If you have been waiting for an opportune time to take that home loan, or a car or education loan, you’d best not defer your decision much longer. The downward spiral of interest rates that gave so many so much cause for hope may be coming to an end. There are murmurs among bankers that interest rates are firming up and might rise over the next 4-5 months. Says O.P. Bhatt, chairman, SBI, “Interest rates may go up by 25-100 basis points if liquidity is not managed well when the busy season picks up.”

The RBI uses interest rates swings to influence the economy. So, when the economy weakens, it may decide to lower the interest rate because that will make money flow more freely and, hopefully, stimulate economic growth. On the other hand, interest rates are hiked to make loans less attractive and, thereby, rein in inflation. So what could be the reason for the rate cut party winding up this time round? The culprit is the central government’s borrowing programme, which the finance minister had indicated in his budget speech.

The pressure points |

|---|

| Bank loan growth is expected to pick up as the economic activity revives. |

| Corporate demand is likely to pick up in the third quarter. |

| States and local bodies may come out with their own borrowing programmes. |

| With inflation going up again, RBI may tighten monetary policy. |

Here’s how things will pan out: to finance the fiscal deficit, the government will borrow around Rs 4,00,000 crore in the current fiscal, which will cause interest rates to firm up. The various state governments and local bodies that are likely to hit the street with their own borrowing programmes will further compound matters. When the government needs to borrow large sums of money, it has to offer higher interest rates to attract investors. While the increased borrowing will suck out liquidity from the market, it also means that interest rates may move northwards.

Furthermore, bank loan growth has slowed to 15% in June this year compared with the 30% it achieved in 2007-8, which will add to the liquidity concerns in the coming months. Though the finance minister has been repeatedly claiming that government borrowings will be managed in a manner that will avoid an interest rate hike, the banking body is not convinced.

The other concern is inflation, which is likely to build up in the coming months on account of rising food prices, the hike in petroleum products and the modest revival in prices of manufactured products. “With deficient rainfall, the risk of rise in the consumer price index is real. When the consumer price index (CPI) moves up, consumers (depositors) may expect banks to protect their returns on deposits. In such circumstances, banks may have to increase deposit rates,” says V.K.R. Agarwal, CFO, Bank of India.

What does this mean for consumers? This is a good time for borrowers to take advantage of the existing low rate to get locked into loans which are fixed in nature. Investing in floating rate funds and debt funds is also a good way to shield your investments from the vagaries of fluctuating interest rates.

- Narayan Krishnamurthy

Holiday Hotspots |

|---|

| 67%: Historic sites |

| 54%: National parks |

| 47%: Adventure spots |

| 41%: Spa resorts |

| The preferred destinations that Indians like to visit while travelling |

Travel trends

There was a time when a pilgrimage was the most obvious holiday option for Indians. Today, sole therapy is more in demand than soul therapy, as TripAdvisor’s latest annual travel trends survey reveals. This summer, a majority of Indians chose to travel within the country, along with choosing budget hotels for their stays. Says Sharat Dhall, managing director, TripAdvisor India, “The slowdown has made travellers re-discover Indian destinations in preference over international travel itineraries which were popular over the past couple of years. We are using the slowdown as a great opportunity to reconnect with our roots.”

The economic climate has also shrunk travel budgets. While 60% of the travellers surveyed said they looked for cheaper air tickets on travel Websites, 50% booked their travel in advance to take advantage of low fares. Of the 54% of respondents who chose value-for-money accommodations for their leisure stays, 32% preferred hotels where a room was priced at less than Rs 2,000 a night. However, the rich and upwardly mobile continue to live it up—more than 11% of travellers indicated that they spent upwards of Rs 2 lakh on vacations and plan to continue doing so. In terms of emerging trends, 45% of respondents said they would like to be more environmentally conscious during their travel in the coming year and to choose an eco-friendly hotel for their stay.

- Sushmita Choudhury

Refiling a claim

Don’t let the recent crop of consumer court judgements give you the idea that you can challenge your insurance company for refusing a claim on the grounds of inaccurate information. The Supreme Court has now declared that insurance companies can repudiate a mediclaim policy if accurate and complete information is not furnished by the policyholder. According to the court, a mediclaim policy is a non-life insurance policy and a contract of utmost good faith. Also, it is not for the proposer to determine whether the information sought by the insurance companies is material for the purpose of the policy or not.

