Improving GDP growth should continue to support PLFs, the report added.Improving GDP growth should continue to support PLFs, the report added.

Improving GDP growth should continue to support PLFs, the report added.Improving GDP growth should continue to support PLFs, the report added.The earnings outlook for Indian and South-east Asian airline sector should improve in 2016, driven by higher demand, lower fuel costs and ongoing industry restructuring, according to a report by Fitch Ratings. However, the operating environment is expected to be challenging due to strong competition and capacity expansion.

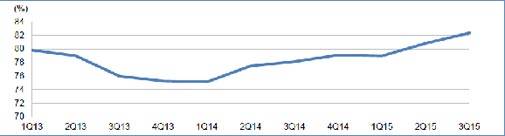

Passenger load factors (PLF) in India and South-east Asia have risen steadily, with the average PLF across seven major airlines based in the region hitting multi-year highs above 80 per cent in Q3 of 2015 (calendar year).

Improving GDP growth should continue to support PLFs, the report added. Revenue passenger-kilometre growth topped 19 per cent year-on-year in India over the first 10 months of 2015, above 12.4 per cent in China, 8.5 per cent in Russia and 2.3 per cent in Brazil. Air travel demand in South-east Asia was supported by a robust increase in tourist arrivals in countries including Thailand and Philippines, which had double-digit growth in the first nine months of 2015.

The continued decline in global oil prices is also expected to provide a much-needed boost to airline earnings, with Brent crude falling further so far in Q4 of 2015.

Jet fuel costs comprise around 50 per cent of airline operating costs and EBITDA has been rising steadily as oil prices have fallen.

According to the report, "currency weakness throughout the region will partially offset the benefits of the falling oil price, which is denominated in US dollars. But oil prices have declined significantly even in local-currency terms. Airlines will be reluctant to cut capacity or exit routes and therefore any sustainable profit improvement resulting from low fuel prices could be delayed."

Industry consolidation and restructuring should also start to result in improved profitability. Many airlines hit by overcapacity and a weaker economy in recent years have sought to delay aircraft deliveries, cut loss-making routes, improve utilisation and consolidate operations.

Low-cost carriers' capacity in South-east Asia grew 9 per cent in 2015, compared to 14 per cent in 2014 and 30 per cent in 2013. Philippines' carriers have gained improved yields and load factors from consolidation in the domestic market that halved the number of domestic carriers to three. India's SpiceJet has also achieved a remarkable turnaround over the past year, turning profitable from the verge of bankruptcy by focusing on profitable routes.

Aggressive competition and capacity expansion, however, remain key risks for the sector, especially over the longer term. Capacity growth in South-east Asia and India has slowed in 2015 as airlines focused on profitability. But a huge order book for new aircraft remains, which could make it difficult to improve profitability for the sector.

Another factor driving capacity growth is the attraction of larger and higher-density narrow-body aircraft in the face of infrastructure constraints at some airports. Growth in fleets and increase in average aircraft size could have a significant impact on capacity outpacing demand, the report says.

Competitive threats could yet put pressure on margins even as passenger growth remains robust. In India, capacity growth risk stems from new entrants such as AirAsia India and Vistara trying to gain a foothold in a growing market, with incumbents such as IndiGo and SpiceJet trying to retain their share of a growing market by expanding their fleet size.

NSE IPO may unlock mega gains for billionaire investors RK Damani, Premji

NSE IPO may unlock mega gains for billionaire investors RK Damani, Premji 'The real sting is the monitoring': Brahma Chellaney flags risk for India in Trump's Russian oil order

'The real sting is the monitoring': Brahma Chellaney flags risk for India in Trump's Russian oil order Moltbook hype unravels: Viral posts were human-written, not AI, finds MIT Technology Review

Moltbook hype unravels: Viral posts were human-written, not AI, finds MIT Technology Review is signed.") India-US BTA: Harley Davidson bikes to get 0% duty, gradual tariff reduction on luxury cars

India-US BTA: Harley Davidson bikes to get 0% duty, gradual tariff reduction on luxury cars India-US interim trade agreement: 'No GM modified product allowed, agri sector protected,' says Piyush Goyal

India-US interim trade agreement: 'No GM modified product allowed, agri sector protected,' says Piyush Goyal BT Golf 2025-26 Kochi, Kerala Awards Ceremony Marks A High-Energy, Successful Conclusion

BT Golf 2025-26 Kochi, Kerala Awards Ceremony Marks A High-Energy, Successful Conclusion Golf Is An Addiction. We Eat And Sleep Golf!

Golf Is An Addiction. We Eat And Sleep Golf! The Fairway Fixes Everything. Mindset, Life, Relationships

The Fairway Fixes Everything. Mindset, Life, Relationships BT Golf LIVE: Join AU Small Finance Bank Presents BT Golf 2025-26 For Its 4th Leg In Kochi, Kerala

BT Golf LIVE: Join AU Small Finance Bank Presents BT Golf 2025-26 For Its 4th Leg In Kochi, Kerala AI Will Change MBAs, Not Leadership: IMD President On India’s Global Education Rise

AI Will Change MBAs, Not Leadership: IMD President On India’s Global Education Rise RIL, SBI, Kotak Bank, Kalyan, HAL, BEML, BDL among stocks in focus next week; here’s whyNSE IPO may unlock mega gains for billionaire investors RK Damani, Premji

RIL, SBI, Kotak Bank, Kalyan, HAL, BEML, BDL among stocks in focus next week; here’s whyNSE IPO may unlock mega gains for billionaire investors RK Damani, Premji SBI Q3 Results: Profit jumps 24% to Rs 21,028 crore; asset quality improves

SBI Q3 Results: Profit jumps 24% to Rs 21,028 crore; asset quality improves IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’

IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’ BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week

BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week