According to the RBI’s December monthly bulletin, small savings schemes excluding the Public Provident Fund (PPF) saw inflows shrink by nearly 24%.

According to the RBI’s December monthly bulletin, small savings schemes excluding the Public Provident Fund (PPF) saw inflows shrink by nearly 24%.Indian households are steadily redrawing their savings playbook as lower interest rates erode the appeal of traditional fixed-income products. Latest data from the Reserve Bank of India (RBI) shows that in FY25, savers pulled back from bank deposits, insurance and small savings schemes, while channelling a growing share of their money into equities and mutual funds.

This reallocation gathered pace as banks and small finance banks cut fixed deposit (FD) rates repeatedly through 2025, following a series of repo rate reductions by the RBI. The central bank lowered the policy rate by a cumulative 125 basis points during the year, squeezing returns on deposits and prompting households to seek higher-yielding investment avenues.

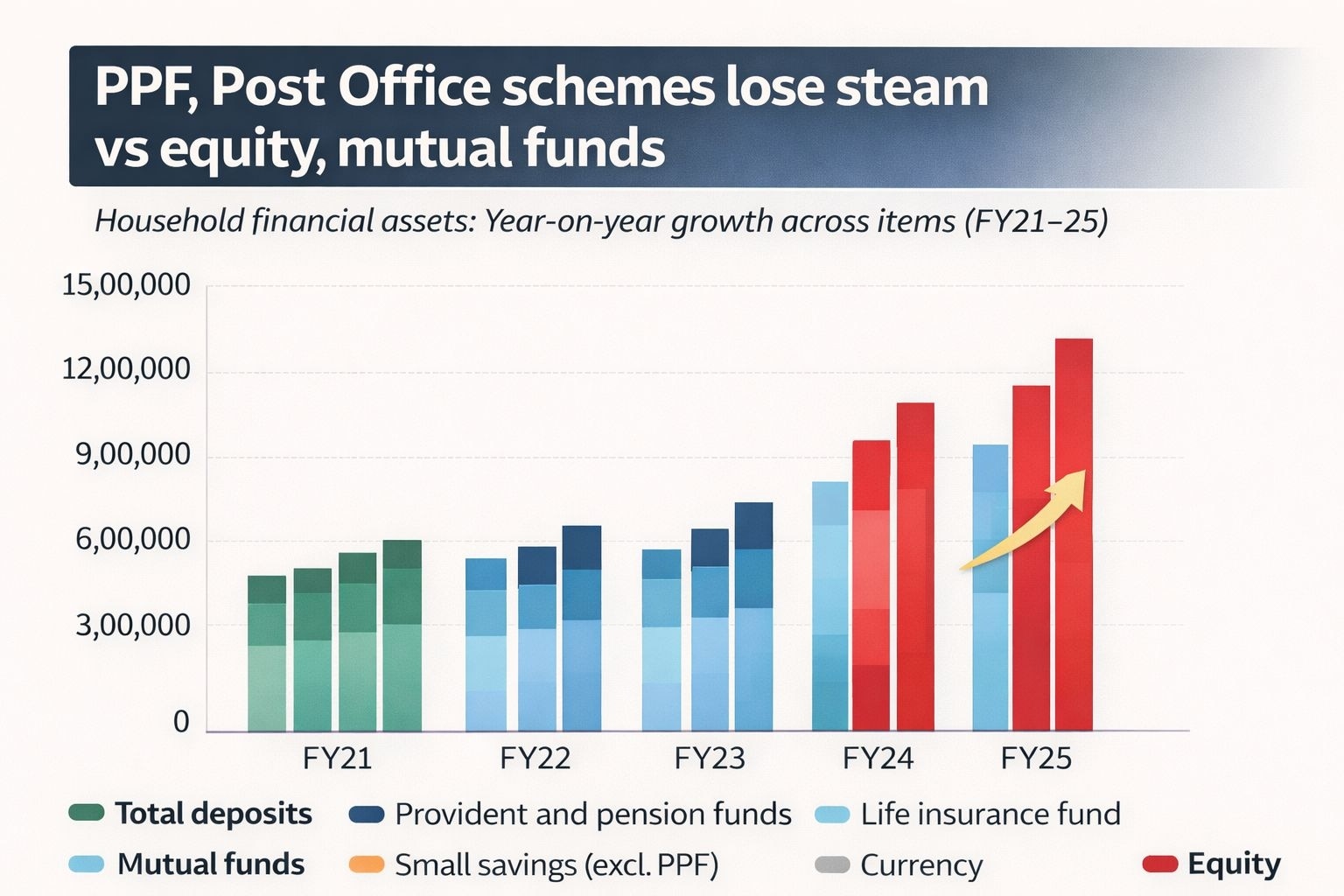

According to the RBI’s December monthly bulletin, household bank deposits declined 8.97% in FY25 to Rs 12.54 lakh crore, reversing the expansion seen in the previous two years. Investments in life insurance funds dropped even more sharply, falling 17.3% to Rs 5.3 lakh crore, while small savings schemes excluding the Public Provident Fund (PPF) saw inflows shrink by nearly 24%. Together, these figures point to waning appetite for low-risk, low-return instruments.

