| Cost comparison | ||

| Service/facility | Then | Now |

| Credit cards (interest) | 30-40% | 35-50% |

| Premature account closure | Rs 250 | Rs 500 |

| Unblocking debit card | 0 | Rs 100 |

As if the rising interest rates were not worrying enough, now be prepared for the sting of higher service charges. The financial sector in the country has been battling rough weather for a while now. With a significant slowdown in credit growth and deposit rates going up, banks are scrambling for ways to plug their declining net interest margin. The most obvious way is to hike charges for services, be it cheque issuance, locker facilities or credit cards. In fact, most leading banks, private and public, have started announcing revised fees. This is the bad news. On the other hand, RBI is taking a host of steps to make banking customer-friendly. From allowing bonds as collateral for bank loans to allowing sleeping bank accounts to earn an interest, there is good news in the offing.

Forget the freebies: From unblocking a debit card and depositing cash in a branch other than your home branch to mobile banking, most bank services shall now incur a fee. You will also have to pay more for facilities like making a demand draft or getting a duplicate passbook. In fact, the fees for some products have been hiked by up to 50%. Kotak Bank was the first to announce a hike in its service charges, followed by the State Bank of India, the IDBI Bank, Bank of India and, most recently, ICICI Bank.

The last, ICICI Bank, is charging Rs 50 per demand draft up to Rs 10,000 and Rs 3 per Rs 1,000 thereafter, subject to a maximum of Rs 15,000. Till 1 August, the bank charged Rs 2 per Rs 1,000, subject to a minimum fee of Rs 50, and a maximum of Rs 10,000. On the other hand, SBI has decided to levy Rs 2 per Rs 1,000 deposited at a non-home branch from 1 September. Earlier, cash deposit up to Rs 50,000 at a non-home branch was free and millions availed of it as a means of sending money home. M.V. Nair, chairman and managing director, Union Bank of India, says, “Income from core banking operations are likely to suffer at least in the current financial year. So banks are on the lookout to increase their income.” To compound the problem, higher service charges also mean higher penalties. Apart from paying more for bounced cheques and premature closure of an account, you will have to watch out for new penalties.

Telling figuresNumbers speak louder than words. Money Today highlights some figures that have an immediate or long-term personal finance implication. 24.1% 90.6 lakh 46,000 crore 1,145 crore |

No penalty for sleeping accounts: Do you have a savings account that you haven’t touched for months? Now you will not only earn the regular 3.5% interest on it, but also escape the penalty for sleeping on the account. The RBI has recently ruled that banks can no longer impose a fee for reactivating the account, which ranged from Rs 200 to Rs 750. The circular issued by the central bank suggested the same interest rate on unclaimed fixed deposits. An account is considered inoperative if you don’t withdraw or carry out credit or debit transactions, be it via the ATM, branch or the Internet, for a certain period at a stretch. Till now, banks had different definitions for this “period”, which ranged from one year to 15 months, but RBI has fixed the ceiling at two years. However, service charges levied by banks will not make an inoperative account operative.

Bonds as collateral: Most retired people find it difficult to land an unsecured bank loan, and drumming up the requisite collateral is easier said than done. But help is at hand, thanks to the Finance Ministry. If you own savings bonds, which were issued by the government as a saving avenue for retiring officials, you can now pledge it against a loan. But loans can be availed of only by the holders of the bonds, not by third parties, and the facility is limited to the 7% bonds issued in 2002 and the 6.5% and 8% bonds issued in 2003.

Be punctual or pay up: How often have you had to wait for days for a cheque to be credited to your account? Though RBI states that a local cheque should be processed the same day, or latest by the next day, and that outstation cheques shouldn’t take over 15 days, the ground reality was different. Now, the National Consumer Disputes Redressal Commission, on a petition by advocate Atul Nanda, has asked the banks to stick to the schedule. So if your cheque is languishing or lost, make sure your bank pays an interest at fixed deposit rate or a rate as per its policy.

