Before buying any common stock, the first step is to see how money has been most successfully made in the past,” says Philip A. Fisher, pioneer of growth investing, in his acclaimed book Common Stocks and Uncommon Profits. If we look at the recent past in light of the above statement, all we feel is deep pessimism.

But go back a bit and you’ll see that it was the then relatively unknown companies that created the most wealth. We are talking of firms like Unitech, KS Oils, ICSA India, Lakshmi Energy, Areva T&D and Himadri Chemicals. Even after the recent correction in prices, these stocks, on an average, have risen 80% per year in the past five years.

It has generated an annual return of 157% in the past six years; Rs 285 (100 shares) invested in March 2003 has now increased to Rs 82,853. KS Oils has seen an over 1,000-fold rise in market capitalisation from Rs 1.43 crore in March 2003 to Rs 1,450 crore on 5 March 2009.

“Mid-caps will always do better than large caps in prolonged growth cycles. A high growth phase of economy is a good breeding ground for small- and midcap companies as it creates an opportunity for mid-cap companies to access capital and talent, and the market expands for their services,” says Manish Bhandari, vice-president and portfolio manager, equity, ING Investment Management India.

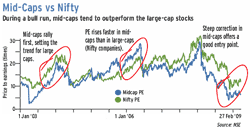

An analysis of the past bull market (January 2003 to December 2007) gives us a better understanding of the market dynamics. By the beginning of January 2003, the NSE Midcap Index was available at 12.3 times PE compared with the Nifty’s valuation of 14.9 times. As pessimism engulfed equity investors, mid- and small-caps faced the brunt of price erosion. The NSE Midcap Index PE contracted to 5.9 times while the blue-chip Nifty valuations stood at 13.3 times by March 2003.

However, as the economy moved to a high growth trajectory, smaller and medium companies were at the forefront of investor wealth creation. Consider this: from a low of 5.9 times in March 2003, the Midcap Index valuations more than tripled to 19.5 times by January 2004. In the same period, the Nifty PE rose from 13.3 to 21.2 times. The steep variation in the Nifty and Midcap Index valuations contracted as the risk appetite increased among investors.

In essence, small-cap valuations corrected the most in the last downturn (or slowing economy), while the blue-chip Nifty companies were the least affected. Improving liquidity conditions and high economic growth benefited medium and smaller companies more than their largecap peers.

This resulted in a greater expansion of mid-cap PE (valuations) than the Nifty. “Over a period of time, the probability of creating more wealth is higher in mid-cap stocks, but these stocks are like a double-edged sword. During good times they outperform by a mile, but during downturns they under-perform by a wide margin. For an investor in mid-caps, two attributes are vital: stock selection and patience,” says Mehul Shah, assistant vice-president, Sharekhan.

“If one has a two-three year investment horizon, mid- and small-cap scrips are likely to generate good returns. Invest only in high growth companies with sound promoters, which have good average daily trading volumes. Keep away from unknown promoters,” says Ranjit Kapadia, head of research, private client group, Prabhudas Lilladher. Past experience shows that not all mid-cap and small-cap companies have risen from the economic downturns. But those that do, bounce back in style.

| Small Cap, Big Profit If you can take nasty surprises in your stride and can afford to wait for the next bull market, then consider small-caps. These stocks are going at fire sale prices and are worth a look. | |

| Temptation Foods is a turnaround story. The December quarter turnover rose to Rs 231 core from Rs 36 crore a year ago; the profit after tax is Rs 12.10 crore. At Rs 27, it trades at 1.3 times its estimated annualised 2008-9 earnings per share. SKM Egg Products is a 100% export-oriented unit. The company witnessed a healthy sales growth of 41% in the past quarter and registered a net profit of Rs 5.3 crore. The ICICI Bank-promoted 3i Infotech registered a 37% rise in the third quarter in net profit to Rs 27 crore and has a healthy order book of Rs 1,420 crore. However, the slowdown in the financial services segment and high FCCBs are a matter of concern. Fag Bearings posted a 14% growth in revenue and has registered around 30% profit growth over the past five years. It made a net profit of Rs 21 crore in the third quarter of 2008-9. |