Mahin Gupta, a 30-year-old software developer in Ahmedabad, joined

the alternative economy in 2011, when an Australian company contacted his firm to create a platform based on the digital currency known as Bitcoins. He accepted part of the payment in Bitcoins, and then continued to collect them even when their value fell briefly to around $2.

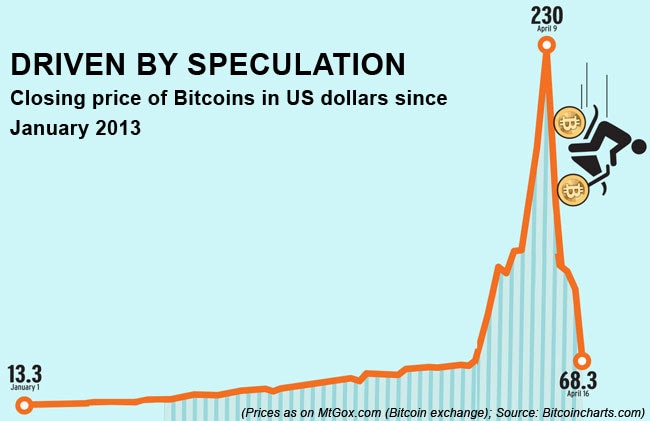

"The value of Bitcoins suffered due to scams and trades as it wasn't very mature then," says Gupta. On April 11 this year, one Bitcoin was worth around $170 (over Rs 9,200). The appreciation reflects the popularity of this highly volatile virtual currency (it was at a record $260 on April 10) in the real -world economy.

Mahin Gupta, a 30-year-old software developer in Ahme d - abad, joined the alternative economy in 2011, when an Australian company contacted his firm to create a platform based on the digital currency known as Bitcoins. He accepted part of the payment in Bitcoins, and then continued to collect them even when their value fell briefly to around $2.

"The value of Bitcoins suffered due to scams and trades as it wasn't very mature then," says Gupta. On April 11 this year, one Bitcoin was worth around $170 (over Rs 9,200). The appreciation reflects the popularity of this highly volatile virtual currency (it was at a record $260 on April 10) in the real -world economy.

For example, in March this year, Cyprus demonstrated the perils of the trust-based financial model. Deep in an economic crisis, the Mediterranean island country's government decided to take depositors' money in some bank accounts with deposits over i100,000.

Many who trusted Cyprus's banks will have no access to much of their money for an uncertain period, and may lose it all. Had these depositors used Bitcoins, they would not have been at the mercy of the government.

The Appeal of BitcoinsLaunched in 2009 by an unidentified person or group known as Satoshi Nakamoto, Bitcoins are encrypted sets of digital data representing past transactions. The open source currency, abbreviated as BTC, is powered by a peer-to-peer network similar to torrent file-sharing networks, and is in the public domain both in terms of issuing and valuation.

Its supply is distributed evenly throughout the network, grows at a rate known to all parties in advance, and can never exceed the predetermined limit. It cannot be manipulated by governments and political bodies, and cannot be inflated or deflated artificially. No central authority issues Bitcoins. All transactions are directly between the two parties involved, with no financial institution as intermediary. So transaction costs, if any, are low.

Another reason Bitcoins are popular is that payments are irreversible, unlike those made by conventional methods such as debit or credit cards. A credit card payment, for instance, can be later denied to the seller if the cardholder claims there was some fraud.

At the start of April 2012, there were some 11 million Bitcoins in existence, with 25 being added every eight minutes as on April 11, 2012. Around the year 2140, there will be around 21 million, the maximum currently permitted by the system.

The currency has seen massive user interest since March 2012, thanks in large part to Cyprus's banking crisis. The Bitcoin was worth around $100 on April 1, 2013, up from $13 at the beginning of the year. With demand rising and supply limited, the digital currency rose steeply before a crash.

"The recent surge is a sort of virtuous cycle of people talking more about Bitcoins and finding it easier to buy them," says Peter Vessenes, Executive Director at the Bitcoin Foundation, which creates standards for Bitcoins and works to promote them. "Demand so far has come from the US and Europe. Asia is less represented currently."