At the same time, households moved decisively towards higher-yielding, market-linked assets. Direct equity investments surged about 153% during the year, while mutual fund inflows jumped 95%. Currency holdings also rose sharply by 77.6%, suggesting a mix of higher liquidity preference and increased consumption.

The shift is visible not just in annual flows, but also in the composition of household financial assets over time. Bank deposits, while still the single largest component, saw their share of total household financial savings fall from 40.9% in FY21 to 35.2% in FY25. In contrast, mutual funds expanded their share dramatically -- from just 2.1% to 13.1% over the same period. Direct equity holdings, though smaller in absolute terms, also increased their share from 1.3% to 2.1%.

RBI data from FY21 to FY25 points to a steady and structural change in savings behaviour. Deposits continue to dominate, but their growth has become volatile, particularly after a sharp contraction in FY22, indicating they are no longer the default destination for incremental savings. Provident and pension funds, however, have shown consistent year-on-year growth, supported by mandatory contributions, formal employment and a long-term focus on retirement security.

Life insurance funds have grown more slowly, reinforcing their role as protection-oriented products rather than return-seeking investments. The standout trend remains the surge in mutual fund investments, especially from FY23 onwards, driven by robust equity market performance, widespread adoption of systematic investment plans (SIPs) and rising financial awareness among retail investors.

Small savings schemes

Despite the broader move towards market-linked assets, the government has kept interest rates on small savings schemes unchanged for the January–March quarter of FY26. Rates on instruments such as PPF (7.1%), Senior Citizen Savings Scheme and Sukanya Samriddhi Yojana (both 8.2%), National Savings Certificate (7.7%) and Kisan Vikas Patra (7.5%) have been left untouched for the seventh consecutive quarter. The Ministry of Finance last revised rates in the fourth quarter of FY24.

Post Office savings deposits will continue to earn 4%, while time deposits will offer between 6.9% and 7.5%, depending on tenure. The Monthly Income Scheme will pay 7.4% annually.

Instrument Interest rate from January 1, 2026 to March 2026 (%)

Savings Deposit 4%

1 Year Time Deposit 6.9%

2 Year Time Deposit 7%

3 Year Time Deposit 7.1%

5 Year Time Deposit 7.5%

5 Year Recurring Deposit 6.7%

Senior Citizen Savings Scheme 8.2%

Monthly Income Account Scheme 7.4%

National Savings Certificate 7.7%

Public Provident Fund Scheme 7.1%

Kisan Vikas Patra 7.5% (Matures in 115 months)

Sukanya Samriddhi Account 8.2%

Cancer is leaving more children without mothers; India among six hardest-hit countries, says WHO

Cancer is leaving more children without mothers; India among six hardest-hit countries, says WHO RAM shortage declines global PC shipments down to 4.9%, Apple gains market share

RAM shortage declines global PC shipments down to 4.9%, Apple gains market share TCS Q1 results: Net profit rises to ₹13,349 crore, revenue up 14% | Quarterly earnings details

TCS Q1 results: Net profit rises to ₹13,349 crore, revenue up 14% | Quarterly earnings details NCR real estate market underperforms; sales decline 7% in first half of 2026

NCR real estate market underperforms; sales decline 7% in first half of 2026 Nissan Tekton launched in India at ₹10.49 lakh; check variants, key features

Nissan Tekton launched in India at ₹10.49 lakh; check variants, key features Markets Recover Amid Global Uncertainty: Jyotivardhan Jaipuria Explains Why

Markets Recover Amid Global Uncertainty: Jyotivardhan Jaipuria Explains Why Trump's Iran Warning Sparks Oil Rally | What's Next For Crude, Petrol, Diesel & LPG?

Trump's Iran Warning Sparks Oil Rally | What's Next For Crude, Petrol, Diesel & LPG? LIVE What’s Hot: Stocks, Gold & Big Money Moves | Daily Markets Show | July 09 | Business Today TV

LIVE What’s Hot: Stocks, Gold & Big Money Moves | Daily Markets Show | July 09 | Business Today TV Nitin Gadkari Responds To Ethanol Row: Are Ethanol Fuel Blends Really Damaging Your Car?

Nitin Gadkari Responds To Ethanol Row: Are Ethanol Fuel Blends Really Damaging Your Car? India Hosts Half Of World's GCCs, Emerges As Global Enterprise AI Talent Hub: CEA Nageswaran

India Hosts Half Of World's GCCs, Emerges As Global Enterprise AI Talent Hub: CEA Nageswaran Sensex, Nifty trim gains but settle higher; what's next for the market?

Sensex, Nifty trim gains but settle higher; what's next for the market? Adani Enterprises shares gain as group forays into low-carbon chemical production

Adani Enterprises shares gain as group forays into low-carbon chemical production  Kalyan Jewellers shares zoom 25% in two days; is more steam left?TCS Q1 results: Net profit rises to ₹13,349 crore, revenue up 14% | Quarterly earnings details

Kalyan Jewellers shares zoom 25% in two days; is more steam left?TCS Q1 results: Net profit rises to ₹13,349 crore, revenue up 14% | Quarterly earnings details TCS Q1 FY27 results: Rs 12 per share interim dividend announced; check record date

TCS Q1 FY27 results: Rs 12 per share interim dividend announced; check record date