Retail investors often favour stocks that are established in the market. Those with lofty market capitalisations and recommended by analysts are usually preferred.

However, there are certain stocks that have the ability to outperform the market but remain obscure because their businesses are in the early stages. How does one identify such companies?

In the second part of this series on celebrity investors' strategies, we look at the one formulated by Joseph Piotroski. He gained fame for his method of selecting unpopular stocks that have the potential to become winners.

In 2000, while teaching at the University of Chicago, Piotroski came up with a highly regarded academic paper on investing.

His research focused on companies that had high book to market (B-M) ratios, that is the stocks whose book values (total assets minus total liabilities) were higher than the values (measured by market capitalisation) accredited by investors.

Joseph Piotroski He has a degree in accounting and an MBA in finance. In 1999, he joined the University of Chicago's Graduate School of Business after completing a PhD in accounting. In 2007, he left Chicago to join Stanford as an associate professor. |

However, there can be genuine reasons for a low market value, resulting in high B-M ratios. For example, investors could have shunned a stock because of a financial crisis in the company. According to Piotroski, the key is to avoid such slugs and focus on high B-M stocks.

He defines these as ones that appear in the top 20% of the market. Such stocks can be great investments because their share prices are likely to jump once the market recognises their potential.

After selecting stocks with high B-M ratios, Piotroski applies a series of balance sheet and accounting measures to choose profitable options.

The factors he uses to segregate superior stocks are return on assets (ROA), cash flow from operations, net income, debt to asset ratio, gross margins, outstanding shares and asset turnover ratio.

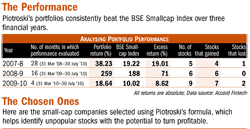

We analysed the figures for 2008-9 and found six companies, all small-caps, that satisfied Piotroski's criteria. We compared the price performance of the six-stock portfolio with the BSE Smallcap Index between March 2009 and July 2010.

If Rs 10,000 had been invested in each of these six stocks on 31 March 2009, the portfolio's value would have grown to Rs 2,15,428 on 30 July 2010. This indicates that the portfolio had an absolute growth rate of 259% compared with the 188% delivered by the BSE Smallcap Index.

Joseph Piotroski's Stock Selection Methodology

|

Piotroski's strategy has delivered market-beating returns in both our back-tested portfolios. We also tested the method using 2009-10 figures, shortlisting nine companies, and evaluating their performance between March and July this year.

As in 2007-8 and 2008-9 portfolios, the companies are small-caps. An investment of Rs 90,000 invested on 31 March 2010 would have grown to Rs 1,06,783 by 30 July 2010, an absolute return of 18.64%. The BSE Smallcap Index generated 10.02% in the same period.

In fact, five of the nine companies in the 2009-10 portfolio are turnaround firms. For example, Kandagiri Spinning Mills suffered a loss of Rs 2.6 crore in 2008-9 but recorded a profit of Rs 3.3 crore in 2009-10.

Also, Panasonic Battery India suffered a loss of Rs 9.6 crore in 2008-9 but showed a profit of Rs 7.2 crore in 2009-10.

Investments in small-cap companies are considered risky as they are highly volatile. Such stocks also witness greater speculation.

Therefore, it is extremely difficult to pick quality stocks from the smallcap universe. Piotroski's strategy not only helps pick quality smallcaps but also a portfolio that beats the market. However, he says the strategy works best for a holding period of one to two years.