BEL’s order inflows for the first nine months of FY26 are estimated at about Rs 18,600 crore, placing it well on track to meet its full-year guidance of Rs 27,000 crore.

BEL’s order inflows for the first nine months of FY26 are estimated at about Rs 18,600 crore, placing it well on track to meet its full-year guidance of Rs 27,000 crore.Nomura expected order inflows across its capital goods universe to decline 19 per cent year-on-year (YoY) to about Rs 1,30,000 crore in Q3FY26, led by an unfavourable base, limited traction in ultra-mega orders, continued sluggishness in short-cycle orders and the absence of a broad-based pickup in private capital expenditure. The brokerage said order inflows during the quarter were largely driven by the power transmission, hydrocarbons, buildings and factories, and minerals and metals segments.

Nomura estimated L&T’s core order inflows at around Rs 67,300 crore in Q3FY26, marking a 32 per cent year-on-year decline due to the high base of Q3FY25 and the lack of ultra-mega orders during the quarter. It said inflows were supported by large orders in the hydrocarbons and metals and minerals segments, along with wins in power transmission and distribution and buildings and factories.

For Hindustan Aeronautics Ltd (HAL), Nomura assumed repair, overhaul and spares order inflows of about Rs 5,300 crore in the absence of meaningful manufacturing contracts, implying a 68 per cent year-on-year decline on a high base. In contrast, the brokerage estimated BEL’s order inflows at around Rs 5,600 crore, translating into 148 per cent year-on-year growth on a low base. It said BEL’s order inflows for the first nine months of FY26 were estimated at about Rs 18,600 crore, placing it well on track to meet its full-year guidance of Rs 27,000 crore.

Nomura expected KEC International to report order inflows of about Rs 7,600 crore, up 25 per cent year on year, led by the power transmission and distribution and cables segments. It estimated Afcons Infrastructure’s order inflows at around Rs 1,460 crore during the quarter.

For short-cycle orders, Nomura said channel checks indicated moderate momentum. It estimated ABB’s order inflows at about Rs 3,390 crore, up 26 per cent year on year, while Siemens’ order inflows were estimated at around Rs 4,500 crore, reflecting 6 per cent year-on-year growth.

Nomura expected CG Power to record order inflows of about Rs 4,350 crore, marginally lower year on year, supported by two orders worth around Rs 330 crore from Power Grid in December 2025. For GE Vernova T&D India, the brokerage estimated robust order inflows of about Rs 12,000 crore, led by a high-voltage direct current order win.

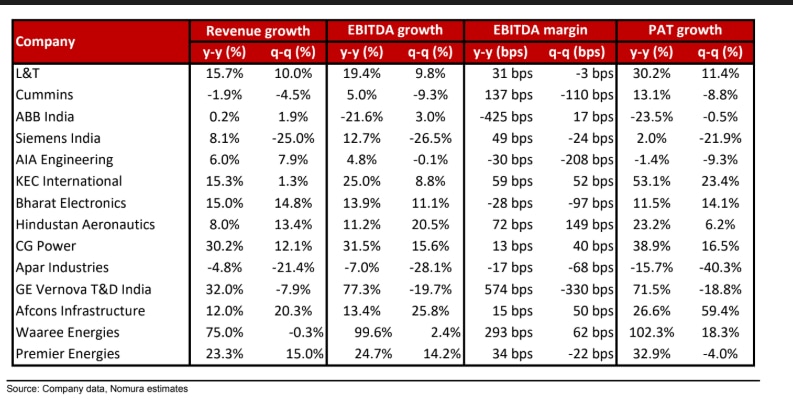

On execution, Nomura expected strong outstanding order books to sustain revenue growth, with the coverage universe seen reporting 15.3 per cent year-on-year revenue growth in Q3FY26. It estimated L&T’s core execution growth at 21 per cent year on year, driven by infrastructure and hydrocarbons. KEC International’s revenue was expected to grow 15.3 per cent year on year, led by power transmission and distribution.

Among power ancillaries, CG Power was expected to post revenue growth of 30 per cent, with power systems and industrial systems growing 53 per cent and 10 per cent respectively. GE Vernova T&D India’s revenue was seen rising 32 per cent year on year, while ABB’s revenue was expected to remain largely flat. Nomura expected Cummins to report a 2 per cent year-on-year decline in revenue due to weakness in the power generation segment, partly offset by growth in exports and distribution and industrial segments.

