The recent Sebi diktat to do away with entry loads on mutual funds has resulted in mixed feelings among the three key stakeholders—the AMC, the distributor and the investor. The ruling supports the investor in the long run, but the regulator has taken the decision without understanding the role of the distributor. In any business, the intermediary plays an important role in bridging the gap between the buyer and the seller for a fee or commission.

Unlike other businesses, where products are bought, not sold, financial products are sold, not bought. For instance, 80% of the mutual fund sales are accounted for by the top eight cities, which explains the need for a distributor to push them to a wider retail audience. Moreover, the state of the industry is reflected by the asset it manages, which is skewed towards debt products and corporate money.

Fracas over fees |

|---|

| Commission is paid on insurance, assumed to be sold on advice. |

| Commission is also paid on post office products, PPF and others which involve little advice. |

| AMC pays trail commission of up to 0.5% to distributors who can retain assets for a year. |

| The move encourages distributors to sell high commission products. |

Says Suresh Sadagopan, financial planner: “In the present system, the AMC depends on distribution to push products. This is evident from the commission they earn. Once the new regime kicks in from 1 August, the intermediaries won’t be interested in selling MFs.” As for the 2008-9 sales of equity funds, 33% of the business was routed through independent financial advisers (IFAs), banks accounted for another 32%, and 26% was by national distributors. In January 2008, Sebi allowed a window for investors to bypass distributors and directly invest in AMCs. But, according to the fund industry, the move has been inconsequential, with few takers.

For AMCs, the new regime, with no entry loads and the exit load capped at 1%, means that running the operations will be difficult. The expenses for running the funds will go up, already at about 2% for most equity funds. As a result, the AMCs will find it hard to infuse fresh funds in existing schemes and the new schemes will get, at best, reluctant distributors.

As for the investor, does he really gain from the move? The savvy ones are already putting in money directly in an AMC, doing away with distributor commissions. The average investor is unlikely to benefit: since a fund will no longer be sold to him, the investor will have to either seek advice or buy blindly.

In addition, confusion abounds on the variable fee that one can charge the customers for advice. This will bring the fund distributor on a par with a vegetable vendor, where haggling will dominate the fund selection process. Consequently, the investor is more likely to end up with a fund that is available for less, instead of a fund that suits him.

Says Rajesh Krishnamoorthy, managing director, iFAST Financial India: “It will be tough for a distributor to ask an investor to drop two cheques—one for investing and the other for advisory fee.” There is also a lack of clarity on what happens to SIPs, which account for over 1.25 crore folios. How will the advisory fee be paid and reconciled by the distributor or AMC in this case?

It’s a case of too many cooks. The financial services industry is governed by multiple bodies, such as Sebi, Irda, RBI and now Pfrda, each with a different view on furthering the cause of the industry as well as the investor. There is a need to bring all the financial intermediaries under a single regulator. This will ensure a level playing field that will help develop the industry and enhance financial literacy

- Narayan Krishnamurthy

The number game |

|---|

| Assets managed by insurers: Rs 9,31,000 crore. |

| Assets managed by mutual funds: Rs 4,17,300 crore. |

| In 2008, insurance firms put in Rs 58,000 crore in the market. |

| Mutual funds invested Rs 7,000 crore in the same year. |

| LIC to invest Rs 50,000 crore in 2009-10. |

Market insurers

Every investment talks of the virtues of a long-term, disciplined approach. To some extent, insurance companies do just that for the stock markets. The insurance premium collected by the Ulip policies are regular streams tapped by insurers and put in the markets. Today, at Rs 9,31,000 crore, insurers have twice the total AUM of MFs invested in the markets.

Moreover, they infused Rs 58,000 crore in 2008, when MFs had placed only Rs 7,000 crore. Things are looking up this year too, with LIC alone planning to invest Rs 50,000 crore. Given that insurers parking funds in the market do not face short-term redemption pressure, they don’t have to produce returns on a weekly, monthly or yearly basis. This allows the insurance companies involved to make prudent, long-term investments. This acts as a ballast to the markets. Better still, investment in pension and insurance schemes is set to grow bigger. This assures continued inflow of long-term stable money in the market for several years.

- Narayan Krishnamurthy

Deposit rates on offer |

|---|

| 0-2%: tenures up to 14 days |

| 2.25-3%: tenures of 15-29 days |

| 3.25%: tenures up to 45 days |

| 4%: tenures of 46-60 days |

| These rates are indicative, based on the current rates offered by the leading banks in the country. |

Falling interest

The slowing GDP growth is having a domino effect on the banking system. With export-oriented industries like information technology, textiles and gems and jewellery being severely impacted by the global financial crisis, Indian banks are struggling to sustain the high loan growth rates that they witnessed in the pre-2008 period.

