You have paid your taxes and made your tax saving investments. But the worst is yet to come: filing income tax returns. Last year, the Government introduced a new set of tax return forms, longer than the single-page Saral. The new forms might seem intimidating, but are actually more comprehensible and user friendly than the Saral.

The best thing about the new forms is that they are in a tech-enabled format. And you don't have to attach all those papers — no Form 16, TDS certificates, proof of tax saving investments, etc. Just fill it and submit it, online or offline.

Can filing returns really be so easy? It seems that way, considering the fact that about seven lakh individual taxpayers filed tax returns electronically last year. About 45 minutes is all it takes to fill up your tax return form online provided you have all the required information on income, investment and expenditure handy.

ONLINE FILING: THE PROCESS |

| 1. Log in |

| 2. Prepare return — (Conventional route)— Take print — Physically submit it |

| 3. Make XML file |

| 4. Log in to http://www.incometaxindia.gov.in/ |

| 5. Upload XML — (if no digital signature) — Print two copies of receipt — Submit to IT Department — Retain one stamped copy of receipt |

| 6. Append digital signature |

| 7. Print receipt |

There are three routes to filing your tax return online. The simplest and most basic method is to use the services of a tax portal. There are at least half a dozen tax portals that help you fill up and submit the form online. Just log on and follow the simple instructions.

For as little as Rs 200, the completed form is uploaded and submitted to the tax department online. Or you can take a print of the completed form and submit it in physical form. Some portals even arrange to pick up the printout of the form from your house and submit it for you for a small fee.

The next online option is to prepare a return online and upload it yourself on the Income Tax Department's website (http://www.incometaxindia.gov.in/). Print two copies of the acknowledgement form (ITR-V) and submit them at the IT office. The receiving official will return a stamped copy to you.

The third option is a truly online process, which does not require physical submission of the tax return to the authorities. Prepare your return, upload it on the site, add your digital signature and print an acknowledgment. A digital signature costs around Rs 1,000 and is valid for two years.

You can also use the signature for other online transactions.Despite the ease of online filing, the process is yet to take off in a big way. The number of e-filers constitute less than 3% of the total number of tax returns filed in the country last year. This is expected to go up this year.

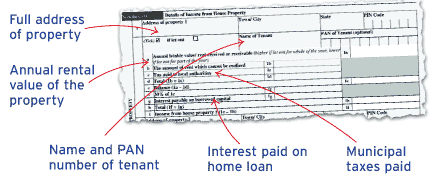

INCOME FROM HOUSE PROPERTY Saral dismissed this with a single line entry. The taxpayer just wrote out the income from house property and that was it. But in the new forms, the taxman wants to go the whole distance. He wants to know the following things:  |

Last year, nearly 50% of the seven lakh e-returns were filed in the last five days before the due date. More than 15% were filed on the last day. "Many taxpayers wait till the last week to put together all the tax-related documents," says Delhi-based tax consultant Surya Bhatia. "They don't realise that efiling has only made the process easier; the documents are still required."

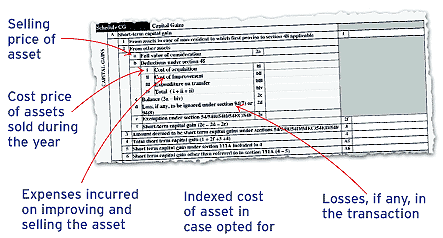

The section on capital gains, for instance, requires a taxpayer to fill in lots of details. In the Saral, income from capital gains was dealt with in just three lines. The new forms have a 45-line section on it. Taxpayers who have made capital gains this year, whether in stocks, mutual funds, real estate or gold will be required to give details regarding the acquisition price of the asset, expenditure incurred to improve it and the price at which it was sold.INCOME FROM CAPITAL GAINS The three lines and four columns devoted in Saral to list out short-term and long-term capital gains in the four quarters have been expanded to 45 lines in the new forms. The tax department wants you to state the following:  |

It's an annual nightmare that chartered accountants and tax consultants have to live through. Indolent clients wake up just a few days before the due date and provide sketchy details that need plenty of clarifications. Often, this leads to discrepancies in the tax return that could result in a notice from the income tax authorities.

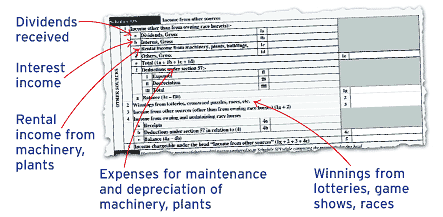

Though the high costs of digital signature is still an issue, the new tax return forms are a major step towards making e-filing popular. Of course, for people who still can't get head or tail of the new forms, there's help at hand in the form of tax return preparers. It's a good idea for first timers to let a TRP teach them the ropes before they venture into DIY territory.INCOME FROM OTHER SOURCES This too was single line entry in the Saral. Now it is a 17 line section that seeks the following information:  |

CLEARING THE AIR

The annual information return (AIR) is a section in the new tax forms, in which you will have to declare any "high-value transactions" made during the year. These transactions include:

• Cash deposits of over Rs 10 lakh in any savings account in a year

• Credit card bills of over Rs 2 lakh in a year

• Investment of over Rs 2 lakh in mutual funds

• Investment of over Rs 5 lakh in bonds or debentures

• Investment of over Rs 1 lakh in a public issue of shares

• Investment of over Rs 5 lakh in RBI bonds

• Sale or purchase of property of Rs 30 lakh or more

Till now, credit card companies, banks, mutual funds and financial institutions used to file AIRs listing high-value transactions by any customer during the year. Now, individuals are also expected to provide such details, making it possible for the tax authorities to compare the AIRs, as well as compare a taxpayer’s income and expenditure.

| • Taxpayers have to declare high-value transactions made during the year |

| • This information also filed by banks, mutual funds, credit card companies |

| • The taxman will compare the two sets of information |

| • He will also see if investments and expenses match income |

Any mismatch is an invitation for a notice. "If you declare an investment of Rs 5 lakh in the year when your income is only Rs 1.5 lakh, our computer will pick up your case for scrutiny," says CBDT Chairman Ratneshwar Prasad. Some experts feel that the limits mentioned above are for single investments or bills of one credit card. "However, the current provision requiring this information to be reported in the form causes a lot of confusion whether the limit is for a single card or for all credits cards put together," says Sonu Iyer, tax partner, Ernst & Young-India.

Others say that you can invest more than Rs 2 lakh in different mutual funds and not declare it in the AIR. This is not the case. The declaration in the AIR is meant to show your combined investments and expenditure. Nitin Baijal, director, BMR & Associates, advises taxpayers to err on the side of caution and make a declaration if the combined investment or expenditure exceeds the limit. "Honest taxpayers have nothing to fear since this is only a declaration of investments and expenditure out of their stated income," he says. Indeed, there's no reason to give the taxman an excuse for issuing a notice, is there?