several quarters for a sustained bull run. Obviously, the expectations for the next couple of fiscals need to be encouraging. For a long-term investor, this implies that the country’s GDP will have to continue to grow at a frenetic pace for at least two-three years, and that the growth has to be more secular in nature.

This is what happened in the previous bull period (2003-7). Almost every company posted positive quarterly results. Analysts were gung-ho about high double-digit earnings growth over the next six-eight quarters. Despite the markets discounting future earnings, Indian PEs still looked attractive for a long time, especially when they were compared with those in other emerging markets. It was only in 2007, when the Sensex rose sharply from 13,942 to 20,286, a growth of 45%, that there were murmurs about a bubble in the making in the Indian markets. Anyway, the global recession pricked it.

Today, the expectations are optimistic for 2009-10. Three sectors—auto, pharma and petrochemicals—which are expected to show a negative growth in net profits in 2008-9, may show positive rates in the next fiscal. Several other sectors, such as construction and consumer goods, will maintain high growth rates in 2009-10. This, say experts, will almost double the combined PAT of the Sensex stocks from 3.9% in 2008-9 to 7.5% in the next year.

Therefore, it seems that investors should track the quarterly results from the third quarter of 2009-10. These results will tell them which stocks are likely to show an upsurge and also whether the current bearish period is about to end. If, as we said earlier, a higher percentage of the BSE 500 universe shows exceptional growth rates, it will hint at the beginning of the next boom. However, optimistic investors will want to compare indications from the quarterly data with what is really happening in the capital goods sector.

Moving quarters

In the first phase between June 1998 and March 2000, when 70% of the BSE 500 companies had a profit growth, the Sensex rose by 107% from October 1998 to February 2000.

When 73% of the BSE 500 companies posted a profit growth from June 2003 to March 2004, the Sensex rose by 100%.

When 79% of the BSE 500 companies posted a profit growth from June 2004 to December 2007, the Sensex gained 362%.

The one sector that participates in almost every boom is capital goods. When the BSE Capital Goods Index clocks an annual growth of over 10%, it is normally succeeded by an overall gain in the stock market. As the bull run picks up steam, one other sector takes over from capital goods to sustain the rally. In the late 1990s, it was the IT sector, which was finally seen as a major catalyst to spur all stocks to dizzying heights. In the previous bull phase, the financial services sector took the Sensex to an unbelievable 21,000 points.

Why is the capital goods sector so critical? One, its growth proves that corporates have started investing in building new capacities, which signifies that firms envisage a growth in demand in the future. Two, investors get attracted to these stocks initially as they find it more comforting to invest in them because of the long-term growth that such companies can deliver. To cite an example, if a capital goods company has an order book-to-sales ratio of 2.5:4, it means that the company can maintain an annual growth in revenues of 30-40% over the next two-three years, even if it doesn't get any fresh orders. Says Raamdeo Agrawal, joint managing director, Motilal Oswal Securities: "One should take a long-term view for this sector. If these companies are growing at a higher rate, they are bound to command high multiples, which seems justified from a perspective of two to three years. Besides, these companies offer a greater earnings visibility."

Obviously, the growth of the capital goods sector is also closely linked to the economic surge. When the economy expands at over 6%, capital goods are bound to grow at high rates. Moreover, a huge chunk of the GDP growth is contributed by asset formation, which results in the capital goods index outperforming other indices, such as the FMCG and healthcare. In a bear phase, the government too tries to prop up capital goods through several incentives to aid growth.

Capital gains

Between Jan ’03 and Oct ’03, the BSE Capital Goods Index led the growth, with the Sensex lagging on growth by a month. Again between Aug ’05 and Mar ’06, the BSE Capital Goods Index was trailed by the Sensex, with a lag of over two weeks.

To find out what's likely to happen in the near future, consider the EBITDA earnings of the power equipment segment in 2009-10. It is estimated to jump from 11.2% in 2008-9 to nearly 40% in the next fiscal. Net profits are projected to increase from 14.3% in 2008-9 to 32.9% in 2009-10. Such figures should propel investors to think about investing in capital goods stocks, and also have faith that the Indian stock market will rebound at least by end-2009 or early 2010. But this has to be backed by low inflation, which helps the growth in savings that contribute significantly to future capacity additions.

There is an inverse relationship between inflation and the stock markets. As the growth in prices goes down, it provides a boost to equities. This has been the case in several of the past bull runs. There are many theoretical reasons as to why this happens. As inflation weakens, it improves the sentiments because people feel they have more money to spare and, hence, look for riskier investment opportunities like stocks. If low inflation goes hand-inhand with a high GDP and IIP growth, it may actually increase the disposable income all around, which may eventually be invested in equities.

