Persistence, they say, is the twin sister of excellence. One is a matter of time, the other, a matter of quality. Both life insurance companies and policyholders are learning this now. A recent report by the Insurance Regulatory and Development Authority (Irda) analysing lapsed policies explains the aphorism. Policyholders gain by staying with an insurance policy, and insurance companies benefit by offering better prices and making it possible for the policyholders to stay on.

The various factors for policy lapses include the mode of premium payment, the duration since the policy’s inception, the policy type and the type of underwriting. Most policyholders understand that it is profitable to continue with a policy through its tenure or till the policy reaches a paid-up value, when they can terminate it and receive a surrender value. This depends on the type of policy, the year in which one decides to terminate it and the kind of penalties charged. The Irda report offers a wealth of data that can be used to best effect by insurance companies, brokers and agents. Among other things, the report details the lapse rate over a five-year period. The industry lapse rate increased from 5.62% (2002-3) to 7.8% (2004-5) and then fell to 6.64% (2006-7). Policies are broadly classified as unit-linked and nonlinked. For the former, the lapse rate in the first year has reduced dramatically over the years, thanks to the high front-end loaded cost structure and the high allocation charges.

The Irda report offers a wealth of data that can be used to best effect by insurance companies, brokers and agents. Among other things, the report details the lapse rate over a five-year period. The industry lapse rate increased from 5.62% (2002-3) to 7.8% (2004-5) and then fell to 6.64% (2006-7). Policies are broadly classified as unit-linked and nonlinked. For the former, the lapse rate in the first year has reduced dramatically over the years, thanks to the high front-end loaded cost structure and the high allocation charges.

Another interesting nugget in the report is that the lapse rates for nonmedical policies are higher than for medical policies. Among other things, this seems to indicate that those taking medical covers are very serious about protecting themselves and their dependants.

For insurers, especially new players, this kind of data is very useful. The estimation is beneficial for pricing insurance products, valuation of liabilities and comparison of experience with other countries and for new product development. Also, by identifying the factors influencing the lapse rates, companies can change pricing parameters and marketing strategies of the products or policies that are ready to be launched.

The study helps the policyholders because of the possibility of gains from select ‘with profit’ policies (that declare bonus). They get a cash reward for staying with the policy through the tenure. They can also figure out why some policies might not work for them in the long run. Most importantly, they can also see why it makes sense for them to continue with a policy that gives their financial dependants adequate protection.

— Narayan Krishnamurthy

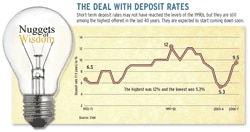

WORD’S WORTH  — K.V. Kamath, CEO, ICICI Bank “A retail investor should not leverage himself (invest borrowed money) and come into the equity market.” — C.B. Bhave, Chairman, Sebi “The less persuaded the investors are that the government will speed up reforms, the more damage breaches of security will do to investor perceptions.” — Subir Gokarn, Chief Economist, Standard & Poor’s, Asia Pacific “We are seeing a global economic downturn of the kind not seen in 70 years. India is now in danger of being drawn into it.” — Pradip Shah, Chairman, IndAsia Fund Advisors Source: The Hindu, The Business Standard and Reuters |

Intelligent ATMs

What the machines can do • Personalise your transactions to cut the time by 40%. • Deposit cash for which receipt will be issued immediately. • Credit deposited amount immediately to the account. • Detect counterfeit currency notes. • Help banks sell specific products depending on customer profile. |

Simply greeting by name is not enough. An intelligent ATM ought to know your preferences too, be it language or the fast cash amount typically withdrawn. That’s exactly what the recently unveiled HDFC Bank ATMs promise to do. Sometime next year, the machines will also be upgraded with the technology to identify counterfeit currency notes that you may deposit inadvertently.

By allowing you to personalise your transaction settings, these ATMs cut down the number of screens you encounter while withdrawing money, from eight on an average to just three, claims the bank. Rahul Bhagat, country head for retail liabilities, marketing and direct banking channels, HDFC Bank, says, “This initiative will reduce the time taken for cash withdrawal by 40% since 45% of our customers use ATM services, 80% of them withdraw the same amount every time and 97% of ATM transactions are done either to withdraw cash or inquire about account balances.”