The much awaited iPhone 3G is finally in India. But the high price tag— Rs 31,000 (8 GB) and Rs 36,100 (16 GB)—has been a big dampener. Most people are disappointed that the same set costs much less in the US: $199 or Rs 8,720 for the 8GB version. What they forget is that the monthly subscription charges are much higher in the US and one is tied to the service provider for at least two years. A simple calculation shows that over two years, iPhone usage works out cheaper in India than in the US.

| The real cost of an 8 GB iPhone | ||

| India | US | |

| Handset | Rs 31,000 ($706) | Rs 8,720 ($199) |

| Activation cost | Nil | Rs 1,577 ($36) (one time) |

| Monthly fee* | Rs 999 ($23) | Rs 3,067 ($70) |

| Talktime/data | 299 mins/500 MB | 450 mins/unlimited |

| Contract | None # | 2 yrs with AT&T |

| Ownership cost over 2 yrs | Rs 51,783 ($1,181) | Rs 83,923 ($1,915) |

| Taxes and actual usage charges have not been included; *monthly fee is for data and talktime; # All warranties/benefits are null and void if unlocked before 12 months; rupee-dollar exchange rate: 43.8 | ||

Traditionally, the best hedge against inflation has been gold. But with gold (and silver) prices on the slide despite the increasing demand, is it the right time to invest in gold or are the prices likely to go down further? Gold is now trading at Rs 11,700 per 10 gm, down from Rs 14,000 till a few months ago. Says Sanjeev Agarwal, managing director, Revah Corporation (which owns a chain of retail jewellery shops) and ex-managing director, World Gold Council: “This is a short-term correction; gold prices may shoot up any time.” One reason for this confidence is that the factors pushing up gold prices remain intact. So while oil prices—which fell slightly and led to a fall in gold prices—are unlikely to fall further, the weakening of US dollar may only be temporary, and inflation is still not under control. According to experts, such minor corrections should be seen as an opportunity to buy gold. Gold exchange traded funds (ETFs) are also a good option. If you already hold units, don’t panic. “People think of redeeming the moment there’s a sharp correction, but it’s not wise to sell at this time,” says financial adviser Amar Pandit. Gold ETFs will give reasonable returns only over a long term, so keep them for at least 3-5 years, he adds.

Traditionally, the best hedge against inflation has been gold. But with gold (and silver) prices on the slide despite the increasing demand, is it the right time to invest in gold or are the prices likely to go down further? Gold is now trading at Rs 11,700 per 10 gm, down from Rs 14,000 till a few months ago. Says Sanjeev Agarwal, managing director, Revah Corporation (which owns a chain of retail jewellery shops) and ex-managing director, World Gold Council: “This is a short-term correction; gold prices may shoot up any time.” One reason for this confidence is that the factors pushing up gold prices remain intact. So while oil prices—which fell slightly and led to a fall in gold prices—are unlikely to fall further, the weakening of US dollar may only be temporary, and inflation is still not under control. According to experts, such minor corrections should be seen as an opportunity to buy gold. Gold exchange traded funds (ETFs) are also a good option. If you already hold units, don’t panic. “People think of redeeming the moment there’s a sharp correction, but it’s not wise to sell at this time,” says financial adviser Amar Pandit. Gold ETFs will give reasonable returns only over a long term, so keep them for at least 3-5 years, he adds.

—Shruti Kohli

| Pay less to talk | ||

| Category | Current | Expected |

| Local rates | Re 1 | 60 p |

| STD rates | Re 1-2 | 50-80 p |

| ISD rates | Rs 4-5 | Re 1-3 |

| Source: ISPAI | ||

Want to save money on long-distance calls? Shift to Internet telephony. If the Telecom Regulatory Authority of India (TRAI) has its way, it will not only be cheaper to make phone calls through the Internet, but you can also choose the cheapest STD and ISD tariffs irrespective of your service provider. In its recommendation to the Department of Telecom, TRAI has asked for lifting of all restrictions on Internet telephony. So far, communication was allowed only between personal computers or from a PC to mobiles/landlines abroad, but soon, you could make calls to landlines and mobiles in India too. All you need is an adapter, which costs Rs 1,000-1,500 and converts a regular landline with broadband connection to a Net phone. In another recommendation, TRAI has asked telecom providers to offer their subscribers the choice of picking their own carrier for long-distance calls, domestic or international. This is how it will work if it gets the government nod: if you are a Bharti subscriber and find that BSNL has the best rates, you can buy a pre-paid long-distance package from BSNL, get on to the BSNL network, dial the number and start talking. The only trouble is that you have to plan your talktime in advance or end up buying multiple packages. But service providers are likely to protest on both scores.

