• Inflation and market cycles usually have an inverse correlation • The current market cycle is likely to last for at least a year • Rising costs and new capacities will show up from the next quarter results • Use short market rallies to off-load weak stocks in your portfolio • Watch out for market anomalies, when valuations of blue-chip stocks are lower, and buy them |

The only way to master the art of stock investing—low risk and high returns—is to take the time-tested route of long-term investing. Money Today has always preached the virtues of this strategy. But investors—rattled by the yoyoing Sensex and the fact that they cannot predict whether the future will offer respite or further dent their portfolios—can be forgiven for thinking that long-term investing is subservient to market cycles. In times like these, when the market is both bearish and volatile, when every opportunity to grab a good share for a bargain is fraught with risk (what if the price of the share falls further), you might wonder if it is more prudent to stay out of the market till it recovers.

Allow us to prove this notion wrong. If you do decide to abstain from Dalal Street, be prepared for a very long wait. Given the uncertain global and national economic situation, the market is likely to stay bearish for at least a year. And as a stock investor, you shouldn’t, and indeed cannot afford to, be inactive for so long. So what should your strategy be? The answer depends on where you think the market is headed at any given point in time.

The volatility in the market offers two clear opportunities for investors—the phases of recovery allow you to sell the bad stocks in your portfolio, while the periodic downswings will offer the opportunity to pick up good long-term bets. As Nandan Chakraborty, head of research, Enam Securities, says: “Investors should use this bear rally to prune weaker trading positions, while picking up blue-chips for the core portfolio if the valuations are right.” At the same time, the current market scenario leads to certain inconsistencies that promise opportunities in the long term. Says Sanjeev Patkar, head, research, Dolat Capital: “We feel the market is still incoherent and has diverse anomalies where valuations are concerned—a construction company trades at a multiple of 15xFY09E, while quality assets such as Maruti trade at a 7xFY09E (core earnings).” Some quality businesses have gone unnoticed in the market, so watching out for such anomalies can help you build a solid portfolio.

Word’s worth —C.B. Bhave, Chairman, Sebi, on cutting the time for a rights issue from 109 days to 43 days “Inflation may touch the 13% mark, (but) trends of moderation should begin in December” —C. Rangarajan, former RBI chief “Investors looking to put money in income schemes could try fixed maturity plans, which give better post-tax returns compared with traditional products” —Nimesh Shah, CEO, ICICI Prudential Asset Management “It makes sense to go for a fund that invests in frontier markets because these countries throw up a lot of potential for investors” —Anthony Heredia, CEO, Morgan Stanley Mutual Fund Source: Business Standard, The Hindu, IANS, Economic Times |

The bottom line is that volatility is not your enemy if you know how to use it to get rid of the once-promising-but-now-dud stocks at a decent price during a relief rally and pick up long-term bets, current or potential blue-chips, when markets fall below the levels that fundamentals justify. The investors who make such use of volatility will ride the market cycle and gain the most when the bull run returns.

— Rakesh Rai

Defining disease

Have you ever had your medical claim rejected by insurance companies citing “pre-existing health condition”? The perennial debate on the health conditions that are covered by policies claiming to insure pre-existing diseases and the ones that are excluded, has finally been resolved. The General Insurance Council (GIC), a statutory body for all non-life insurers, has provided a clear definition. From now on, pre-existing exclusion will mean that “the benefits (of health insurance) won’t be available for any condition, ailment or injury for which the insured had signs or symptoms, and/or was diagnosed and/or received medical advice/treatment, prior to the inception of the first policy, until 48 consecutive months of coverage have elapsed after the date of inception of the first policy”.

Says K.N. Bhandari, secretary general, GIC: “We have issued an advisory to all insurers suggesting that they apply the same definition to existing policies. But it is their discretion to adopt the definition.” The policies issued from 1 June 2008 will have to adopt the new definition and will cover pre-existing diseases from the fifth year of the policy, should the policy-holder not make any claims for the first four years. Strangely, only health insurers and general insurance companies selling health plans will have to follow this diktat. Nonetheless, policy-holders will no longer be at the mercy of the whims of the insurers, and that is good news.

Pre-existing diseases will include:

•Hypertension, leading to heart condition

•Diabetes, leading to other ailments

•Obesity, leading to health deterioration

— Narayan Krishnamurthy

Battle of indices

Stocks in the DJIT 30 and not the Sensex Cairn Energy Stocks in the Sensex, not in DJIT NTPC |

Why does India need another benchmark? That’s the question most investors were asking when media mogul Rupert Murdoch launched the Dow Jones India Titans 30 (DJIT) index earlier this month. One answer is that though both indices look at the stocks of 30 leading companies, their line-up differs—the DJIT index lays more emphasis on infrastructure and capital goods and has omitted some popular infotech and financial sector stocks listed on the Sensex. Their weightages also vary. For instance, the Reliance Industries figures on the DJIT index with the weightage of 10.8% as compared with 15.96% on the Sensex.

