Nomura India has downgraded CreditAccess Grameen to 'Reduce' from 'Neutral' due to both growth and asset quality concerns.

Nomura India has downgraded CreditAccess Grameen to 'Reduce' from 'Neutral' due to both growth and asset quality concerns. Nomura India has downgraded CreditAccess Grameen to 'Reduce' from 'Neutral' due to both growth and asset quality concerns.

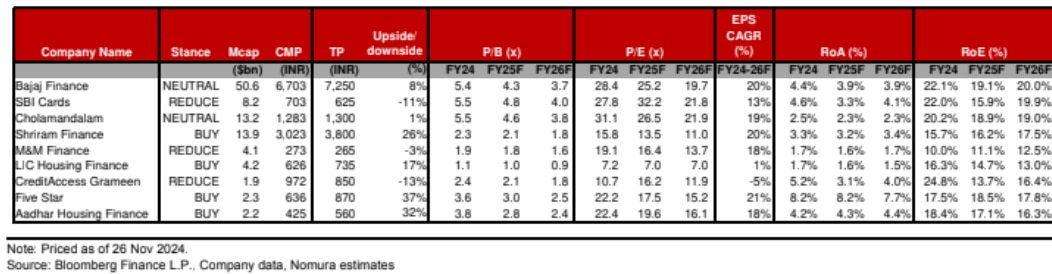

Nomura India has downgraded CreditAccess Grameen to 'Reduce' from 'Neutral' due to both growth and asset quality concerns.Nomura India in its latest note on NBFCs said it has maintained a cautious stance on the sector for FY25 due to asset quality concerns, which in-turn would affect growth levels. Out of nine NBFCs under its coverage, Nomura India said it witnessed a further gradual moderation in YoY asset under management (AUM) growth in Q2FY25 against June quarter. Despite a controlled opex growth, pre-provision operating profit PPOP growth declined, it said adding that asset quality also deteriorated and credit cost inched up.

The brokerage has preference for Shriram Finance, Aadhar Housing and LIC Housing Finance among NBFCs. The FY25 and FY26 Bloomberg consensus EPS estimates have been cut across NBFCs, barring LIC Housing and Shriram Finance, it said while downgrading CreditAccess Grameen to 'Reduce' from 'Neutral' due to both growth and asset quality concerns.

Goldman Sachs has also reportedly downgraded CreditAccess Grameen to 'Sell' from 'Buy; with a target price of Rs 564.

"The past few quarterly results, especially Q225 numbers across the board, have validated most of our arguments around growth, cost of fund and credit costs," Nomura said.

Shriram Housing Finance continues to be its top pick in the sector, given its 15-17 per cent AUM growth, 16-17 per cent RoE franchise. The stock is still trading at benign valuations of 11 times FY26F EPS, it said.

"We also maintain Buy rating on Aadhar (20-21 per cent AUM growth, 17 per cent RoE over FY25/26F, trading at valuations of 2.4 times FY26F BV) and Fivestar (play on secured micro SMEs). We are negative on the remaining names, in the order of SBI Card, Mahindra Finance, CreditAccess Grameen and Neutral on Cholamandalam," it said.

Nomura said credit cost is likely to be higher in FY25 for NBFCs than in FY24, driven by higher delinquencies reported in unsecured personal/ credit cards/ micro finance segments; and ECL/EAD have come down for most players in recent years, from the highs during Covid, and are now at/below pre-Covid levels.

There is limited cushion in terms of impact on P&L if asset quality deteriorates, it said.

Nomura India said the regulator has been cautioning the NBFCs on usurious rates charged by them, especially on unsecured loans (personal loans/ MFI loans) which along-with yield pressure in secured segment due to higher competition, can adversely

impact the yields.

"Furthermore, in case of any repo rate cut in 4Q25F, it would be a positive for CoF/NIMs of NBFCs only in FY26F. Any change in the timeline for repo rate cut would have implications, in our view," it said.

, will establish an integrated compound semiconductor fabrication and assembly facility in Dholera.") Cabinet clears two new semiconductor units in Dholera, Surat, investment tops Rs 3,900 crore

Cabinet clears two new semiconductor units in Dholera, Surat, investment tops Rs 3,900 crore Mamata won't resign after Bengal defeat - what the law allows next

Mamata won't resign after Bengal defeat - what the law allows next Coinbase layoffs: Brian Armstrong says AI is reshaping work, trims 14% workforce

Coinbase layoffs: Brian Armstrong says AI is reshaping work, trims 14% workforce Biocon gets a successor: Why Kiran Mazumdar-Shaw has chosen Claire Mazumdar

Biocon gets a successor: Why Kiran Mazumdar-Shaw has chosen Claire Mazumdar US-Iran war: Govt may have prevented a consumer shock for now but every buffer has a cost

US-Iran war: Govt may have prevented a consumer shock for now but every buffer has a cost Mutual Fund Strategy: Why You Shouldn’t Exit Underperforming Funds Too Soon

Mutual Fund Strategy: Why You Shouldn’t Exit Underperforming Funds Too Soon "Badla Nahi, Badlav!": PM Modi Hails Violence-Free Election As Bengal Enters A New Era Of Peace

"Badla Nahi, Badlav!": PM Modi Hails Violence-Free Election As Bengal Enters A New Era Of Peace India Vs Global Markets: Why Experts Still Prefer Domestic Mutual Funds

India Vs Global Markets: Why Experts Still Prefer Domestic Mutual Funds Tehran Crisis: India Today Reports From Damaged Golestan Palace Amid Protests

Tehran Crisis: India Today Reports From Damaged Golestan Palace Amid Protests Stalin Defeated! The Unbelievable Rise Of Vijay That Has Shaken Indian Politics | TVK

Stalin Defeated! The Unbelievable Rise Of Vijay That Has Shaken Indian Politics | TVK CreditAccess, Titagarh Rail, Quess Corp shares surge up to 17%; check targets, stop-loss levels and outlook

CreditAccess, Titagarh Rail, Quess Corp shares surge up to 17%; check targets, stop-loss levels and outlook Rupee closes at all-time low on renewed US-Iran tensions; analysts see more downside

Rupee closes at all-time low on renewed US-Iran tensions; analysts see more downside  Jio Financial, Inox Wind, Indus Towers: How to trade these stocks? Expert strategy | Daily Calls on BTTV

Jio Financial, Inox Wind, Indus Towers: How to trade these stocks? Expert strategy | Daily Calls on BTTV Kissht IPO subscribed 9.5 times on final day of bidding; GMP rises

Kissht IPO subscribed 9.5 times on final day of bidding; GMP rises L&T Q4 FY26 results: Profit slips 3% to Rs 5,326 crore; announces final dividend, sets record date

L&T Q4 FY26 results: Profit slips 3% to Rs 5,326 crore; announces final dividend, sets record date