Lower inflation also impacts interest rates, which are bound to come down in such a scenario. Lower interest rates spur individual consumption, thereby resulting in a higher demand for goods and services. It also helps the corporates to borrow for financing their expansion. The result: both individuals and firms overleverage themselves, resulting in an irrational exuberance, which is also reflected in stock indices. This is exactly what happened in the previous bull phase.

The opposite is true when inflation goes up. It forces the policymakers to clamp down on money in circulation. This was the case when inflation rose from 3.51% in September 2007 to 12.29% in October 2008. The steps usually taken by RBI during such a period include raising the repo rates (the rates at which banks borrow from RBI), hikes in the cash reserve ratio and a reduction in the rate of interest on cash deposited by banks with RBI. These moves are aimed at pushing banks to raise lending rates and reduce credit disbursal. Such measures are expected to suck out money from the system and control inflation.

from the system and control inflation. However, investors should remember one thing. Low inflation should lead to higher savings. These savings, after being put aside in traditional and safer avenues like bank deposits, insurance and pensions, and purchase of physical assets (house), should be used to buy stocks. Therefore, only after the inflation falls and savings rise, there is an expected boom in stock markets. So, investors can check the manner in which these two indicators are moving to find out if money can flow into the stock markets. Obviously, FII inflows shouldn't be forgotten as they constitute a major 'liquidity' driver for any boom to sustain over a period of few years.

| Saving for growth | ||

|---|---|---|

| As savings rise over 20% for successive years, the Sensex starts to gain as it did during the period between 1987-91 and 2002-7. | ||

| Year | Net domestic savings growth (%) | Sensex growth (%) |

| 1987-88 | 35 | -21.94 |

| 1988-89 | 23.54 | 79.13 |

| 1989-90 | 24.71 | 9.45 |

| 1990-91 | 30.41 | 49.54 |

| 2002-3 | 29.65 | -12.11 |

| 2003-4 | 36.11 | 81.31 |

| 2004-5 | 24.11 | 17.44 |

| 2005-6 | 26.37 | 73.75 |

| 2006-7 | 18.67 | 15.89 |

Savings growth of over 20% for at least two years in succession leads to a bull rally. If the savings rate remains high for the next two years, the boom can be sustained. For instance, in 1987-88, when savings rose by 35%, the Sensex showed a negative return. But as the former remained buoyant in the next year, the BSE Index was up by nearly 80%. The rally continued with a few blips for the next two years. Similar was the case in the period between 2002-3 and 2006-7. Obviously, at some critical stage, the high savings find their way into the stock markets.

As a nation, we are more of savers than investors. So when we have a certain surplus due to lucrative job opportunities and prospects of higher GDP growth rates, we opt for financial and physical savings. According to RBI figures, in the period between 2002-3 and 2005-6, financial savings accounted for 70% of the total household savings. This meant that most people chose banks, pensions and insurance as the first means of investment. Since 2000-1, there has been another distinctive change in the pattern of household savings. People now also prefer to save in the form of physical assets such as real estate. After traditional savings avenues, a roof over their heads is next in priority for most households.

It is only after these objectives have been fulfilled, and if the individuals are still left with a surplus, will they look at riskier stocks and mutual funds. But once they make money on the markets and get used to high returns of 30-40% a year, a major portion of their disposable income finds its way into equities. It is common sense that the savings growth will definitely precede a rise in the stock market and, over time, will further add to the boom.

As time passes and a bull rally begins to take concrete shape, the rise in savings is helped by other factors. Some experts reckon that the inflows of FII money could be reflected in savings, as a portion of it could be lodged with Indian banks before being invested in equities. Another major contributor to savings in such a scenario is private corporate savings, as the increase in demand due to high GDP and IIP growth rates helps the corporates to show larger profits. Thus, more and more money is invested in buying stocks-by individuals, Indian corporates and foreign institutions-leading to a sustained bullish run.

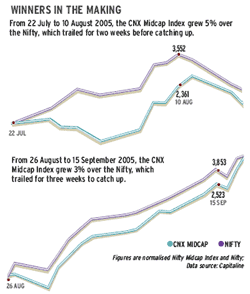

However, while FIIs and corporates turn their attention to large-caps and blue-chip stocks, since they are supposed to be safer than the small- and mid-caps, individuals do the opposite. They first look at mid caps, which are affordable and less risky than the small caps. Since the volumes in mid-caps are low in a bearish phase, their prices jump up immediately due to this inflow. Generally, the mid-caps boom before the rise in the overall indices.The mid-cap rally begins first and sets the trend for the large-caps and the market indices to follow. Agrees Saurabh Mukherjea, head of Indian equities, Noble: "Historically, mid-caps have recovered first, instead of the large- or small-caps. This was the case both in India and the western markets. In the previous bull runs in India, the mid-caps have outperformed during the first year of recovery and for the entire duration of the bull market." In the periods from 22 July to 10 August 2005, the BSE's mid-cap index started to rise two weeks before the Sensex, with an over 5% difference between them.