This discrepancy is because the new index has 10% weightage cap for individual securities, which makes it stand out among the other benchmark indices in the country such as the Nifty and the Morgan Stanley India index. The DJIT index is not a replacement for the Sensex. It simply offers a different perspective on Dalal Street, helping you to take more informed investment decisions.

— Rakesh Rai

Prepaid insurance

Taking a cue from the success of mobile telephony, Max New York Life is looking at launching a low-cost insurance cover which will be sold like prepaid mobile packs. The company plans to stock retail stores in small cities and semi-urban areas with start-up packs, which come in three denominations and offer five times the sum insured. The cost of the package ranges from Rs 1,000 to Rs 2,500. Says Analjit Singh, chairman, Max New York Life: “This is an extension of the existing distribution channel and will allow policy-holders to have additional top-ups for their insurance policies.” This low-cost insurance experiment could prove successful for consumer loan companies—a loan can be backed with this kind of insurance and offered to consumers as a package. One can choose to top up the policy—with a minimum value of Rs 10—or withdraw it after the three-year lock-in period.

— Narayan Krishnamurthy

Telling figures

40% |

Robbing Peter

The rich are different, said F. Scott Fitzgerald. Ernest Hemingway’s response, “Yes, they have more money”, should have included a corollary: they get more benefits. Mutual fund (MF) investors from the Richie Rich club are charged lesser entry and exit loads by fund houses compared with the hoi polloi. But now the Ministry of Corporate Affairs has asked the Securities and Exchange Board of India to examine the matter. For the uninitiated, an entry load is charged to recover selling and marketing expenses, while exit load persuades investors to stay for a longer period. Fund houses justify this differentiation by saying that it helps them get more subscription and enables investment in large-cap and high-value Sensex stocks. According to Dhirendra Kumar of Value Research, “While MFs can still justify giving a discount on entry loads (which is like a buyer getting a discount for buying in bulk) if it is not at the cost of retail investors, charging a lower or nil exit load to high net worth individuals is not justified as it affects the whole portfolio and defeats the purpose of exit loads.” Whether Sebi will succeed in levelling the playing field or not is another story.

— Rakesh Rai

Mobile to cash

Sending money can be an extremely tedious process. More so, if the other person does not have a bank account. The ICICI Bank has recently introduced smsNcash, a mobile banking service that lets you transfer money to anyone who needs it, whether he has a bank account or not. The maximum amount that you can remit is Rs 10,000 per transaction, with a limit of Rs 25,000 a day. You will have to pay Rs 10 as processing fee if you are sending money up to Rs 5,000 and Rs 20 for higher transaction amounts. To avail of this service, you will have to register for the mobile banking facility. As of now, the facility is limited to specific ATMs, but the bank is planning to expand its scope over time.

1. Log in to your online account, enter the remittance amount, your debit account number and your friend’s cell number

2. Your friend will receive a six-digit code number and you will receive a four-digit code number on your mobile phone

3. Call your friend and tell him the four-digit code and the amount of money that he can withdraw

4. After verifying his phone number, the two codes and the transaction amount at the ATM, your friend gets the cash

— Namrata Dadwal

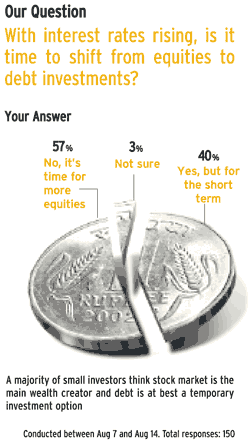

Your verdict  Our question A majority of small investors think stock market is the main wealth creator and debt is at best a temporary investment option Conducted between Aug 7 and Aug 14. Total responses: 150 |

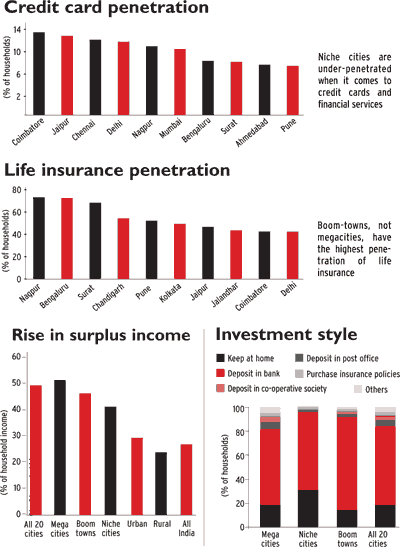

Cities to watch:

It is easy to rattle off the names of India’s megacities. But an insight into the emerging cities is far more interesting, be it from the point of view of affordable real estate, job prospects or a better quality of life. The National Council of Applied Economic Research, along with the Future Capital, has launched a book focusing on this. Titled The Next Urban Frontier: Twenty Cities to Watch, the book lists the eight usual suspects comprising the metros, Pune and Ahmedabad, along with 12 boom-towns and niche cities. The former stand out because they are quickly moving up the ranks as the largest consumer markets after the megacities. This chunk— Surat, Kanpur, Jaipur, Lucknow, Nagpur, Bhopal and Coimbatore—has also posted the fastest growth in disposable incomes since 2000. Niche cities may be smaller in terms of population but their household expenditure is nearly the same as in the megacities. In fact, these cities—best represented by Faridabad, Amritsar, Ludhiana, Chandigarh and Jalandhar—have the highest spending propensity among the three city groups. Here is a look at some interesting spending and investment patterns in these cities:

