WHAT INCREASED FDI MEANS • Health insurers to look at expanding operations. • More pension plans likely to be launched. • Expect niche, customised insurance products. |

It has taken long enough to stage an appearance and already there are complaints about arriving after the party is over. The Indian Cabinet has finally given the nod to the proposal to hike the foreign direct investment (FDI) cap in insurance from 26% to 49%. While the move is a welcome step for the cash-intensive business, as it will enable the players to garner capital for expansion, many are arguing against the timing of the move. A majority of partners in the Indian ventures are from the US and the UK. Given the state of most foreign insurers on their home turfs, it’s unlikely that they will come rushing to increase their stakes in India at the moment.

However, one cannot deny that the move is vital for the growth of the Indian insurance industry. Eight years after the sector was opened, the drab insurance business has emerged as the fastest growing segment in financial services. Currently, there are 20 players in life insurance—13 players vis-a-vis four stateowned companies in the general insurance business and three players in the standalone health insurance business— compared with the LIC monopoly. This has been the trigger for some radical shifts in the way insurance touches our lives today. With a CAGR of over 25% in life insurance business, the hike in foreign holding will help ensure long-term capital to maintain the growth momentum and increase insurance penetration. For instance, the current FDI in the life insurance segment alone is pegged at about Rs 5,200 crore. But after the hike comes into effect, it can easily go up to Rs 10,000 crore.

As and when insurers queue up to start operations in India, the increase in competition will raise the existing benchmarks. The move will not only enable the sector to aggressively expand business, but also introduce products that are more sophisticated and custom-designed to meet specific target groups. It will also propel the health insurance sector. Though it is in a nascent stage, it will, in all likelihood, make the most of this amendment to expand its footprint using fresh capital.

The pension products from insurers is another area that will witness renewed activity, with longterm care plans grabbing the limelight when it comes to financial planning for retirement. As for the stakeholders, this development will be a trigger to consider going public and listing on the stock exchange. But don’t rush to pop the bubbly yet. According to industry players, the actual passing of the bill is unlikely to happen anytime soon; it will be taken up after the general elections and could be a year before one actually sees any activity. Also, if you are hoping to garner some benefit as a consumer, say a drop in prices, you have a long wait ahead.

— Narayan Krishnamurthy

Posting gains

The small savings schemes offered through post offices are inversely related to the stock markets. While the market was booming, the post-office deposits were emptied out by the investors. But they are seeing a fresh inflow of deposits these days. Despite the lower interest rates offered by these schemes compared with fixed deposits (FDs), their high safety quotient has attracted many investors.

And how! The postoffice accounts have grown by 35%, the highest growth posted among small savings schemes, followed by recurring deposits (21%), monthly savings schemes (19%) and small savings certificates (6%). What might come as another boost to small savings schemes is a proposal with the Finance Ministry that recommends an upward revision of the tax-free interest limit.

Currently, the interest accrued on deposits of Rs 1 lakh in single accounts and Rs 3 lakh in joint accounts is tax-free. Post office savings emerge a clear winner when you consider that the current appeal of FDs is unlikely to last. As lending rates are headed downward after RBI’s efforts to increase liquidity, banks will be forced to cut deposit rates to balance it.

Post-office deposits regain lost ground Net collections have grown four times since July ’08 | ||||

| Gross collections (Rs cr) | Net collections (Rs cr)* | |||

| 2007 | 2008 | 2007 | 2008 | |

| June | 31,000 | 31,600 | -3,209 | 957 |

| July | 42,000 | 43,900 | -4,500 | 700 |

| August | 58,000 | 68,000 | -7,200 | 4,000 |

| * Collections after deducting withdrawals | ||||

— Rakesh Rai

Today, less than four in 10 bills are paid electronically in the country. But don’t write off India as a slave to cash transactions just yet because the payment system is fast waking up to the electronic potential. According to a report, Payments in India Going the e-Way, by Celent, the retail e-payment market will grow at 65-70% in the next two years. The value of e-transactions by 2010 will be almost $180 billion. E-payments have posted over a 60% growth in the past three years.

