The initial public offering (IPO) of CL Educate, an integrated, technology-enabled education provider, was oversubscribed 1.9 times on the last day of the offer today. It received bids for 63.26 lakh shares as against the total issue size of 33.32 lakh, according to the exchange data. The IPO also had a fixed price band of Rs 500-502. At the lower end of the price band, the issue size worked out to Rs 238 crore while at the higher end, it amounted to Rs 238.95 crore. The issue managed to sail through on the last day, would it list at a significant premium, given its unimpressive financial performance?

CL Educate focusses on diverse education segments. Its asset-light, technology-enabled business model and well-recognised brand Career Launcher ascertain its strong brand equity. In addition, the company operates K-12 schools under the Indus World School brand name. As on September 30, 2016, the company had 151 test-prep centres in 87 cities, eight K-12 schools in six cities and 28 vocational training centres and offices. It has also diversified its operations across various business segments, including service segments such as test preparation and training, publishing and content development, integrated business, marketing and sales for corporate, vocational training and integrated solutions for educational institutions.

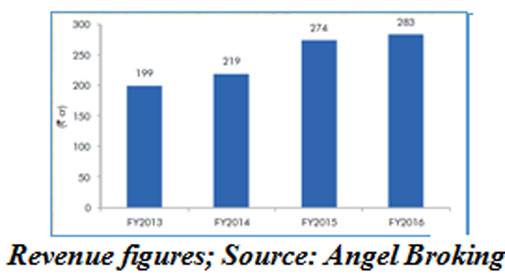

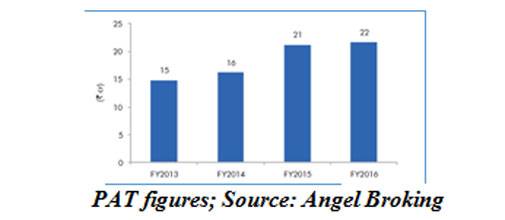

However, its weak financial performance is one big concern. The company's overall financial performance had not been impressive over the past 4-5 years. "Profits have been low and fluctuating, which do not give a significant quality to business," says Amarjeet S Maurya of Angel Broking in his IPO note.

CL Educate lagged behind its closest peer MT Educare both on top line and bottom line during FY2013-16. It registered a compounded annual growth rate of around 12 per cent compared to MT Educare's approximately 22 per cent growth in revenues over the same period. With around 13 per cent growth in profit after tax, it was much behind MT Educare, which recorded around 21 per cent growth over these four years.

Incidentally, over 45 per cent of the company's revenue comes from institutional businesses such as corporate training, vocational training under government schemes, and advisory and research incubation services to educational institutions/universities, which has resulted into stretched working capital cycle--it has increased from 89 days in 2012/13 to 130 days in 2015/16.

"K-12 vertical under Indus World Schools has nearly 60 per cent of the company's capital deployed, which has resulted in lower profitability and return ratios," adds Maurya in his IPO note.

In terms of valuations, at the upper end of the issue price band, the pre-issue P/E worked out to 23.2x its annualised H1FY17 earnings, which is higher compared to its peers (MT Educare is trading at 8.9x its annualised H1FY17 earnings).

The company's EV/sales multiple at 2.1x works out to be at premium to MT Educare's 1.2x. Compared to its peers, the margins and the ROE profile of the company do not appear to be attractive.

"The company's business is working capital-intensive, which, coupled with expensive valuations, may not provide a significant upside to the investor," says Maurya.

is signed.") India-US BTA: Harley Davidson bikes to get 0% duty, gradual tariff reduction on luxury cars

India-US BTA: Harley Davidson bikes to get 0% duty, gradual tariff reduction on luxury cars India-US interim trade agreement: 'No GM modified product allowed, agri sector protected,' says Piyush Goyal

India-US interim trade agreement: 'No GM modified product allowed, agri sector protected,' says Piyush Goyal 'Decided to give 0% tariff on some cancer medications, neuro treatment': Piyush Goyal on what US got

'Decided to give 0% tariff on some cancer medications, neuro treatment': Piyush Goyal on what US got ‘How is this a win?’: Chidambaram slams India-US trade framework as opaque, US-tilted

‘How is this a win?’: Chidambaram slams India-US trade framework as opaque, US-tilted Qualcomm’s ‘tapes-out’ 2nm chip design with their Indian design labs

Qualcomm’s ‘tapes-out’ 2nm chip design with their Indian design labs  BT Golf 2025-26 Kochi, Kerala Awards Ceremony Marks A High-Energy, Successful Conclusion

BT Golf 2025-26 Kochi, Kerala Awards Ceremony Marks A High-Energy, Successful Conclusion Golf Is An Addiction. We Eat And Sleep Golf!

Golf Is An Addiction. We Eat And Sleep Golf! The Fairway Fixes Everything. Mindset, Life, Relationships

The Fairway Fixes Everything. Mindset, Life, Relationships BT Golf LIVE: Join AU Small Finance Bank Presents BT Golf 2025-26 For Its 4th Leg In Kochi, Kerala

BT Golf LIVE: Join AU Small Finance Bank Presents BT Golf 2025-26 For Its 4th Leg In Kochi, Kerala AI Will Change MBAs, Not Leadership: IMD President On India’s Global Education Rise

AI Will Change MBAs, Not Leadership: IMD President On India’s Global Education Rise RIL, SBI, Kotak Bank, Kalyan, HAL, BEML, BDL among stocks in focus next week; here’s why

RIL, SBI, Kotak Bank, Kalyan, HAL, BEML, BDL among stocks in focus next week; here’s why NSE IPO may unlock mega gains for billionaire investors RK Damani, Premji

NSE IPO may unlock mega gains for billionaire investors RK Damani, Premji SBI Q3 Results: Profit jumps 24% to Rs 21,028 crore; asset quality improves

SBI Q3 Results: Profit jumps 24% to Rs 21,028 crore; asset quality improves IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’

IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’ BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week

BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week