Call it an institutioal SIP (systematic investment plan). Every month, the insurance companies receive a steady inflow from Ulip collections. Every month, they invest those sums systematically across the stock market. That gives the Ulip an edge in terms of lower average costs and helps it combat volatility in the same way as an SIP does. Since the Ulip corpus is massive enough, it acts as a stabiliser for the entire market and it provides a lifeline to those businesses that need really long-term funding. India’s capital markets can finally boast of an institutional backer of last resort; the Ulip funds have the potential to act as a counter-balance to panic withdrawals and to give the markets a solid foundation.

The net effect is a win-win situation for everyone. The Ulip-holder gets excellent long-term returns (while usually being unaware of the fact that he has a big market exposure). The stock market benefits from a stable assured inflow. And infrastructure gets the type of funding in terms of a large quantum of longterm funds.

The net effect is a win-win situation for everyone. The Ulip-holder gets excellent long-term returns (while usually being unaware of the fact that he has a big market exposure). The stock market benefits from a stable assured inflow. And infrastructure gets the type of funding in terms of a large quantum of longterm funds.

When it comes to stock investing most investors think long term but act short term. But some of the companies’ stocks they invest in, especially infrastructure- related ones, have very long gestation periods. Something like an airport project or a power project requires massive initial investments followed by many years of waiting for returns. During that period, patient support is required from investors. But market sentiments or dynamics often leads to short term investing.

Even mutual funds and other institutions face quarterly reporting compulsions that lead to short-term investment styles. Any dip in the market creates a vicious cycle where institutions are hit by redemption pressures as well. In the US, the pension funds perform the vital role of providing long-term support. The pension funds can think in the timeframe of decades; there’s no fear of sudden redemption.They can get into projects which require years to give returns.

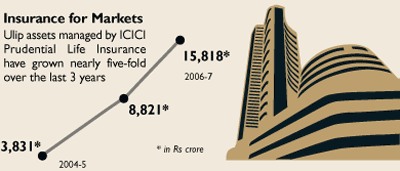

This is similar to the role Ulips have begun to play in Indian market. Thanks to this hybrid instrument, Indian insurance companies have now started to play role of the long-term investor. Since 2005, life insurance premium collection has grown by 300% and around 80% of that money has come in the form of Ulips. We’re talking of sums of the order of Rs 49,174 crore at least. The best thing about a Ulip is that it has a lock-in period of three years and, in practice, the average Ulip-holder is prepared to wait 6- 7 years or longer. That gives the insurance companies freedom from the fear of redemption and the leeway to invest for the long term.

Forget about redemptions, insurance companies don’t even suffer reduced inflows when the market dips! Since the average Ulip-holder is thinking in terms of insurance, his decision to take out a policy is not influenced by market fluctuation. This is what makes Ulip an institutional sort of SIP . Ironically, the dynamics would probably change for the worse if the average Ulip-holder was more aware of the nature of the instrument. Then, inflows would be more correlated to market fluctuations. This is one situation where ignorance is truly bliss!

Narayan Krishnamurthy

Falling in line

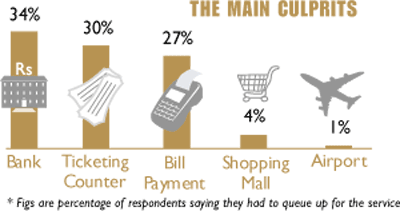

As a nation we have a penchant to stand in queues; be it at bus stops, ration shops, ATM counters and even parking lots. But these queues don’t go well with the average consumer. A recent “Queue Frustration” survey undertaken by AC Nielsen in five metros (Mumbai, Delhi, Kolkata, Chennai and Bangalore) reveals how 84% of the respondents spend close to an hour waiting in queues. People in Chennai spend the most time, 59 minutes, at queues followed by Mumbai, where people line up for 52 minutes. People in both the metros spend far more time in queues compared to the average time spent by those surveyed.

According to the survey, more respondents claim to have become less patient about being in queues especially at banks, ticketing counters and bill payment centres where most of the problems originate. It’s not surprising to find people getting angry and changing service providers because of the time wasted. The survey suggests multiple queues and self-service solutions for reducing queuing-related frustrations. There are also those who advocate the display of wait time in queues to give people a fair idea of how long it will take. For service providers where queues are inadvertently long, a point to note—26% of those surveyed switched service providers offering better self-service solutions. For the respondents, with an average income of Rs 14,500, spending 49 minutes a week in queue means losing Rs 65 a month or 0.5% of their income. Time indeed is money.

