Ajay Piramal, Chairman of the Piramal group, has been through several avatars. There was the passionate businessman, when he - along with wife Swati - acquired Nicholas Laboratories and built it bit by bit through acquisitions and organic growth as Piramal Healthcare, India's third largest domestic pharma firm; the dispassionate businessman when he sold Piramal Healthcare's flagship formulations business to US pharma major Abbott for $3.8 billion (Rs 18,000 crore then); the White Knight when he became Vodafone's India investor alongside Max group's Analjit Singh when it needed at least 26 per cent equity to be held by Indians; even the start-up man when he floated Piramal Realty in 2012 and a few weeks ago, invested in Aircel's C. Sivasankaran's start-up cab aggregator Utoo.

But nothing sticks in public memory more than his most recent avatar - Ajay Piramal, the investor. The risk taker. Alike Warren Buffett. The contrarian, who is placing big bets on businesses ranging from financial services to healthcare on one hand, and drug discovery and realty on the other. He even bid for Lafarge's cement business in India before losing out to Nirma. "We are planning to enter one more business sector in India and let's see how it pans out. I have not set any targets or timeframe for it," Piramal told BT. Over the years, India has seen several investors/ financiers/ arbitrageurs, starting with Sivasankaran himself. Max group's Singh has been through several investment cycles. And his nephews Malvinder and Shivinder also invested heavily in healthcare before pulling back. But nobody has reached the scale at which Ajay Piramal operates.

"I have not come across any parallels like Ajay Piramal in family businesses, though there are many entrepreneurs who have moved out and built their own businesses," says Kavil Ramachandran, Executive Director, Thomas Schmidheiny Centre for Family Enterprise, Indian School of Business (ISB). "His primary intention is to create wealth by aggressively acquiring or identifying niche business areas, investing in them, and selling off for a big value."

From the sale proceeds and earnings thereafter, he first bought an 11 per cent stake in Vodafone India for Rs 5,863 crore in two tranches in August 2011 and February 2012. Then, Piramal Healthcare spent Rs 4,583 crore in three deals to acquire minority stakes in Shriram Capital, the holding company of Chennai-based Shriram group, Shriram Transport Finance and Shriram City Union Finance. The deals made him the chairman of the group.

Piramal's investment binge is backed by substantial growth in the company's and his personal wealth (through dividends). Piramal Healthcare netted Rs 15,000 crore from Abbott in four years after taxes and dividends, another Rs 3,037 crore from Vodafone's entry and exit, Rs 600 crore from sale of his diagnostics business to SRL Ranbaxy, and another Rs 756 crore in net profits in the past five years. The sale proceeds, dividends and his personal wealth now add up to a mind-boggling investible corpus of Rs 23,500 crore.

Method in the Madness

It is hard to digest that his shrewd business brain didn't see an opportunity in sunrise sectors such as power, renewables, infrastructure or defence, which are all drawing large corporate houses in droves.

After all, Piramal has always kept economics above emotions, listening to his mind rather than his heart. Five years before he exited Piramal Healthcare, in 2005, he divested his inheritance Morarjee Gokuldas Spinning & Weaving Mills, India's oldest surviving composite mill, at a time when organised mills were closing down mainly due to trade union strikes. In 2010, he divested his pathology lab chain to SRL Ranbaxy for Rs 600 crore, citing lack of big growth prospects. In 2015, he discontinued drug discovery research, which his scientist-wife and Vice Chairman of the Group Swati Piramal passionately spearheaded for 15 years. In 2016, he sold off BST CarGel, a cartilage regeneration product developed for global markets. Next, he could sell off the loss-making imaging business.

But Piramal sees future for a business only if it has the potential to generate revenue growth in excess of 20 per cent a year and profit growth in excess of 20-30 per cent. Almost all his acquisitions were brands or companies owned by MNCs, in which investments - hence, growth - had come to a standstill. Like Nicholas Laboratories, he acquired them, invested in them, grew them to unlock value, and then sold them at the right time and price to jump into another business.

He chose to put money in unheard of businesses - such as acquiring healthcare information management (IM) firm Decision Resources Group (DRG) of the US for $635 million (Rs 3,906 crore) in 2012 and Bayer's molecular diagnostic or imaging business. Meanwhile, Piramal Healthcare became Piramal Enterprises (PEL) and part of the money was invested in an unrelated area - financial services - by floating an NBFC to fund infrastructure and real estate sectors.

The Contrarian

Ajay Piramal has the knack of making 'abnormal returns' through abnormal risks. "We have always been contrarian. That is why we did not invest in infrastructure when everybody was investing. Nobody was investing in the US when we did. That is a judgement call and till now it has been proved right," says Piramal.

Having taken over as chairman of the group in 1984 at the young age of 29 following the sudden demise of his eldest brother Ashok and his father's death two years earlier, he turned around Morarjee Gokuldas Spinning & Weaving Mills in two years and divested it in 2005 as part of a family asset split.