According to the Noble group, banks registered their lowest credit growth rate of 17% in 2008-9. According to analysts, this is likely to put pressure on the banks’ net interest income (NII), which comprises 65-80% of their total income. With the slow credit growth unlikely to pick up till the end of 2009-10, the interest income growth for most banks is expected to be under 12%. This factor, along with concerns about growing bad debts, is making banks look at innovative ways to cut costs. One of them is to cut the short-term deposit rates.

Last year, liquidity crunch had the banks scrambling for short-term deposits (FD) of one year or less, offering interest rates of up to 9.5% for under 100 days. That party is over. Now, the HDFC Bank offers 3% on deposits for 30-45 days, while the State Bank of India offers a 3% interest on deposits maturing in 15-45 days. This is lower than the interest your money would earn in a savings account, which is considered abysmally low at 3.5%.

- R. Sree Ram

Teaser loans

No matter which type of loan you seek, your choice of lender will primarily be dictated by the interest rate quoted. This is the reason banks are trying to lure customers by offering low interest rates, or ‘teaser’ rates, for the first one or two years. Take the State Bank of India (SBI). Given the renewed preference for fixed interest rates, the bank has introduced a new home loan scheme, under which it offers loans of up to Rs 30 lakh at fixed rates of 8% for the first year and 9% for the next two years.

This scheme has been launched on the heels of an earlier offer of loans at a fixed rate of 8% for the first year. Under the new scheme, customers will have two options in the fourth year—a floating rate at 2% below the State Bank advance rate (SBAR), which is currently at 11.75%, or a fixed rate of 1% below SBAR. The rate will be reset after five years. For loans above Rs 30 lakh, you can choose either a floating rate at 1% below the SBAR or a fixed rate of 0.5% below the SBAR from the fourth year, again with a fiveyear reset clause.

SBI also has teaser auto loans. It has cut car loan rates to 8% for the first year and 10% for the second and third years, apart from waiving off the processing charges on these loans.

- Rakesh Rai

Policy snapshot |

|---|

| Entry age: 12-62 years |

| Policy term: 99 minus your age |

| Minimum sum assured: Rs 1 lakh |

| Premium paying term: 8-20 years |

| Riders: Term assurance, accident death, waiver of premium, critical illness and disability. |

A plan for life

The new whole life plan, Future Anand, is designed to meet all your requirements as your life shapes up. Launched by the Future Generali India, the plan is a combination of endowment and whole life insurance, which safeguards you during your lifetime and your dependants after your death. It allows policyholders to choose a short payment term and get back the sum assured along with guaranteed additions and bonuses as maturity benefit, while staying insured till 99 years. There is a 125% life cover after the premium-paying term. Apart from a minimum sum assured of Rs 1 lakh, the policy also comes with five optional riders to enhance the scope of the cover.

Says Jayant Khosla, CEO, Future Generali India: “This policy is an appropriate choice for customers looking for consistent returns amidst continued market uncertainty.” Future Anand comes with guaranteed additions of 3.5% of sum assured per annum for the first five years, compounding annually. From the sixth year onwards, the policy earns compounded reversionary bonuses. Policyholders can also take a loan within the surrender value of the policy. A special feature of the plan is the premium holiday after three years, where the policyholder can choose not to pay premium for up to two years even as the life cover continues.

- Narayan Krishnamurthy

Trading gold

Indians are the largest consumers of gold in the world, buying almost 800 tonnes per annum. But, until now, individuals were forced to buy or sell gold either through jewellers or banks, in the physical form. The National Spot Exchange (NSE) aims to change things by launching gold contracts in denominations ranging from 8 gm to 1 kg.

“This is aimed at the millions of households that hoard gold,” says Anjani Sinha, managing director and CEO, NSE. Like any other market, a contract will be listed and buyers and sellers will quote their price, after which the clearing house will settle the trade. Your broker will charge you a negotiated fee.

If you wish to convert your gold to bars and coins, the refiner will charge a fee of Rs 75 for converting 100 gm of gold— a small price to pay given that it will be vetted by an approved refiner and you will get a certification for purity, weight, etc.

- Tanvi Varma

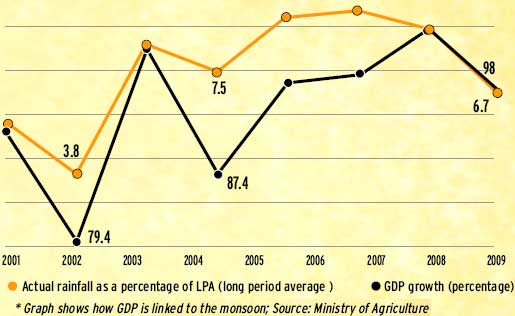

Monsoon may derail GDP growth

According to experts, heavy rainfall over the next month in rain-dependent central and southern India is crucial for agricultural GDP growth.

The Indian Meteorological Department, in its second-stage forecast, has predicted a below-normal rainfall in the country. This will be the first disappointing rainfall in India after 2004.