You have reason to party if you were among the over 10,000 investors who applied for the derailed Rs 34 crore initial public offering of SVPCL Ltd in October last year. The Supreme Court has upheld the Securities Appellate Tribunal’s (SAT) directive that the Hyderabad-based company should refund the application money along with 15% interest to all the applicants. The court observed, “Investors have suffered for a long time and their money should be given back to them immediately.” Though the issue was fully subscribed when it was launched, the Bombay Stock Exchange denied permission for the shares to be listed because UTI Securities, the lead merchant banker, had expressed its inability to give an undertaking as required under the Companies Act. A prolonged court drama followed. SVPCL first challenged BSE’s move in the Andhra Pradesh High Court, saying the delay was due to the pending complaint with Sebi, which was beyond its control. The court issued an interim order to BSE and NSE to allow the listing, not trading, of the shares on the exchanges. Then the BSE challenged the interim order and demanded that the matter be looked into by SAT, which in turn ruled against the company. Let’s say a prayer for quicker justice now.

| Number crunching |

| Entry age: 18 to 55 years |

| Policy tenure: 10 years |

| Premium payment tenure: 5 years |

| Fixed annual premium*: Rs 35,000 |

| Life cover with plan: Rs 3.5 lakh (10 times the annual premium) |

| *premium same across all ages |

Health seems to be the biggest concern among life insurers this year. Not to be outdone, Aviva life insurance has joined the fray with its Health Plus plan. The easy-to-understand bundled product carries a fixed annual premium of Rs 35,000 to be paid over five years. It offers the policyholders cover for life, accidental disabilities cover for 10 years and health benefits for five years. The last is spread across 18 critical illnesses listed in the policy, besides hospital cash benefit and surgical benefits, depending on the type of surgery.

For those who consider healthcare plans an unavoidable expense, an important feature is that the policy guarantees maturity benefits even if a medical claim is made. What this means for individuals under 46 years at the time of taking the policy is that they can collect more money from the insurers on maturity than they pay as premium (Rs 1.75 lakh). For the rest, the costing is such that the premium returned reduces; it’s nearly Rs 1 lakh for a 55-year-old. This reduction in maturity benefit for those above 45 years is to adjust the mortality charges for higher ages. Being rich in features, the policy should appeal to all individuals even if the premium is a shade higher than what others boast. Then again, the premium is offset by the tax benefits under Section 80C and Section 80D that the policy offers. The mix of life and health benefits means that one can take this plan to supplement a health cover with a limited period term plan.

—Narayan Krishnamurthy

Hotels for the price of candy,” screams an Ezeego advertisement offering bookings in three-star hotels at Re 1 a night. Travelocity is promising 30% off on heritage holidays across India. A few other online travel portals are promising cashback schemes on hotel stays, while the hotels are falling all over themselves to offer hot deals like complimentary fourth night or seasonal packages. At a time when the average room rates in Indian hotels are going up by 20-40% annually, such schemes may sound like a late Independence Day present. The hotels are not doing this out of love for you, but due to compulsion. With air fares spiralling out of control and a slowdown in corporate bookings, both of which have contributed to fewer people checking in, hotels have had to pull up their socks when it comes to wooing travellers. There can be no time like the present when it comes to bargaining for a better hotel deal, or at least more freebies such as meal vouchers or spa treatments. Hit the road or take the train to maximise holiday savings.

—Sushmita Choudhury

Word’s worth —Montek Singh Ahluwalia, Deputy Chairman, Planning Commission “Though it’s the right time to invest in equity, we have to react as per consumer demand which is biased towards FMPs” “The slowdown or the crash in real-estate prices is only at the micro level.The negativity is mostly sentimental” “The recent decline in global oil prices will not help cool consumer price inflation in India as energy prices are still below global levels” Source: Business Line, The Economic Times |

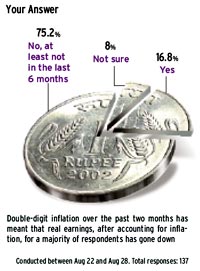

Your verdict

Your Answer Double-digit inflation over the past two months has meant that real earnings, after accounting for inflation, for a majority of respondents has gone down Conducted between Aug 22 and Aug 28. Total responses: 137 |

Most of our stories are devoted to bringing the best expert advice on personal finance. But our readers too come up with profound pearls of wisdom. We bring you the results of Money Today online poll on select and current investing issues.

Most of our stories are devoted to bringing the best expert advice on personal finance. But our readers too come up with profound pearls of wisdom. We bring you the results of Money Today online poll on select and current investing issues.