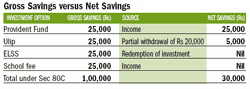

Saving means an increase in one's net worth. However, many taxpayers tend to focus on gross savings without caring to raise their net savings. So though India's domestic savings rate is touted to be among the highest in the world—Indian households saved 22.6 per cent of their post-tax incomes in 2008-9, as per the Economic Survey 2010—people may not be saving as much as they think they are. This is because while making tax-saving investments under Section 80C, they make use of the EEE model to recycle the same savings. While the maximum deduction under Section 80C is Rs 1 lakh, not all taxpayers save this amount. Withdrawals are made from PPF accounts only to reinvest and claim fresh tax benefits. Similarly, while the total amount invested in ELSS funds in 2009-10 was Rs 2,699 crore, investors also withdrew Rs 1,786 crore from these schemes. So, the net inflow into ELSS funds during the year was only Rs 913 crore.

It is this mindset that makes Ulip buyers consider their investments as a short-term tax-saving option rather than a long-term wealth creation and risk management tool. Since partial withdrawals are allowed after the lock-in period, investors dip into the corpus and reinvest the amount.Smart? No, if you consider the threat of old-age poverty India faces 30-35 years from now, when its demographic dividend of a young population will end and today's youth will retire. The threat is evident even now. Did you know that the average corpus of an EPF account is Rs 50,000, which can earn a monthly pension of barely Rs 375.

In this backdrop, the EET proposal is welcome. If one has to pay tax on withdrawals, one will avoid dipping into the retirement corpus. The present tax laws are biased against long-term savings as they don't make any distinction between a three-year and a 30-year investment horizon. This promotes current consumption over future consumption. All the tax-saving options specified under the new Section 66 are long-term investments. No more lock-in periods of three and five years. No more tax-free withdrawal and reinvesting cycles. The DTC will tax all withdrawals, unless the maturity proceeds from an investment are reinvested in the specified options. Maybe the DTC should strike out the deduction offered to tuition fees of two kids. For, if you pay tuition fee, you aren't adding to your net worth, are you?