When the Wall Street was breached, the Indian bourses had to battle a tsunami. Succumbing to panic, institutional and retail investors frantically pulled out money from the stock market and mutual fund schemes. The result was an unparalleled liquidity crisis in the equity market. Cynics might say it’s a case of too little too late, but market regulator Sebi is now considering ways to minimise the impact on institutions and companies, thereby helping investors. Here is a look at the measures that will affect your investments in the stock markets.

MUTUAL FUNDS: In a bid to cap the huge redemption pressure that mutual funds have been facing since October, Sebi has curbed early exits from closed-ended schemes. Mutual funds will have to list all their closed-ended funds, including fixed maturity plans, on the stock exchanges. Now, the only way that investors can exit prematurely from these schemes is by selling the units on the bourses. Earlier, they could scoop their money out of a scheme after paying an exit fee.

Sebi has also mandated that the underlying assets for such schemes will not have a maturity beyond the date on which the scheme expires. Says Sukumar Rajah, CIO, equity, Franklin Templeton Investments: “This will help the fund contain the interest rate risk on the debt portfolio by matching the maturity of its debt securities with that of the fund. It will also help the fund remain fully invested through its tenure, reducing a cash drag on returns.”

The decision will also benefit investors as mutual funds will no longer have to dip into their reserves or sell assets—often at depressed prices in a falling market—to pay off investors who wish to opt out of a scheme.

IPOs AND RIGHTS ISSUES: Sebi has decided to extend the validity of the approval letter it hands out for public and rights issues. The validity has gone up from three months at present to a year. This means a company can wait for a year before a flotation if it finds the market isn’t receptive to IPOs. The move will immediately benefit 18 companies, which were collectively planning to raise around Rs 9,000 crore. In the past year, about 40 companies, which were planning to raise Rs 29,000 crore, had to let Sebi’s permission lapse due to poor investor response.

The board has also cleared a proposal, allowing electronic trading of ‘rights entitlement’ in stock exchanges. Now, shareholders with demat accounts can receive their rights shares in an electronic form. The issuer will gain access to issue proceeds only after the allotment is finalised.

In addition, Sebi is debating the collection of disbursement amount from entities that have committed irregularities in the market as also ways to compensate the investors. The other issues discussed by the board include the segregation of schemes for corporates and individuals. Sebi has asked the Association of Mutual Funds in India (Amfi) to prepare an industry paper on the subject. Says A.P. Kurian, chairman, Amfi: “This crisis has thrown up certain issues, which are, in a way, welcome. The paper aims at promoting mutual funds for retail investors.”

Steps taken by Sebi

• No early exit in any closed-ended mutual fund schemes.

• All closed-ended schemes to be compulsorily listed on stock exchanges.

• Underlying assets of such schemes not to have maturity beyond their expiry date.

• Validity period of IPOs and rights issues extended from three months to a year.

• Firms to access rights issue proceeds only after the finalisation of allotment.

• Rights entitlement to be available in demat form.

Gulliver Yields to Lilliputians

This is the second highprofile case of investor activism in recent times, after DLF was forced to offer shares to minority shareholders in 2006. Experts say the backlash was swifter in this case as institutions hold more than 60% share in the firm. It has also put a question mark on the role of independent directors on the board, who are supposed to protect the interests of non-promoter shareholders. “We will see investors becoming more active in India if firms don’t adhere to corporate governance,” says S. Dalal, MD, IL&FS Investment Managers.

WORD’S WORTH  —Praful Patel, Aviation Minister “Interest rates on deposit and lending are expected to come down by 150 basis points by March 2009.” —T.S. Narayanasami, Chairman, Indian Banks’ Association “About 4,000 ancillary units are on the verge of closure and about 2 lakh people will be affected by this crisis.” —Anil Bhardwaj, Secretary General, FISME “The markets are seeing a momentum upswing, but only when the global and domestic macro-economic environment stabilises will we see a sustained rally.” —V.V.L.N. Sastry, Country Head, Firstcall India Equity Advisors Source: The Hindu, The Business Standard and Reuters |

Your money’s worth

Why does one take vehicle insurance? The answer is obvious—for cover against damage and theft. But what if your insurance company gives you less than the insured value citing ‘market value’? That’s exactly what the National Insurance Company tried to pull off. A customer’s vehicle was insured for Rs 7 lakh before being stolen, but the insurance company offered to settle the claim for Rs 5.5 lakh, stating that he was “entitled only to the market value as assessed by the surveyor”.

Unhappily for the company, the customer took up the matter with the Delhi State Consumer Commission, which ruled that the cost of the vehicle and the corresponding premium charged after theft, or damage, would be the same value as assessed at the time of issuing the insurance policy. The commission held that if insurance companies were allowed to re-assess the market value, then the concept of charging a premium and declaring an insurance value would “lose its meaning”. Now insurance companies can, at best, deduct the depreciation value—5% per year for passenger vehicles and 10% for commercial. This ruling effectively means that insurance companies will no longer be able to appoint surveyors to assess the value of a vehicle after theft or damage.

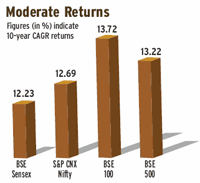

Equities vs bonds

TELLING FIGURES Numbers speak louder than words. Money Today highlights some numbers with a short- or long-term impact. 25 is the number of US banks that collapsed this year. On an average, it’s two banks failing in a month. 54% of Indians prefer insurance schemes while 34% opt for fixed deposits, according to an AC Nielsen survey. 200 billion messages each day, approximately 90% of worldwide e-mails, are spam-related, claims a Cisco study. 12% is the increase in non-performing assets of Indian banks in 2007-8, according to a recent RBI report. |

It’s Raining Guarantees

YOUR VERDICT Our question Will India Inc. heed the finance minister’s call to reduce prices to boost demand? Your answer 54.9% Yes, in the near future 35.2% No, not till the RBI cuts rates further 9.9% I don’t know |

The stock market volatility in the past one year has forced the investors to adopt a defensive stance and opt for guaranteed investments. Little wonder then that the demand for capital guaranteed insurance plans is on the rise, with almost all insurers joining the bandwagon. We review three such products. Mostly single premium products, such policies offer a wafer-thin insurance cover of up to five times the annual premium, with the capital fully protected and a guaranteed return on maturity. The plans are usually structured the way traditional insurance plans are, but the InvestAssure plan from Tata-AIG is an exception. It is based on the Ulip platform.

Available for different tenures, these plans work well as an additional insurance cover. The policies come with a surrender option during the tenure of the policy as well, where the guaranteed addition is lesser than the stated return because of the premature termination of the plan. The guarantees vary depending on the insurance value and tenure of the plan. Then there is the tax benefit to consider. With both Section 80C and Section 10(10D) coming into play, on maturity, these plans are comparable to fixed deposits. InvestAssure also comes with rider options that can be attached to expand the scope of the cover. In addition, you have seven fund options to choose from.

ASSURED RETURNS A look at three capital guaranteed insurance plans | |||

| LIC Jeevan Aastha | TATA-AIG InvestAssure Optima | Aegon Religare Guaranteed Return plan | |

| Entry age | 13-60 years | 30 days to 70 yrs | 90 days to 45 years |

| Policy tenure (years) | 5 or 10 | 10/15/20/25/30 | 7 or 10 |

| Basic sum assured (Rs) | 1.5 lakh and then multiples of Rs 30,000 | 5 times the single premium | 5 times the annualised premium |

— Narayan Krishnamurthy