It is easy to rattle off the names of India’s megacities. But an insight into the emerging cities is far more interesting, be it from the point of view of affordable real estate, job prospects or a better quality of life. The National Council of Applied Economic Research, along with the Future Capital, has launched a book focusing on this. Titled The Next Urban Frontier: Twenty Cities to Watch, the book lists the eight usual suspects comprising the metros, Pune and Ahmedabad, along with 12 boom-towns and niche cities. The former stand out because they are quickly moving up the ranks as the largest consumer markets after the megacities. This chunk— Surat, Kanpur, Jaipur, Lucknow, Nagpur, Bhopal and Coimbatore—has also posted the fastest growth in disposable incomes since 2000. Niche cities may be smaller in terms of population but their household expenditure is nearly the same as in the megacities. In fact, these cities—best represented by Faridabad, Amritsar, Ludhiana, Chandigarh and Jalandhar—have the highest spending propensity among the three city groups. Here is a look at some interesting spending and investment patterns in these cities:

Family account

Assume you have a five-member family and each member has an independent savings account. This means that a minimum of Rs 50,000 from your family’s collective kitty is locked away as mandatory quarterly balance, unless you fancy being penalised. Now, Barclays Bank promises to take care of the problem with the just-launched Kutumb Savings Account, a family savings account. The offer is open for up to five family members, and singles are excluded. The family, comprising parents, spouse, children, in-laws and other close relatives, nominates one person as the principal member for leading the account. He will be responsible for the maintenance of the minimum balance. However, each family member is assigned a separate account with several value-added features like free withdrawals at non-Barclays ATMs and free pay-orders and demand drafts. The principal member is also entitled to a few privileges like a free accident insurance of Rs 1 lakh. The account also offers the family the option to include their domestic help under this umbrella. The domestic help named in the account can have access to a no-frills savings account. Says Suresh Gurumani, director, retail banking, Barclays Global Retail and Commercial Banking, India: “Barclays Kutumb not only serves the entire family, but also offers a practical way of reaching out to the unbanked.”

| Principal member Has to maintain the minimum balance in the account | |

| Up to five separate accounts for family members Each account is managed independently with many value added services | Bank account for domestic help The helpers are given a no-frills savings account and, as an exclusive offer, the quarterly balance is waived |

— Priya Kapoor

Investor rights

Till recently, the “right to information” did not mean very much to investors in UTI. So if one wanted to check the records of India’s first mutual fund company before applying, he was laughed out of town. But one Mumbaiite has single-handedly changed this. Vijay T. Gokhale approached the Central Information Commission (CIC) when the UTI and Sebi ignored his queries on the Unit Trust of India Asset Management Company. The CIC, in a landmark order, has ruled that an institution wholly owned by a public authority could be considered in the same mould and, therefore, has to comply with the Right to Information Act. Since the UTIAMC is owned by four public authorities, it can no longer deny Indians information— and even copies—on its balance sheet, mode of appointment of directors, profit-sharing patterns and the like.

— Sushmita Choudhury

Post the hike

Sending a rakhi through the courier service has never been costlier; you would have paid 10-25% more this year. With the cost of aviation fuel sky-rocketing and inflation eating into their margins, courier companies are passing on the burden to consumers. So big players such as Fedex, Elbee Express, DTDC and AFL WIZ revised their charges last month. Blue Dart has hiked prices in its retail air and ground express service by 15% and freight services by 10%. Worse, there are indications that the rates will be hiked yet again by at least 3%. Perhaps it’s time to turn to virtual gifts.

Dial for jobs

It has long been accepted that the Indian labour market is plagued by two key ills—connecting people to jobs and a demand-supply mismatch. TeamLease Services, India’s largest staffing company, has launched a Job Hotline that hopes to tackle both the issues. Available in 11 languages (English, Kannada, Tamil, Telugu, Malayalam, Hindi, Marathi, Marwari, Oriya, Bengali, and Manipuri), the helpline will be available from 8 a.m. to 8 p.m. on all days. On dialling 60012345, you will receive a unique candidate ID and a preliminary assessment will be conducted to enter your details in the firm’s job matching engine. The shortlisted candidates will be invited to take a one-hour advanced assessment test at 150 centres across the country for a more detailed feedback. All the assessed candidates will receive a call from TeamLease within 72 hours, detailing the job prospects and options. The candidates for whom the firm cannot find job matches will be counselled on short-term courses to upgrade their profile and to try finding the right job again.

— Sushmita Choudhury

Earnings Growth Over the Next Three Years :