Nomura expected solar equipment manufacturers to report robust growth in Q3FY26, driven by order execution and stabilisation of new plants. Waaree Energies Ltd and Premier Energies Ltd are estimated to deliver revenue growth of 75 per cent and 23 per cent respectively. In defence, Nomura estimated BEL’s Q3FY26 sales at about Rs 6,600 crore, up 15 per cent YoY, while HAL is expected to report sales of around Rs 7,500 crore, up 8 per cent.

On margins, Nomura estimated Ebitda margins for the coverage universe at around 13.5 per cent. It expected margin expansion in power ancillaries and solar equipment manufacturers to be offset by pressure on product companies due to higher raw material prices and competitive intensity. The brokerage estimated a sharp year-on-year decline in ABB’s margin due to lower pricing power, higher commodity costs and the depreciation of the rupee.

Siemens is expected to see modest margin expansion supported by operating leverage. Cummins is estimated to maintain a healthy margin of about 20.8 per cent, while GE Vernova T&D India’s margin was expected to expand sharply on improved gross margins and operating leverage. Waaree and Premier Energies were expected to sustain strong margins due to backward integration, exposure to the domestic content requirement segment and higher capacity utilisation.

Nomura said project-based companies were likely to see modest margin expansion, with L&T and KEC International benefiting from favourable execution mix and completion of legacy projects. It built in Ebitda and PAT growth of 19.4 per cent and 24.6 per cent year on year for its coverage universe.

The brokerage noted that the Defence Acquisition Council had approved capital acquisition proposals worth about Rs 3,30,000 crore during the first nine months of FY26, nearly double year on year, supporting the medium-term outlook for defence companies.

Nomura added that RBI data continued to indicate the absence of a broad-based private capex recovery, with business confidence indicators remaining subdued and new capex announcements declining year on year. It said tariff-related and other uncertainties had weighed on private investment, although recent GST cuts could support consumption and potentially aid a recovery in industrial capex over the coming quarters.

IMF trims India’s 2026 growth forecast to 6.4%, raises 2027 outlook to 6.7%

IMF trims India’s 2026 growth forecast to 6.4%, raises 2027 outlook to 6.7% Trump warns of fresh strikes on Iran, revives threat to seize Kharg Island as ceasefire unravels

Trump warns of fresh strikes on Iran, revives threat to seize Kharg Island as ceasefire unravels") Cult.fit IPO: 'Alpha' star Hrithik Roshan is a selling shareholder - Check number of shares he will offload

Cult.fit IPO: 'Alpha' star Hrithik Roshan is a selling shareholder - Check number of shares he will offload West Bengal government set to implement Labour Codes

West Bengal government set to implement Labour Codes From $2,950 to $1,200: Why FIFA World Cup 2026 quarter-final tickets suddenly became affordable

From $2,950 to $1,200: Why FIFA World Cup 2026 quarter-final tickets suddenly became affordable RBI Liquidity Outlook: FCNRB Deposits And ECB Measures Could Boost Banking System

RBI Liquidity Outlook: FCNRB Deposits And ECB Measures Could Boost Banking System Growth Or Value Investing? What Could Outperform In India's Market Over The Next 18 Months

Growth Or Value Investing? What Could Outperform In India's Market Over The Next 18 Months Semaglutide Market Enters New Phase; Generics Dominate, Innovators Hold Ground

Semaglutide Market Enters New Phase; Generics Dominate, Innovators Hold Ground Why India Is Challenging The U.S. Tariff Plan At Section 301 Hearings

Why India Is Challenging The U.S. Tariff Plan At Section 301 Hearings Trump Says Iran MoU Is 'Over'; Markets Slide, Crude Oil Surges

Trump Says Iran MoU Is 'Over'; Markets Slide, Crude Oil Surges Jio Financial shares tumble over 5%; here's what analysts are sayingCult.fit IPO: 'Alpha' star Hrithik Roshan is a selling shareholder - Check number of shares he will offload

Jio Financial shares tumble over 5%; here's what analysts are sayingCult.fit IPO: 'Alpha' star Hrithik Roshan is a selling shareholder - Check number of shares he will offload NIIT, Apollo Micro Systems, Tejas Networks shares: Expert decodes trading strategy on BTTV

NIIT, Apollo Micro Systems, Tejas Networks shares: Expert decodes trading strategy on BTTV  Stock market crash: Five biggest reasons behind Sensex, Nifty's 2% slump today

Stock market crash: Five biggest reasons behind Sensex, Nifty's 2% slump today India VIX shoots up 26% as Trump's Iran ceasefire 'over' remark rattles markets; Sensex, Nifty slump over 2%

India VIX shoots up 26% as Trump's Iran ceasefire 'over' remark rattles markets; Sensex, Nifty slump over 2%