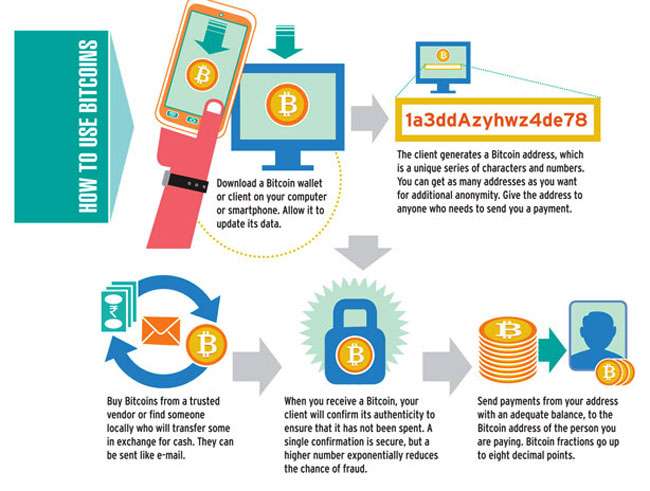

Using BitcoinsBitcoins can be broken into small units of up to eight decimal points, and are transferred like e-mail. They are used to pay for goods and services on websites that accept them. Every time they change hands, they are stamped with the transaction details and the identification key of the new owner. All transactions are communicated to the public network and indexed for future verification. Buyers and sellers remain anonymous, as the ident i f ication numbers include no personal details.

Early adopters, such as Mahin Gupta in Ahmedabad, have gained hugely. Gupta now runs a trading platform called buysellbitco.in. At the beginning of April this year, Gupta had 20 unfulfilled Bitcoin orders, as none of his contacts - some 60 people in India and the US - were willing to sell the coins.

"There are about 2,000 active Bitcoin users in India. Most of the users are individuals and want to explore the possibilities of an alternative investment opportunity," says Nilam Doctor, an Ahmedabad-based software professional who has invested in Bitcoins and also developed an online trading platform for the currency, rbitco.in.

No e-commerce websites in India accept Bitcoins, but many Indian enthusiasts use the payment system for trade of goods and services from overseas websites. Many online stores offer discounts for Bitcoin payments to increase their coin holding for future gains.

The huge demand for Bitcoins in India has largely been from speculators hoping to gain from the rising value of the currency.

How Bitcoins Are MintedIn a traditional economy, a central authority issues currency. But Bitcoins can be created by anyone by mining. It's a bit like digging for gold.

Bitcoins are small blocks of data hidden in a huge amount of irrelevant data. To get Bitcoins, one has to take the entire chunk of data, rearrange it, and process it through a set algorithmic functions - in other words, 'hash' it - until the desired result is found. The first person to find it owns the block - currently 25 Bitcoins. Luck plays an important role in solving the 'puzzle', or rearranging the raw data into the pattern that yields the right result.

You don't need to be a geek to mine. The software, freely available, does everything automatically. What you do need, though, is powerful hardware and money to pay for the power the machines consume.

Nilam Doctor, Ahmedabad-based software professional and Bitcoin investor, has developed a trading platform for the virtual currency. PHOTO: DEEPAK G PAWAR

Mining takes time and energy in terms of processing power. As mining activity increases, and as more coins are discovered, the difficulty level of mining rises. Going back to our gold analogy, the more gold we mine, the harder we need to work to extract the remaining gold.

In the early days of Bitcoins, the puzzles were easy enough for even personal computers. Until recently, Bangalore-based Bitcoin enthusiast Benson Samuel mined the currency using a botnet, or a network of computers that run applications. "I used to mine coins using GPUs," he says. He is referring to graphics processing units, or computers designed to run graphics-heavy applications such as video games. He also used personal computers. "Most of my hashing power used to come from friends' computers. I know a lot of gamers, which helped," says Samuel.

But the rising value of Bitcoins has prompted miners to use powerful computers. The puzzles have become more difficult, too, to control the number of coins that are generated. So low-powered computers now take longer to win a block, which means higher electricity costs. "We used to get a constant turnover of Bitcoins until the difficulty increased and brought in complete disinterest due to the imbalance of effort versus results," says Samuel.

He has now disbanded most of his botnets, and is awaiting delivery of a computer designed to mine Bitcoins. The computer, made by Butterfly Labs, one of the few manufacturers of specialised hardware for Bitcoin mining, uses applicationspecific integrated circuits that hugely increase its processing power and energy efficiency. Samuel says he has invested around Rs 1 lakh in the machine, and is unwilling to disclose its processing power.