Today, less than four in 10 bills are paid electronically in the country. But don’t write off India as a slave to cash transactions just yet because the payment system is fast waking up to the electronic potential. According to a report, Payments in India Going the e-Way, by Celent, the retail e-payment market will grow at 65-70% in the next two years. The value of e-transactions by 2010 will be almost $180 billion. E-payments have posted over a 60% growth in the past three years.

According to RBI, over the past year itself, the volume of credit card transactions has grown 35%, the highest rate posted so far. The volume of debit card transactions is growing even faster—up 46% from 2006-7. It’s not just cards; other electronic modes of payment such as ECS and electronic funds transfer (NEFT) are also gaining ground. According to the report, about 83% customers make payments via a bank Website because they consider it safe and secure. About 43% customers pay bills on the biller’s Website directly and about 21% pay via third-party service providers. At this rate, standing in queues to pay bills or carrying a wallet bulging with cash will soon be a thing of the past.

— Namrata Dadwal

Travel planner

If you have to travel from Delhi to Gaushala, a small town in Uttaranchal, the travel planning would involve booking a combination of flight, train and bus tickets separately. Now comes a travel portal that does this work for you in seconds. At www.nearhop.com, all you have to do is to key in the first three letters of the place of origin and the destination, pick the suitable option from the drop-list and hit search. It will plot out all the combinations that will take you there. For instance, the Delhi to Gaushala search yields a bus ride to Ramnagar and then a train trip. In addition, you get the details of departure and arrival time, duration and fare. Not only can you book the tickets online, but the site also allows you to choose the timegap between switching the modes of transportation. Currently the site covers only around 5,200 places, but this is a good first step.

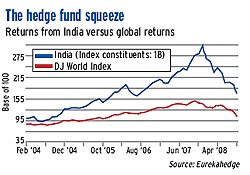

The fall has been equally sharp this year—the India-focused funds have booked losses to the tune of 46% in 2008. This is worse than their returns from other emerging economies like China (-31%), Russia (-34%), Brazil (-14%), Japan (-13%) and the US (-7%).

What went wrong with the India bet? Most of the top hedge funds had a big exposure to the real estate and financial sectors, which were the worst affected when the Indian markets suffered a free fall. Their highly leveraged positions made matters worse for the hedge funds. Then there was the redemption pressure from clients back home, which was triggered by the global financial turmoil. As a result of all these, many of them were forced to sell their shares at a discount. The slide in the value of the rupee has been the final nail in the coffin for hedge funds as they are bagging fewer dollars at the time of conversion.

— Rakesh Rai

Word’s worth

“We expect interest rates to soften, taking into account the liquidity conditions.”

— T.Y. Prabhu, Executive Director, Union Bank of India

“If the growth outlook is as good as is being claimed, the public is entitled to demand a rationale for the desperate policy measures being taken (by RBI) to boost liquidity.”

— V. Anantha Nageswaran, Head, Research, Bank Julius Baer

“Barack Obama will be a change agent. Any comment on outsourcing should not bother us. Once he is in office, he will realise that countries have to work together.”

— P. Chidambaram, Finance Minister

Source: The Economic Times, The Times of India and Mint

Telling figures Numbers speak louder than words. Money Today highlights some numbers that have a short- or long-term personal finance implication. 15,000 tonnes is the quantity of gold tucked away in India’s private family vaults, according to McKinsey. This is nearly double the bulk of gold in the US Federal Reserve. Rs 1 trillion is the total lending by banks and housing finance companies to home buyers in 2007-8 and the total outstanding mortgage debt is well over Rs 3 trillion. $1,789 is the amount Indians spend per person on a leisure holiday abroad. Other than travel and accommodation, the biggest expense is shopping for global branded goods. 16% is the projected hike in Indian salaries in 2009, according to compensation firm, HR Business Solutions. This is expected to be among the highest in Asia. |

YOUR VERDICT We bring you the results of MONEY TODAY online poll on select and current investing issues. Our question Clearly, Indians are able read the signs correctly because the PSU banks have already started cutting the rates Conducted between 29 Oct and 6 Nov. Total responses: 141 |