In the US, the mid-cap stocks have performed better during the bear phases too, but this is not true for India. In the current downturn, since the Dow Jones bottom on 10 March 2008, the S&P MidCap 400 Index jumped 14.4% compared with S&P 500's rise of 5.2%. According to experts, this may be because investors realise they can get "higher octane results from the more nimble stocks", mid-cap companies can enter into more favourable contracts than the large-cap ones, and they are likely to have a greater percentage of their revenues derived from overseas operations.

Even in India, the argument in favour of mid-caps is that a smaller business can grow quicker as the economy improves because of the lower base compared with large-caps and, therefore, the returns in the case of the former can be higher. Take Infosys. The software giant doubled its turnover and profits every year for the first eight years after listing in 1993. But the growth rate slowed down to 19% in 2007-8. The growth is still impressive, but much lower than what it clocked earlier.

In addition, since the mid-cap stocks (as also the small-caps) get battered more badly than the large-caps during bear phases in India, their ability to rise at the first signs of a recovery are higher. So, if you want to get a sense of where the market is heading and where the next big idea is likely to come from, watch the mid-cap space closely.

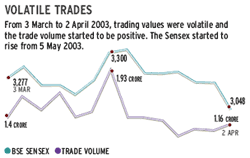

High volatility in trading volumes over several weeks can also signal that a bullish phase is around the corner. Here's what you should watch out for:

1. The growth in daily trading volumes is in double digits for at least four weeks.

2. The number of 'buy' days equal those when the selling pressure is more.

3. On 60% of the days, the market closes in the green. If all this happens, you can be confident that markets will zoom by over 25% in one month. More importantly, it could be the beginning of a bull run.

High volatility implies investor nervousness which, in the counter-intuitive world of markets, is bullish. Conversely, low volatility is a sign of investor confidence or even complacency and a warning of a downturn. Therefore, in times of high volatility, it is just a matter of time-a few months, perhaps-when buyers outweigh sellers, and market sentiments change from negative to positive. However, be wary of relief rallies, which fizzle out in a couple of weeks.

Any rally in India in recent times has generally been preceded by the beginning of a bull run in at least two countries in East Asia. The region includes countries such as South Korea, Taiwan, the Philippines, Indonesia and Singapore. If Taiwan, which traditionally attracts more inflows from foreign institutional investors (FIIs) than India, begins to trail India in terms of net foreign inflows, you can be sure that the valuations of Indian equities will go up. It may be a good idea to also observe the progress in other emerging markets that are geographically closer to the critical sources of global liquidity. For instance, institutions in the US are likely to first invest in Latin America. Similarly, the European ones will first invest in east European nations.

The reasons for this trend are two-fold. The first is that in recent times, the FIIs have fuelled the bullish phases in the country. Between 2003 and 2007, when India witnessed one of the longest rallies in history, foreigners pumped in over $5 billion. In 2008, when the markets tanked by over 50%, they withdrew a massive over $13 billion from the markets. In January 2009 too, the FIIs sucked out nearly a billion dollars from the Indian bourses. The second reason is that when the FIIs return to India after a bear phase, they do so only after they have tested the waters in more mature markets in East Asia such as South Korea and Taiwan. Therefore, India is likely to be among the last Asian markets to rise.

One also needs to look at the quality of FII money that's pouring into Indian equities. If it includes pension funds and sovereign funds, the money is likely to stay invested for a longer duration as these funds are long-term investors. If the bulk of the money is coming in through hedge funds, be a little wary as this money can vanish in a flash. Adds a market analyst: "Even for domestic institutions to get interested in stocks, the FII flow has to come in first as the general belief among the former is to trust the foreigners more than the fundamentals."

If you are a smart investor, you will also be clued into what's happening in other asset categories, especially real estate, both in India and abroad.

Little known realty statistics such as property registrations, inventory levels and discounted properties can give an idea about what's going to happen in stock markets. In the past, it was believed that when stocks rise, real estate is depressed, and vice versa. Not any longer. Now, the real estate boom happens simultaneously with a rally in stock markets. This is due to a new phenomenon witnessed in the past few years, when all asset categories (stocks, commodities, real estate and bullion) peaked at almost the same time.

The increased demand for real estate is a sign for stocks to pick up. For example, the increase in the state governments' collections from stamp duty paid on property registrations begins six months before the upturn in stock markets. Likewise, the average period for which properties remain in the market-and don't find buyers-is an important factor. Between 1997 and 2000, when realty witnessed a slump, a property remained in the market for an average of 15 months. As interest rates declined from a high of 13% in mid-2002, this average time came down to eight months. Not surprisingly, the stock market boom began in May 2003.

What influences this new linkage between realty and stocks in India is that an Indian is likely to first buy property if he has the money, and then explore the more risky option of stocks.