"At the current difficulty level and hash rate, you need a very powerful mining hardware of more than 60 GHz (processing speed) to mine Bitcoins easily," says the Ahmedabad-based Doctor. "I know miners who have switched from Bitcoin to Litecoin and TeraCoin (also digital currencies), where mining is still easy."

On Butterfly Labs' website, a Bitcoin miner with a processing speed of 50 GHz is priced at $2,499. A 1,500 GHz miner, priced at $29,899 just before the crash on April 11, is now labelled "out of stock". Another manufacturer, BitSynCom LLC, was accepting orders for its new 65 GHz Avalon miners at 75 Bitcoins until recently.

The machines are selling like hot cakes. Based on current Bitcoin valuation and puzzle complexity, these machines can pay for themselves in a few weeks. Yes, there is a catch: once these machines start participating in mining activity, the complexity of the hash algorithms will go up.

The Dark SideDigital cryptographic currencies are new, and there are not enough regulations governing them. Mining, buying and selling Bitcoins is not illegal in India, but it is not recognised by law either, and their taxability is a question mark. "As long as you retain Bitcoins and do not convert them into rupees, it need not be included in your income," says Gupta, who launched his Bitcoin operations after consulting experts.

"The Bitcoin economy is currently a traders' paradise in India, as the coins do not attract VAT (valueadded tax) or service tax," he adds. "As a company, you just have to pay corporate tax or income tax."

Government authorities cannot track payments in the Bitcoin system. Should that free people from tax liability on income and from laws that regulate financial transactions?

"Bitcoins simply put the decision to pay taxes back in the hands of the citizen," says Samuel. "This cannot be controlled, traced or verified, but several people whom I have spoken with say they would not adopt such a currency without the consideration of 100 per cent honesty in paying taxes."

The anonymity of Bitcoin payments has led to their use for illegal activity. Money-laundering is a threat, as is illegal trade. Silk Road, an online trading website for illegal drugs, uses Bitcoins. "The drug trade from India is vibrant on Silk Road," says Samuel, adding that he has no connection with them.

Since Bitcoin transactions are irreversible, scammers and fraudsters find them useful. "People collect payments and do not deliver," says Samuel.

Monetary regulators are waking up to the reality of Bitcoins. In March, the US Financial Crimes Enforcement Network said a money transmitter's licence would be required to sell or exchange Bitcoins, although they can still be freely used to pay for goods and services.

Traditional financial institutions such as banks are yet to enter the Bitcoin arena. Bitcoin Foundation's Vessenes is optimistic that they will accept Bitcoins this year or the next. "Things are moving here, but it takes time for large enterprises to take action," he says. "Almost every large company we talk to has some internal group that loves Bitcoins and is trying to encourage their use internally. All this advocacy is great, and some of it will flower eventually."

Benson Samuel, Bangalore-based Bitcoin evangelist, says those who use the digital currency are honest taxpayers. PHOTO: DEEPAK G PAWAR

Though Bitcoins have matured substantially, the system is still experimental, and has a few aspects that can be exploited or result in a glitch. If someone could control 51 per cent of the total computing power in the Bitcoin ecosystem, for instance, they could manipulate it to retrieve the money already spent. Thankfully, such a scenario is unlikely, and playing by the rules is rewarding.

Another risk is that Bitcoin apps which serve as the backbone of the system could malfunction. Recently, an incompatibility between two versions of the mining software resulted in a company losing a lot of Bitcoins.

"There was one double-spend (Bitcoins used twice) that left a company out a bit of Bitcoin," says Vessenes. "They resolved it directly with the other party. This sort of thing is not good for the economy. Experts run most important Bitcoin companies, and it's possible that newer ones run by non-experts could face more problems."

The low market capitalisation - around $1.5 billion on April 4, 2012 - lays the system open to manipulation by someone with deep pockets. Governments, on their part, could declare Bitcoins illegal.

Like cash, Bitcoins can be lost or stolen if digital wallets are not secured through encryption and paper or digital back-ups. A lost or deleted Bitcoin cannot be replaced.

Despite the criticism and risks, the Bitcoin is gaining popularity. Just before the crash in prices, some expected their value to reach $1,000 by the end of this year. Whether that happens or not, Bitcoins are making their mark on the economy.