The Direct Taxes Code (DTC), 2010, was introduced in the Lok Sabha a few weeks ago. This Bill replaced the Direct Taxes Code Bill, 2009, which was intended to replace the existing Income Tax Act, 1961.

The 2009 Bill had shocked everyone except, perhaps, the team that had drafted it. Several provisions in this Bill were against the elementary principles of taxation. The 2010 replacement has removed some of the glaring discrepancies, but one essential question remains unanswered: Why do we need a new DTC that substantially replicates the old Act?

In his statement on 27 August 2010, the Finance Minister explained that the 1961 Act was amended no less than 34 times, resulting in "complexity in tax laws", and the inability on the part of the average taxpayer to comprehend it.

The new tax code is being brought in with the objective of revising, consolidating and simplifying the language and structure of direct tax laws.

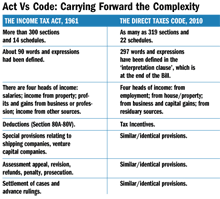

However, a simple comparison of the 2010 code and the 1961 Act shows that there will be no substantial structural change (see Act Vs Code). A plain reading of the new DTC shows that it does not result in either revision, consolidation or simplification of the language and structure of the direct tax laws.

Merely replacing 'salary' with 'employment' and adding expressions like 'tax base' is not simplification. The hard reality is that the new DTC is as complex as the 1961 Act.

A few new provisions

The new Bill has attracted a lot of praise for lowering tax rates. But this can be done by any finance Act and we do not need to discard the old law just to reduce or streamline the rates of tax. Undoubtedly, there are a few new provisions in the 2010 code, but these could have been easily inserted in the old Act.

"There is no purpose in having a new direct tax code whose shelf life is going to be very limited. We are better off with the old Act despite its frequently amended provisions" |

Then, there are bound to be heated arguments on the applicability of numerous case laws under the old Act. Adding to the confusion will be a spate of board circulars that will, of course, interpret every difference in favour of the revenue department.

The Income Tax Act, 1961, repealed the 1922 Act with the avowed objective of placing the income tax law on a stable ground. The First Law Commission had spent several months in preparing the new draft.

A parliamentary select committee had then examined the Bill with a fine-tooth comb, after which it was debated in Parliament for many days. This is in stark contrast to the present day Parliament, where several Bills are passed without any discussions.

All hopes of a stable and simplified law were soon shattered and, as the late lawyer Nani Palkhivala pointed out, the 1961 Act was amended "more often and more drastically during the first six years of its existence than the 1922 Act had been during the 40 years it remained in the statute book".

In the first 15 years, the 1961 Act suffered 560 insertions, 600 substitutions and 190 omissions. In the next 35 years, it underwent more than 2,500 amendments.

Execution is the key

The two components of good tax administration are understandable and reasonable laws, and their effective implementation or execution. If there is one special feature of the Indian republic, it is the exclusive focus on the first component and complete neglect of the second.

To keep on making new laws without executing them is as foolish as a company that keeps on rewriting its mission statement and does nothing thereafter. The fault does not lie with the 1961 Act but with the failure to implement its provisions.

An important provision is the proposed Clause 123, which introduces the General Anti Avoidance Rule. While similar provisions exist in several countries, it is highly likely that it will be abused and every contract that results in a lesser incidence of tax will be declared as 'an impermissible avoidance agreement'.

"The corporate sector, the Income Tax Department, auditors and tax professionals will now have to spend an enormous amount of time comparing and analysing the difference between the old Act and the new code" |

The expressions 'associated enterprise', 'connected persons', 'international transactions' have been widely defined. Clause 124 (19) can also have deadly consequences. It gives unlimited powers to the department to give a completely different interpretation to a contract. Surely, the years ahead are going to be fraught with extensive litigation.

Other deadly provisions

The code contains a few provisions that are either liable to serious abuse or will be wholly unworkable. One example is the proposal to make all managers liable to pay the tax arrears of their employers' companies.

So, if a large company runs into serious difficulties and its taxes cannot be recovered, the department can make the managers liable. Similarly, going abroad can be extremely cumbersome as one will have to get a tax-clearance certificate from the Income Tax Department. Shockingly, foreign airlines can now be made liable for the tax liability of defaulting assessees if they permit them to fly in their aircraft without this certificate.

Another dangerous provision is Clause 159, which permits reopening of assessments even if a different order is passed by an authority or a court in any other proceeding.Shockingly, if the assessment of 'X Ltd' is completed, and several years later, a different view is taken in the proceedings pertaining to 'Y Ltd' (a wholly unconnected company), the assessment of 'X Ltd' can be reopened. The provisions of the Direct Taxes Code destroy the sanctity of an assessment order. There is tremendous scope for extreme arbitrariness in reopening assessments.

The new Direct Taxes Code is an utterly wasteful exercise. It is merely the 1961 Act in a new avatar. The Finance Minister has announced that the new Direct Taxes Code will come into force in 2012. He would do the country a great service by scrapping the proposal for a new Direct Taxes Code and focusing his energies on better implementation of the existing provisions of the 1961 Act.

The author is a noted tax and constitutional lawyer based in Chennai.