Vedanta, Hindustan zinc, Tata Steel, Jindal Steel, JSW Steel, SAIL share price targets.

Vedanta, Hindustan zinc, Tata Steel, Jindal Steel, JSW Steel, SAIL share price targets.The Indian metals and mining sector is poised for a quarter of diverging fortunes, where strong volume growth is expected to lock horns with mixed pricing power. Brokerage Systematix Institutional Equities anticipates a ‘strong set of numbers’ for the third quarter of FY26, driven primarily by post-monsoon demand recovery.

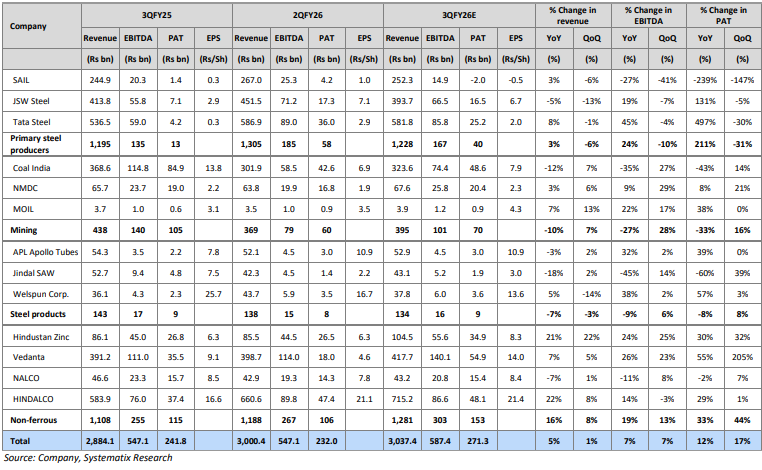

While the aggregate coverage universe is estimated to post a 10 per cent year-on-year (YoY) growth in profit after tax (PAT), the brokerage noted that the heavy lifting will likely be done by non-ferrous majors and select steel tube manufacturers.

According to Systematix, non-ferrous companies are leading the pack, aided significantly by a global surge in commodity prices. The quarter witnessed an uptick in base and precious metal prices, fueled by supply disruptions and geopolitical uncertainties.

Systematix highlighted that Vedanta and Hindustan Zinc are on track to witness margin expansion and higher profitability. However, Hindalco might see its growth moderated; the brokerage points out that the impact of fire at Novelis NY plant would spill over in 3QFY26, dampening the benefits of commodity price tailwinds.

National Aluminium Co (NALCO), on the other hand, may experience weaker comparative growth due to its high base from the prior year.

JSW Steel and Tata Steel are expected to outperform. The brokerage attributed this resilience to a superior sales mix, cost control measures, operational efficiency, and a steady growth in volumes.

Steel Authority of India (SAIL) appears to be on a slippery slope. The PSU major is positioned for a fall in profitability attributed to the dip in steel prices and the absence of any notable capacity expansion led volume growth, it said.

In the steel tubes segment, Welspun Corp is projected to be the ‘top performer’ with a staggering 38 per cent YoY EBITDA growth, supported by diversified operations, Systematix said. APL Apollo Tubes follows with a projected 32 per cent growth.

NMDC and MOIL are tipped to outperform due to a sharp rise in volumes. On the other end of the spectrum, Coal India continues to face headwinds. Systematix remarked that the coal behemoth continues to lag mining peers with a consistently declining offtake and a bleak growth outlook.

Q3 Targets and Ratings

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K crore

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K crore 'You're in the wrong chair': When Gita Gopinath faced bias as IMF chief economist

'You're in the wrong chair': When Gita Gopinath faced bias as IMF chief economist Can India monetise microdramas as the market booms but profitability remains elusive?

Can India monetise microdramas as the market booms but profitability remains elusive? India needs its own DeepSeek to avoid AI dependence, warns Bernstein

India needs its own DeepSeek to avoid AI dependence, warns Bernstein.") Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match

HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recoveryInfosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K croreLast chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recoveryInfosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K croreLast chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure

Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure  JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential

JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential