Buying stocks that can rise multifold in a short period is every investor's dream. But it is not easy to spot such stocks. Of all the companies listed on the Bombay Stock Exchange, only 13 have given positive returns in all years since 2004 (except for 2008, the year of the global financial crisis).

However, the key question is whether these 'Fabulous 13' be able to sustain this run ? Can their past performance be used to predict their future growth?

We analyse these companies to find out why their stocks have been so buoyant and that too for such a long period. Here is a snapshot of each along with a SWOT (strength, weakness, opportunities and threat) analysis.

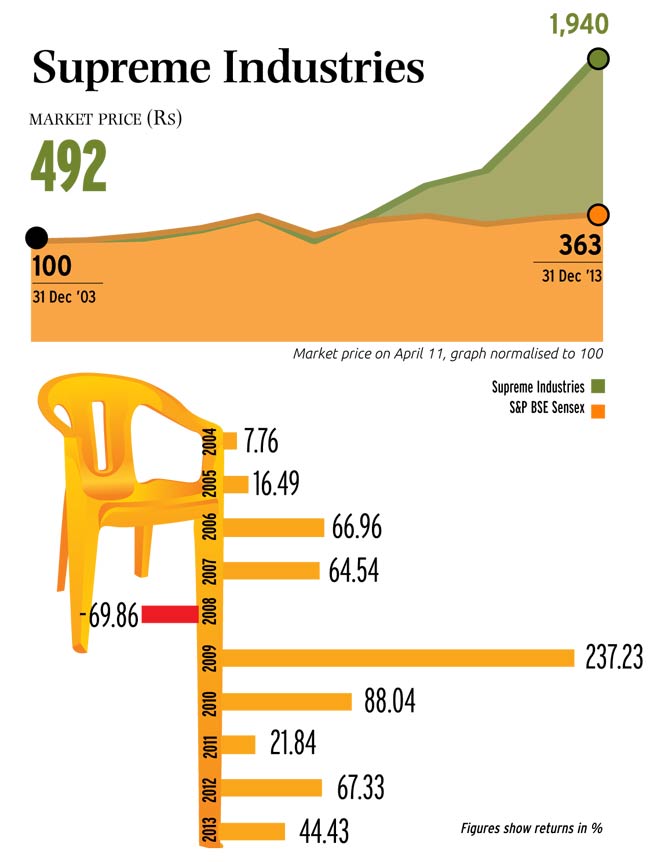

SUPREME INDUSTRIES

The company is one of India's largest plastic processors. It has been growing at a fast pace for the past 10 years due to steady rise in the proportion of value-added products in the portfolio and expansion of the distribution and production network (it has 2,000 channel partners). The operating profit margin of value-added products is more than 17%.

The stock has risen 19 times between 31 December 2003 (Rs 21.92) and 31 December 2013 (Rs 425.35).

"Supreme Industries' decision to move from commoditised products (which can be easily produced) to technologically-advanced products has contributed to its outstanding performance over the years," says Jaipal Shetty, research analyst, Maximus Securities.

Supreme has been increasing net profit at the rate of 22.8% a year on an average for the past five years. It reported a net profit of Rs 272 crore for the year ended June 2013 as against Rs 97.39 crore for the year ended June 2009. The return on equity, or RoE, rose from 9.40% in 2003 to 37.79% in 2013. The strong balance sheet had Rs 22.76 crore cash in hand and bank in June 2013. The company, say experts, looks like a good bet considering its history of efficient capital allocation, excellent distribution network, good brand recall, decent record of developing products and an innovative product line-up.

"We feel the company will be able to at the very least maintain its current growth rate for the next five years provided oil prices do not rise much and India's economy recovers," says Shetty.

On March 31, the stock was at Rs 499 with trailing 12 months price-toearnings, or PE, ratio of 22.52 compared to the industry average of 14.98. The stock has risen 43% since October 2013 in spite of the company reporting weak numbers in the second quarter. The management has cut revenue growth guidance for the financial year from 22% to 20-22% and volume growth guidance from 12% to 9-10% because of weak demand. "But the stock is trading at a slightly high PE multiple," warns Shetty.

CRISIL

CRISIL has been giving huge returns to investors for the past 10 years primarily due to its robust business model. It has been able to successfully diversify into the non-rating business with a series of acquisitions.

CRISIL's RoE has almost doubled from 20% to 40% in the past ten years. Moreover, it has been paying good dividends. Growth in revenue and net profit has been consistently high.

The stock rose 2,090% between 31 December 2003 (Rs 55) and 31 December 2013 (Rs 1,207). In 2008, it had fallen 32.9%. "Share buyback, high dividend payouts, inorganic growth, robust business model, backing of a foreign parent and high return ratios have been driving the stock for the last 10 years," says Silky Jain, research analyst, Nirmal Bang Securities.

Operating profit rose 32% a year on an average between 2005 and 2013. Net profit was Rs 312.57 crore in the year ended December 2013 as against Rs 32.41 crore in the year ended December 2005. Jain expects healthy revenue and net profit growth to continue.

"One can remain remain invested in this market leader. With recovery in the economic environment, the expansion of the sector will lead to faster growth and better returns." On March 31, the stock was at Rs 1,229.30, with a PE ratio of 30.89 as against the industry figure of 26.72.

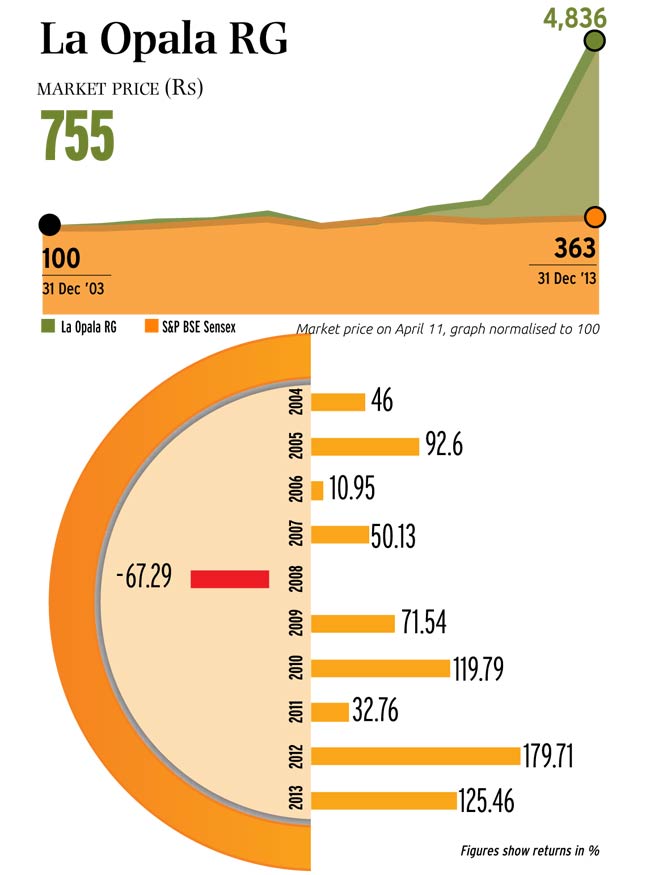

LA OPALA RG

La Opala was set up in 1988. In 1999, Radha Glass and La Opala merged to become La Opala RG. The company makes glass and glass products. It exports 85% of its crystal ware production.

La Opala RG has 125 distributors and 10,000 dealers.

Gokul Raj, executive director and head of investments, HBJ Capital, says La Opala has been the beneficiary of the rise in aspirational spending by Indians over the last decade. The stock returned 47.7% a year on an average between 2003 and 2013.

Factors driving growth are urbanisation, rising demand for branded kitchenware and increasing competitiveness of Indian products against imports from China.

"The exceptional returns of the past decade are a function of strong earnings growth and valuation re-rating," says Gokul Raj.

While revenues have been growing at 16% a year, operating profits have been rising at 32% a year. The latter is due to high margins and capacity utilisation (fixed asset turnover has improved from 1.7 times to over 2.6 times over the last decade).

Gokul Raj expects 15-20% annual revenue and profit growth over the next five years. The reasons are higher utilisation of the recentlyexpanded capacity and rise in exports.

The stock has undergone a sharp re-rating, especially over the last three years, due to improvement in the quality of growth. The Ebitda to capital employed ratio has shot up from 15% to 50% over the last five years. Ebitda, or operating profit, is earnings before interest, tax, depreciation and amortisation. "Leaders of niche consumption segments that have been able to grow fast over the past five years have been re-rated. This has helped La Opala to also deliver fantastic returns," says Gokul Raj.

On March 31, the stock was at Rs 708.50 with a PE ratio of 27.05. It is expensive as the industry PE is just 16.50. Gokul Raj is not positive on the stock. "The current valuation of 10 times the book value and more than 26 times forward PE is high and factors in all the positives. Valuation re-rating is not likely and hence our base case scenario is 15% rise in the stock price. While earnings growth of 15-20% can continue to push up the stock, the risk of negative earnings surprises has increased due to moderation in consumption growth. In view of the sharp rise over the last five years and expected earnings, we believe that the risk-reward equation is not favourable for investing in the stock at current levels."

CERA SANITARYWARE

Consumer spending in India has been rising at a scorching pace over the last 10 years. This is reflected in the top line and operating performance of Cera Sanitaryware. Net profit has been rising by 40% a year and stock by 54.5% a year on an average for the last 10 years (it rose from Rs 9.1 on 31 December 2003 to Rs 701.50 on 31 December 2013).

Twinkle Gosar, equity research associate, mid-caps, Angel Broking, says, "Growth in consumer demand encouraged Cera to expand its sanitary ware division in 2006-07. We expect top line and profit growth of 25% and 15%, respectively, a year in the coming four-five years."

Operating performance has been stable (margins above 17%) while top line has been growing above 40% a year on an average for the last five years.

The stock has risen 283% in the past two years; it was at Rs 890.70 on March 31 (PE ratio of 24.24). "Despite expectation of robust performance, the company is expected to deliver an annual return of 15% for the next five years. The stock has risen sharply in the past two-three years," says Gosar.

BOSCH

Bosch is a leading supplier of technology and services in the areas of automotive/industrial technology, consumer goods and building technology. Its stock has been rising by 20% a year on an average for the last 10 years. It was at Rs 10,087 on 31 December 2013.

Bosch, a global leader in diesel fuel injection technology, commands 80% share of the domestic diesel systems market. In this it has been helped by fast growth in demand for tractors and commercial vehicles and introduction of the anti-lock braking technology in 2010. Other factors are pricing power in fuel injection systems and spark plugs, rising demand for diesel vehicles (55% sales in 2012-13), wide product portfolio which insulates the company from cyclical factors and long relationship with major original equipment makers. Also, the non-auto business grew 20% a year between 2011 and 2013.

Bosch recently launched the energy solutions business, which signals intent to expand the non-auto business.

The company has been increasing revenue and net profit at the rate of 14.25% and 13% a year, respectively, on an average for the past eight years. Experts say such high growth is likely to continue due to revival in commercial vehicle and tractor segments, demand for diesel engines due to low price of the fuel, traction in the non-auto business and implementation of new emission norms in 2015.

Cholamandalam Securities says revenue will grow 14% a year and net profit 16% a year between 2013 and 2018 due to higher localisation and favourable product mix.

On April 1, the stock was trading at Rs 10,858, with PE ratio of 38.20 as against the industry PE of 21.72. Cholamandalam says Bosch is trading at a premium of 50-60% to other auto ancillary companies. The high valuation, it says, is justified given the company's access to expertise of parent, leadership in diesel fuel injection technology, high return ratios and ability to maintain growth even in tough times. The stock can give 15% a year return in the next five years.

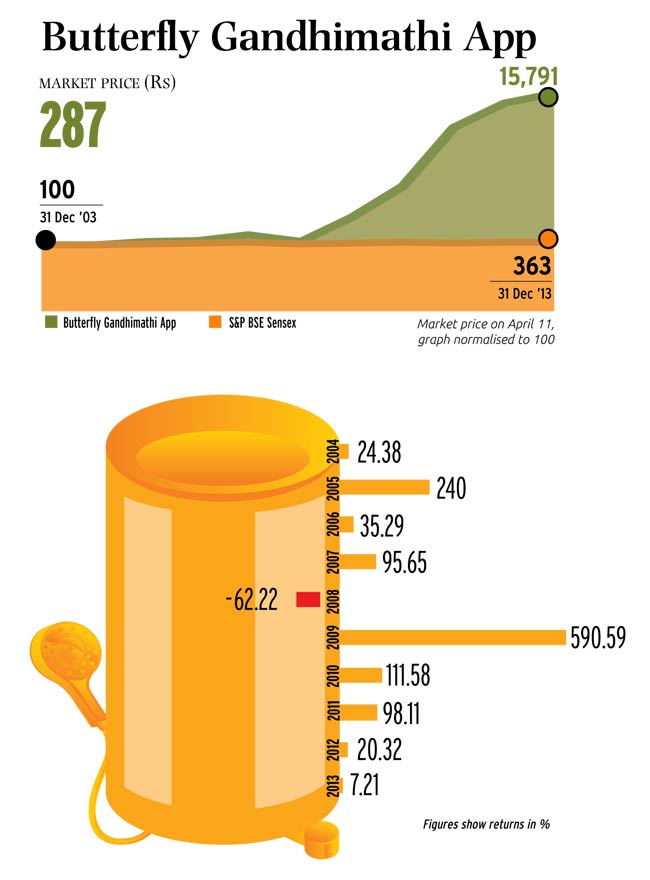

BUTTERFLY GANDHIMATHI APPLIANCES

The maker of home appliances was the first in India to introduce stainless steel pressure cookers and vacuum flasks. Product range includes LPG stoves & mixer grinders. The stock has returned 65.9% a year on an average in the last 10 years.

The company, which was referred to the Board for Industrial and Financial Reconstruction due to financial troubles, has managed to increase operating profit margin from 4.6% in 2005-06 to 9.5% in 2012-13 and reduce the debt-to-equity ratio from 2.1 in 2007-08 to 0.2 in 2012-13. It plans to become debt-free over the next two to three years. In March 2012, Reliance Alternative Investments Fund picked up a 13.7% stake in the company for Rs 100 crore.

The top line has grown 57.62 a year on an average for the last eight years; it was Rs 807 crore in the year ended March 2013. Net profit was Rs 33.42 crore in the year ended March 2013 as against a loss of Rs 3.36 crore in the year ended March 2005.

"We expect branded sales to grow at 15-20% per annum for the next five years. The company is hopeful of expanding margins as its turnover crosses Rs 1,000 crore. However, we expect flat margins in the near term due to rise in promotional expenses in non-south markets," says Dhvani Bavishi, analyst, ICICIdirect.com.

Bavishi is bullish on the stock. "Due to stable top-line growth, we expect a 15-20% price rise over the next 12-18 months." On April 1, the stock was at Rs 293.80.

BATA INDIA

The stock has given a return of 33% a year on an average for the past 10 years. One reason is the massive restructuring at the company, including halving of the head count, which has led to fast growth in profitability.

Bata India has saved a lot in employee cost in the past few years, says Gaurang Kakkad, vice president, institutional research, Religare Capital Markets. "The cost, around 20% of sales in 2004-05, is now 10% of sales Almost 10% margins are on account of savings under this head. Shift to premium products has also helped," he says.

The company reported an operating profit margin of 17.10% for the year ended December 2013 as against 4.71% in the year ended December 2005. Net profit grew from Rs 12.49 crore to Rs 190.74 crore during the period.

Kakkad is positive on the stock. "We expect 17-18% growth in revenue and 20% in profit per year over the next five years. One can expect 15-18% return from the stock in the next 12-18 months." On April 1, it was at Rs 1,131.

AMARA RAJA BATTERIES

Amara Raja is among the pioneers of maintenance-free batteries in India, something that has catapulted it to the second position in the Indian automotive battery market in a short period. The company continues to be a leader in introduction of new technologies in the automotive and industrial battery space. One of its biggest strengths is the technology tie-up with global battery maker Johnson Controls, which owns 26% equity in the company.

The stock has risen 48% a year on an average between 2003 and 2013. "One reason for such spectacular growth has been the shift in demand towards branded batteries. Other reasons could be rapid increase in market share in automotive and industrial segments. The company has managed to retain margins even as its increased sales rapidly due to the strength of its product mix," says Vikram Dhawan, director, Equentis Capital.

In the past 10 years, net profit and sales have been rising 44% and 33%, respectively, a year on an average. Net sales and net profit were Rs 2,961 crore and Rs 286.7 crore, respectively, in the year ended March 2013.

"We expect profit and revenue growth of 20-25% a year for the next five years. The stock is likely to be a clear outperformer in the next few years. One can expect 15-20% annual returns in the next two-three years on the back of earnings per share growth, healthy operating margins and improvement in the country's economy," says Dhawan.

On April 1, Amara Raja was trading at Rs 386, a PE ratio of 19.

GOODYEAR INDIA

The company's financials have been improving for the last ten years. Ten years ago, it had huge debt and was making losses. Now, the debt is zero while profits are soaring. One trend that has helped Goodyear is growth of the automobile industry, more specifically tractor and passenger car segments, its main focus (98% offtake).

New products and launch of a retail outlet are the other factors that have helped the company report decent growth.

The stock has returned 22% a year on an average in the last 10 years. Vijay Dave, senior research analyst, Sunidhi Securities, says, "The stock is attracting investors due to improvement in the company's fundamentals, high dividend payouts, fall in rubber prices and the company's MNC status."

In the last five years, revenue and net profit have grown at a compounded annual growth rate of 11% and 24%, respectively. DK Aggarwal, chairman and managing director, SMC Investments and Advisors, says, "In 2013, the performance improved significantly due to higher margins on account of favourable rubber prices. As the economic situation improves, revenue and profit growth are expected to rise further."

At Rs 418.45, the stock is trading at a PE of 10.26, close to its five-year average of 9.52. Thus, it is fairly priced. "Falling rubber prices, rising incomes in rural areas and topping out of interest rates will benefit the company. One can expect 15-20% annualised return in the future too," says Aggarwal. An Angel Broking report in March 2014 said the stock could hit Rs 472 in the next 12 months.

SUN PHARMACEUTICAL INDUSTRIES

The stock rose 34.3% a year on an average between 2003 and 2013.

Edelweiss Financial Services says high growth in earnings per share and stock price has been due to various acquisitions and leadership in the chronic ailment space.

Net sales and profit have been growing at 10% every year since 2003. Edelweiss expects 20% growth every year for the next three years. The stock is trading at a premium to peers, mainly due to higher return ratios and margins. Analysts expect rise in competition for some of Sun's most profitable brands. This, they say, will make it difficult for the company to sustain returns.

On April 1, the stock was trading at Rs 573.35.

Sun recently entered into an agreement to acquire 100 % of Ranbaxy in an all-stock transaction. Ranbaxy shareholders will receive 0.8 share of Sun Pharma for each share of Ranbaxy. The exchange ratio represents an implied value of Rs 457 for each share of Ranbaxy. The combination of Sun Pharma and Ranbaxy will create the fifthlargest specialty generics company in the world and the largest pharmaceutical company in India.

Rahul Sharma, analyst, Karvy Stock Broking, says, "The deal could be accretive in the long run as Sun Pharma has a track record of turning around acquired companies. We cut our earnings per share estimates by 5% to Rs 30.4 for 2015-16. We roll over our price target to 2015-16 from December 15. We reduce our price target by 5% to Rs 684 based on 22.5 times 2015-16 earnings."

TTK PRESTIGE

Consumer durables industry does well during periods of high economic growth. This is more so in an emerging market like India where ownwership of white and grey goods is low. During the boom years of 2004-11, thanks to exploding discretionary incomes, the industry did spectacularly well.

TTK Prestige reported a remarkable spurt in sales from Rs 339 crore in 2007-08 to Rs 1,385 crore in 2012-13. The net profit rose from Rs 20.67 crore to Rs 133.09 crore during this period. Earnings per share zoomed from Rs 17.64 to Rs 114.29, pushing the stock to dizzy heights.

VK Vijayakumar, investment strategist, Geojit BNP Paribas Financial Services, says, "The explosive growth in top line and bottom line was reflected in the stock price. The market rewarded the performance by a higher PE ratio."

TTK Prestige has returned 70.5% a year in the last 10 years. "It will be unrealistic to expect such returns in the immediate future. Investors should temper expectation to a more reasonable 25% in the next five years," says Vijayakumar.

ITC

Stock markets were under a lot of pressure in the last few years. That's why investors took refuge in defensive sectors, the ones that are not as prone to slowdown as others. One such sector was fast moving consumer goods. That's the biggest reason for the 25.5% a year return given by the ITC stock in the past ten years.

Sudip Bandyopadhyay, president, Destimoney Securities, says, "Tobacco business is a cash cow for ITC. It is also recessionproof. It helped the company report fast earning growth during the period. I expect 15% revenue and 8-10% net profit growth every year for the next five years."

Sales rose from Rs 5,865 crore in 2003 to Rs 41,810 crore in 2013. Net profit rose from Rs 1,371 crore Rs 7,418 crore. On April 2, the stock was trading at Rs 344.25, with a PE ratio of 32.46 as against the industry average of 31.93.

"At present, ITC is reasonably valued and one can expect 10-15% annualised return for the next five years."

SHRENUJ & COMPANY

The company makes polished diamond and jewellery products. The market capitalisation is Rs 900 crore.

The stock has returned 25.6% a year on an average in the past 10 years. It was at Rs 99.6 on 31 December 2013 as against Rs 10.20 on 31 December 2003.

Nikhil Kamath, director, Zerodha, says, "A bullish diamond market is the biggest reason for Shrenuj's stellar performance. We expect revenues to grow by 10% annually. The stock looks fairly valued at current levels with PE of three. We can expect annualised returns of 15% for next five years. However, the stock is a fairly illiquid, and so entering and exiting will be fairly convoluted." On April 2, Shrenuj and Company was trading at Rs 93.70.