| Company | LIC Stake (%) | Sale Receipt* |

| Larsen & Toubro | 16.78 | Rs 5,091 cr |

| ITC | 14.35 | Rs 3,089 cr |

| M&M | 17.49 | Rs 1,029 cr |

| ACC | 15.93 | Rs 680 cr |

| Ranbaxy Labs | 15.01 | Rs 555 cr |

| * If the equity is diluted to 10%. Based on prices as on 26 Sep | ||

The Life Insurance Corporation has for long towered over the Indian insurance industry. And it has played the role of a benign giant to perfection—for years, it has come to the rescue of companies it has invested in. And because it is one of the few domestic institutional investors with large sums at its disposal, it could rein in market volatility in case of stock market swings. The Finance Ministry has often asked LIC to check market falls by infusing some capital, or to restrain frenzied sales.

Now, it looks like those days are numbered. The Insurance Regulatory and Development Authority (Irda) has decided that LIC and private insurance players must work on a level playing field. The move will reduce LIC’s equity exposure in a company from 30% to 10%. This means that LIC will lose the clout it has enjoyed for many years through its investments, specifically through its exposure in equity and debt instruments. If LIC were to trim its stake to the Irda-specified levels, it will have to sell Rs 11,821 crore in BSE 100 companies alone, creating an imbalance in the firms where it holds a higher stake. The fear of shares being hammered when sold in large quantities (even in a phased manner) is a matter of grave concern to those companies where the corporation has a higher holding. LIC has also voiced its fears that it may not get a good value on its investments because of the market downturn.

LIC picked up huge stakes in companies because it had developed products with a high interest rate element, which called for long-term investing for it to earn returns for its policyholders. The book value of LIC’s assets is Rs 6,70,000 crore, of which about 16% or Rs 1,07,200 crore is in equities. It has asked Irda to relax the cap to 20% because of its long history compared to the newer private players.

For policyholders, there is cause for concern. The new rules will make investing more difficult for the insurer, which will impact the returns earned on policies. For companies, increasing the share to the public or to large investor blocks will mean stringent corporate governance.

In an earlier war between Irda and LIC, regarding the minimum amount of Rs 100 crore capital, the latter was the winner. Several private insurers have felt that this violates the rules of the game, but LIC claims that a Rs 5 crore capital base is sufficient. The ball is now in the Finance Ministry’s court. It will decide the future course of action not only for LIC but also for the infrastructure projects being undertaken by various government bodies which feature LIC investments.

Irda cracks the whip

• LIC has over 15% stake in ACC , ITC and Ranbaxy Labs

• LIC has over 10% stake in as many as 19 companies listed in the BSE 100

• BSE 100 shares worth approximately Rs 11,821 crore will have to be sold for LIC to adhere to the 10% ceiling

— Narayan Krishnamurthy

WORD’S WORTH  Montek Singh Ahluwalia — Montek Singh Ahluwalia, deputy chairman, Planning Commission “This is not the end of the global financial crisis. Developers are expecting business to pick up during Diwali. But it is unlikely to happen anytime soon” —Anuj Puri, chairman and country head, Jones Lang Lasalle Meghraj “I don’t try to time things, but I do try to price things. I’ve got a formula that says bet on brains, when it’s the right type of deal” —Warren Buffett, CEO, Berkshire Hathaway Inc “We will see a new high by 2010, when the uncertainty in the global markets is diminished and domestic concerns like inflation and high interest rates come under control” —Amitabh Chakraborty, head (equity), Religare Securities Source: Financial Express, Economic Times and Hindustan Times |

Holiday planner

One of the most important findings of the survey, conducted in partnership with the Pacific Asia Travel Association (PATA), is that while the Internet is one of the most popular sources of information on destinations, with 48% claiming they regularly surf for deals, only 12% actually make an online booking. As Vatsala Pant, associate director, The Nielsen Company, says, “While booking over the Net is becoming more popular, visiting a travel agent for direct and personal interaction is still preferred by many Indians.”

— Sushmita Choudhury

Tech troubles

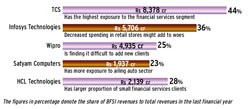

Analysts back home are also worried that about 100 US financial institutions may take the bankruptcy route as they are unlikely get any government intervention since bailout packages have been limited to the larger financial institutions. This will significantly dent the earnings of Indian IT companies. “As we gathered from our visits to the US and Europe, reverberations of the credit meltdown are spilling over to other sectors,” says Viju George, an IT analyst at Edelweiss .

Tech firms are also hit by decreased spending in other business verticals like retail and manufacturing, where the likes of Infosys and Satyam generate significant revenues. The uncertainty on the earnings front is expected to keep IT stocks on tenterhooks—at least for the next year or till the markets settle down—as they would find it difficult to generate new business with favourable margins. Adds George, “Going by the turn of events, it seems that the IT spending will move downwards.”

— R Sree Ram

TELLING FIGURES Numbers speak louder than words. Money Today highlights some numbers that have a short- or long term personal finance implication 20% is the fall in the realty index in the month of September alone. The fall of Lehman Brothers contributed to this—Rs 2,322.3 crore worth of potential investment was expected to flow into real estate projects in India from the investment bank $161 million This is the total exposure India’s top banks—including the State Bank of India, ICICI Bank, PNB, Bank of Baroda and Bank of India— have towards Lehman Bonds 4 large IPOs, namely UTI, MCX, NHPC and Oil India, are likely to be postponed in view of the global financial market turmoil and the meltdown in Indian equities 8% was the rise in the Sterlite stock on the day the parent, Vedanta Group, called off plans for restructuring. The stock had fallen 22% when the group had announced such plans |

Now, an SIP a day

Monthly systematic investment plans are now passé, giving way to a daily SIP concept. Introduced by Bharti AXA Investment Managers, this option, available with their equity fund, extends the concept of disciplined investing. However, the minimum Rs 300 a day rider could restrict the option to a few—not many would be willing to park Rs 9,000 a month in a SIP given that average SIPs range under Rs 2,000 a month according to industry estimates. Though rupee cost averaging will work one level better than monthly SIP, the high entry barrier could act as a damper to many investors.

— Narayan Krishnamurthy

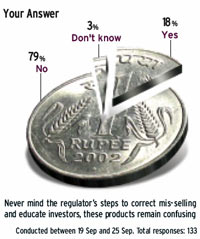

YOUR VERDICT  Our Question: Your Answer: Never mind the regulator’s steps to correct mis-selling and educate investors, these products remain confusing Conducted between 19 Sep and 25 Sep. Total responses: 133 |

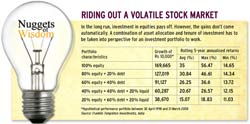

Creating wealth

It’s raining unit-linked insurance plans and insurers attribute this instrument’s burgeoning popularity to the highly volatile stock markets and an unending uncertain phase for most small investors. Cashing in on consumer demand, insurers are coming up with attractive plans that are low cost-low commission and high on allocation. Bajaj Allianz Life’s Fortune Plus is one of the first plans to offer zero surrender charges and high allocation from day one. With a minimum Rs 15,000 annual premium, the policy is very competitive and flexible.

On an annual premium of up to Rs 99,999, 80% of the money will be invested in the first year. The investment would increase to 94% in the second and third year and 98% between the fourth and tenth year. There would be no charges post 10 years, a feature that one should consider if investing for long tenures. The latter is highly advised considering the above 100% allocation on premiums to loyal customers who stay with the policy that long. Says Kamesh Goyal, country manager and CEO, Bajaj Allianz Life Insurance: “The product, designed to offer higher allocation, comes with six riders to expand the scope of cover and also offers unlimited top-ups.” Fortune Plus also offers an asset-allocation fund option that automatically splits the asset-balance depending on the policyholder’s risk profile.

The policy charges for the first three years as well as subsequent charges appear high. In order to offer a product with zero surrender charges, the scheme has loaded higher administration charges for the first three years. For those looking at a low-value insurance scheme with investment prospects can consider this plan, otherwise it is avoidable.

— Narayan Krishnamurthy