It is a win-win situation for banks too. A 10% rise in the usage of alternative banking channels translates into around 5% reduction in the transaction costs of the banks.

— Rakesh Rai

Stolen gains

Your credit cards are worth more than you think—in the underground economy. A recent report by security giant Symantec Corp describes a booming online business, where stolen credit cards and personal identity information are traded like legal commodities. By conservative estimates, the total value of advertised goods in this economy was $276 million between July 2007 and June 2008. The report has data recorded from servers hosting this underground economy for more than a year.

Your credit cards are worth more than you think—in the underground economy. A recent report by security giant Symantec Corp describes a booming online business, where stolen credit cards and personal identity information are traded like legal commodities. By conservative estimates, the total value of advertised goods in this economy was $276 million between July 2007 and June 2008. The report has data recorded from servers hosting this underground economy for more than a year.

India is no stranger to such attacks. The customers of reputed Indian banks faced more than 1,000 unique phishing attacks between July 2007 and June 2008. India was also responsible for 4% of the world’s total spam e-mails. E-mails and social networking sites have become favourite phishing grounds lately. “P2P networks are the new emerging targets for such applications. These may appear to do what they are supposed to do, but also carry out some other actions of which the user may not be aware,” says Shantanu Ghosh, V-P, product operations in India, Symantec.

Volatility score

Given the current market conditions, a tool that allows you to revisit your investment rationale may prove beneficial. Fidelity International has launched such a tool that lets you assess the fate of your investment in various scenarios. “At a time when markets are unpredictable and investors are nervous about investing, it is important to provide information that puts current market events in a longer perspective,” says the firm’s MD and country head, Ashu Suyash. The tool has three components that drive its thesis. The first involves timing the market and calculating your loss if you have missed the top 10-40 best performing days since 1998. The second tool helps you understand how longer holding periods can override volatility. Finally, the ‘Market Crises’ tool shows how markets have recovered from past price shocks. For instance, it took almost 28 months for the Sensex to return to the pre-1992 crash levels and about 47 months to recover from the tech meltdown. For details, visit www.fidelity.co.in/market_volatility/index.html.

TELLING FIGURES Numbers speak louder than words. Money Today highlights some numbers with a short- or long-term impact.

47,324 is the number of phishing attacks reported in the first half of 2008 by the Global Phishing Survey conducted by the the Anti-Phishing Working Group. India ranks 11th in terms of unique phishing attacks. 17% is the projected growth for India’s insurance sector in 2008-9. This is subject to the condition that the economy continues to grow at the pace it did in the September quarter of this financial year. |

Shield from turmoil

In uncertain economic times, when everyone is worried about the safety of their investments, any form of financial guarantee is a boon for investors. Capital Shield from Bajaj Allianz is an insurance product that guarantees investment and offers tax benefits. The product is available in two versions—Capital Shield Fund I and Fund II. The difference between the two is the risk that is associated with each. This policy acts purely as an investment. It offers a wafer-thin insurance cover, so if you are looking at this for protection, you would be better off with a pure term plan.

Fund I invests in debt securities, mutual funds and high-rated secured debentures, yet guarantees capital on maturity. Fund II does the same as Fund I, besides investing in corporate bonds, exchange traded funds and money market instruments. So you get to reap the benefits of diversification along with guaranteed capital protection. On maturity, you get the capital and maturity benefits. Your investment will be unitised, so you will get a sense on the unity value of the underlying asset. As for the charges, you have to pay a 2% allocation charge for contributions less than Rs 5 lakh and 1% on higher amounts. The fund management charge is 2.75% for Fund I and 3.25% for Fund II, with mortality charges and a surrender charge if you exit before maturity.

Then there is the tax benefit under Section 80C on the contribution and under Section 10(D) on maturity. “This policy completely safeguards our customers’ investment and offers a win-win situation,” says Kamesh Goyal, CEO, Bajaj Allianz Life Insurance.

YOUR VERDICT We bring you the results of Money Today online poll on select and current investing issues. Our question Clearly, the brouhaha about retrenchment and slower hiring has not sent alarm bells ringing, yet. |