Narayan Krishnamurthy

The Truth about TDS

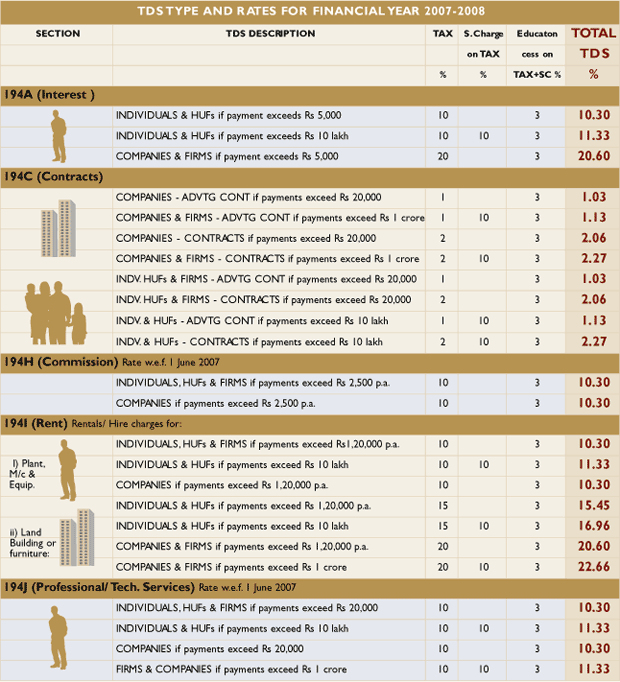

For those of you wondering exactly what changes have been introduced in the IT arena courtesy the Finance Act 2007, here is a ready reckoner. The threshold limit for exemption from deduction of tax at source has been enhanced for women and senior citizens. Also, a new cess (secondary and higher education) at 1% of income tax and surcharge will be applicable in addition to the existing education cess of 2%. While the the rate of deduction of tax at source has gone up in most cases, the TDS for renting or hiring machinery or equipment has actually come down by 5- 10%. Take a look:

SMS to Mint Money

Tired of receiving endless and futile messages on your mobile phone by advertisers from all over? Or tired of cribbing about your mounting phone bills?

Check out mGinger, a new Bangalore-based website which actually pays you to read such ads on your cell phone besides giving useful information. All you need to do is log on to their website, sign up with your cell number, specify your interests and preferences and invite family and friends to register for the same.

It gives you the benefits of getting SMS ads of only those products that you want to buy, over and above a chance to save money through discounts and offers. Says Chaitanya Nallan, CEO, mGinger, “Our aim is to help eliminate spam and build a social network between the advertisers and consumers so as to provide correct and relevant information.” Though only 10 advertisers have joined hands with this new medium since its launch in April 2007, mGinger is notching up increasing popularity with around seven lakh registrations already.

The team is hopeful that in the next few months, they will have many more. Agrees Nallan, “We have done nine campaigns so far and this is just the beginning. However, we do not want to fool our customers with any false claims. Do not think that it will make you rich instantly.”

What cannot be denied is that this is a unique, one-of-its kind scheme in India. And if it helps one earn some extra bucks, then it’s definitely worth a try.

Sonia Sahijwani

Withdrawal Symptoms?

Not too long ago, the Indian stock markets were at the whims and fancies of foreign institutional investors (FIIs). But in the past two years, the correlation between FII confidence and the stock markets has waned—net equity investments by FIIs dipped from Rs 5,431 crore in April to only Rs 443 crore in June. Yet the markets hardly took note.

Perhaps that’s because the markets are far more stable now. Mutual funds and insurance companies are sitting on massive piles of cash collected from investors in Ulips and NFOs. This money would willingly flow into a position vacated by FIIs.

There’s another reason though. The drop in the net investments by FIIs in the secondary market is more than made up in the primary market. When ICICI Bank’s follow-on public offer opened in June, Warburg Pincus applied for shares worth Rs 5,000 crore—over 50% of the Rs 8,750 crore issue. Temasek Holdings too applied for shares worth Rs 3,000 crore. So FIIs’ ravenous appetite for Indian equities isn’t really satiated, it’s just that markets don’t dance to their tunes as much.

Babar Zaidi

The big home hoax

Villas available in 100, 150, 200, 400 sq yard with modern facilities…in a selfsufficient township that has become the address of the elite.” What is the first thing that comes to your mind on reading this advertisement? That the villas are ready and you just have to pay and start living, right? Wrong. Many such ads come out even before the builder has got the relevant clearances for the project.

The antimonopoly watchdog, MRTPC , has now taken up cudgels against one such developer, Delhi-based Arun Dev Builders. Acting on the investigation report submitted by its investigative arm, Director General of Investigations and Registration (DGIR), the MRTPC has issued a notice of enquiry against them.

According to the report, Arun Dev Builders are guilty of false representation of their township projects in Uttarakhand and Rajasthan through misleading advertisements. In its advertisement titled “Operation Grih Pravesh” in various newspapers, the builder claimed it would hand over two-room flats for an EMI of just Rs 2,000 over 20 years, along with a registration fee of Rs 25,000. The DGIR claimed that the commercial created an impression that the flats were available for immediate possession; the title in the advertisement giving further credence to the belief that its township schemes were completed.

Secondly, in its booking plan, the builder assured customers that the flats would be handed over within a year. However, a detailed investigation of these projects in Jaipur and on the Roorkee-Dehradun Highway revealed that these projects were still at the drawing board stage.

For the Rajasthan project, they bought some agricultural land and claimed they had the official nod to build on it. However, they failed to furnish any documentary evidences for the same. The DGIR also found that the builder had not acquired any land in Uttarakhand for its project. Worse, the downloadable form from the firm’s website did not guarantee allotment. It also included a clause that the registration would be cancelled if the buyer defaulted on EMI payment.

Interestingly, during the proceedings of the Commission, Arun Dev Builders claimed that they had stopped releasing such advertisements and pleaded against a judicial inquiry. However, the Commission turned down the request and listed the matter for 10 September this year.

If the MRTPC wins this battle, starry-eyed hopefuls will no longer lose their hard-earned money over a pipe dream.

Rakesh Rai