In another significant ruling, the apex court has held that in motor accident insurance claims, the compensation fixed by the official surveyor need not be the final word. “The approved surveyor’s report may be the basis or foundation for settlement of a claim by the insurer, but, surely, such a report is neither binding upon the insurer nor insured,” observed the bench of Justices D.K. Jain and R.M. Lodha. The ruling could bring relief to many claimants as, usually, the compensation fixed by the insurance companies is based on the surveyor’s assessment, which invariably is lower than the amount claimed by the policyholder.

- Rakesh Rai

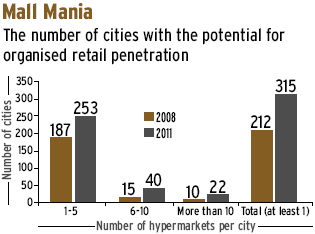

One-stop shops The retail sector seems to be slowly swinging towards hypermarts, a one-stop shop for everything from needles to automobiles. According to a recent KPMG and Assocham study, nearly 315 of them are expected to come up in tier I and II cities by 2011 as, by then, the economy will have recovered from the crisis. With the organised retail sector growing at 20% a year, the mushrooming malls are expected to eventually pave the way for hypermarkets.

The retail sector seems to be slowly swinging towards hypermarts, a one-stop shop for everything from needles to automobiles. According to a recent KPMG and Assocham study, nearly 315 of them are expected to come up in tier I and II cities by 2011 as, by then, the economy will have recovered from the crisis. With the organised retail sector growing at 20% a year, the mushrooming malls are expected to eventually pave the way for hypermarkets.

The study, Reinventing India’s Retail Sector, points out that 212 towns boasted sufficient market potential for hypermarkets in 2008. Says Sajjan Jindal, president, Assocham, “Given the expected growth in the number of households as well as in the income and consumption per household in urban India, five or more hypermarkets per city are feasible even in 2009.” By 2011, this number is anticipated to grow to 52 as a few tier III towns also gain the market potential to support five or more hypermarkets.

- Sushmita Choudhury

QIP Blip

Did you know that India Inc. raised Rs 11,714 crore in the first quarter of the current financial year, up from Rs 2,623 crore raised in the corresponding period in 2008? The key vehicle for most companies was qualified institutional placements or QIPs. With as many as 10 companies raising Rs 11,259 crore, QIPs cornered 96% of the total money mobilised.

However, according to a Crisil study, 10 out of 13 QIPs are trading below their offer price. Says Chetan Majithia, head, Crisil equities, “The run-up in the stock prices before the budget made QIP deals unattractive as the inherent fundamentals of the interested companies had not changed materially.” This may also mean that many will turn to the primary market to raise funds. “Most companies have been waiting for a stable or buoyant secondary market, a pre-requisite for raising fresh capital. If the market goes up, one can hope for a steady stream of issuances,” says Prithvi Haldea, CMD, Prime Database.

- Rakesh Rai

Policy Snapshot | |

|---|---|

| Age at entry | 18-55 years |

| Sum assured (Regular premium) | 30 times the annualised premium if age at entry is up to 40 years. |

| 20 times the annualised premium if age at entry is 41 years and above. | |

| Sum assured (Single premium) | 5 times the premium if age at entry is up to 40 years. |

| 2.5 times the single premium if age at entry is 41 years and above. | |

Joint venture

Given the growing popularity of the unit-linked model, the Life Insurance Corporation has now taken its popular joint life policy, Jeevan Saathi, to the Ulip platform. Called Jeevan Saathi Plus, the new policy is similar to an endowment policy, offers maturity benefits and covers the policyholders for risks like a regular life insurance policy. The proposer under the plan is called the principal life assured (PLA) and the wife/husband is the spouse life assured (SLA).

The PLA can choose the level of cover for both lives within the limits, which will depend on the age, whether the policy is a single premium or regular premium and the amount of premium payable. For regular premium policies, in case of death of the PLA during the term of the policy, the plan also provides for waiver of all future premiums including outstanding ones, if any, provided the life cover is in force.

The policy works well cost-wise at it reduces the administration costs that double up in case of two individual policies. The investment component offers four fund options, ranging from conservative to growth. There is also a provision for premium top-ups without changing the sum assured. However, the policy does not offer any rider options, which restricts the scope of cover.

- Narayan Krishnamurthy

Use the consumption basket to pick stocks

A look at sectors that are likely to be good investment picks in the near future.

A look at the rural consumption basket, compared to the urban consumption, gives a fair idea of the sectors that are likely to benefit from the centre’s renewed focus on rural spending. The rising food prices (food bill is the single largest component of consumption) will also impact spending.