His entry into pharma was also at the right time in 1988, when MNC drug companies were exiting India, and domestic companies were reluctant to buy their assets due to high overheads and costs. Piramal bought the Austrian MNC Nicholas Laboratories' Indian arm for just Rs 16 crore, ignoring expert advice not to do so. At that time, Nicholas was ranked 48th in the Indian pharma industry. A decade later, it was in the top five and by 2010, the third largest in domestic formulations business. He sold that business at a time when Indian pharma was projected to grow at a rate of 15-16 per cent a year (which now is in single digits for many leading companies).

F for Financial Services

Shriram-Piramal Financial Services will be the pivot around which the finance business will revolve. While Piramal is into wholesale lending, Shriram has an extensive retail lending network across India with 60,000 employees in 3,000 offices and Rs 90,000 crore of assets under management (AUM). "We have various options available; it all depends on what the Shriram board decides and what we decide. We see them as a long-term partner," says Piramal. Having started with a loan book of Rs 13,000 crore at Piramal Finance, the combined loan book of Shriram City Union (which operates in microfinance, gold and two-wheeler loans with disbursements of Rs 19,576 crore by March 2016) and Piramal will be over Rs 33,000 crore. Shriram Transport, Indias largest vehicle financier, has over Rs 72,760 crore AUM.

Realty Play

Jijina says that the entry into construction finance helped them scale up; it now accounts for 42 per cent of the loan book (as of March 16). Adds Piramal: "We financed (ranging) from land acquisition to construction finance and sometimes equity. And often, we do the last stage apartment funding. We have the whole project in control. Secondly, we fund only the top developers."

These projects are likely to be completed in four to five years, says Anand Piramal, who got a big boost last year when Goldman Sachs and Warburg Pincus invested Rs 2,760 crore in Piramal Realty, the biggest real estate PE funding in India.

Meanwhile, Ajay Piramal is planning to extend the business to other areas of real estate lending, besides floating a distressed assets fund with a foreign partner. It recently launched Piramal India Resurgent Fund with a corpus of Rs 6,000 crore to acquire stressed loans.

Abbott and After

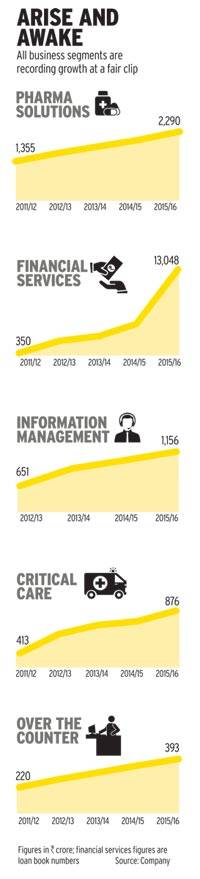

PEL now has four businesses - pharma solutions or contract manufacturing for MNC drug companies, critical care/ imaging business, OTC, and IM. From Rs 939 crore revenues in FY10, pharma solutions has grown to Rs 2,290 in FY16. It was struggling for a few years prior to FY10, but capacity was ramped up with acquisitions, debottlenecking and capacity expansion. "More than the acquisitions and capacity expansions, we focused on quality and customer partnership, which helped us grow better than the industry," says Vivek Sharma, Chief Executive Officer, Pharma Solutions of PEL.

Piramal aims to grow pharma solutions 15-20 per cent every year, which is double of industry predictions. The global contract (bio) pharma manufacturing market is predicted by market research firm Visiongain to reach $79.24 billion by 2019.

Critical Care, or inhalation anaesthetics, is headed by Piramal's son-in-law Peter De Young. The global market for this is valued at around $1.2 billion and Piramal is already among the top three companies in the field after US-based AbbVie (formerly part of Abbott) and Baxter.

The Piramals entered this space in 2002 and revenues have grown at a CAGR of 18 per cent in the past five years to reach Rs 876 crore in FY16. Now Piramal's global market share is about 12 per cent, but it has about 30 per cent of the US business where margins are high. "We are also pursuing acquisition opportunities for faster growth," says DeYoung.

Ajay Piramal is also betting big on consumer healthcare. In 2007, Piramal Healthcare had dissolved its joint venture with Boots to float an independent OTC business, which was ranked 40 in India. In two years, it improved to 17. During the sale to Abbott, this division was retained. Thereafter, PEL did five acquisitions in OTC - contraceptive i-Pill from Cipla, skin care Caladryl from Inova Pharma, five brands in gastro care from Organon India and MSD, baby-care brand Little, and four popular brands of Pfizer including Waterbury's Compound. Now its OTC business has top-selling brands like the Rs 131-crore Saridon pain killer, Rs 50 crore i-Pill, the second largest emergency contraceptive, largest anti-allergic Caladryl and Lacto, the leading calamine lotions in India with sales of Rs 46 crore. OTC revenues also have grown from a modest Rs 124 crore in FY09 to Rs 393 crore in FY16 at a CAGR of 18 per cent.

Besides, Piramal's OTC products today reach 350,000 outlets including 220,000 chemist shops across more than 1,500 towns. "In the recent past, we have acquired many heritage brands with good potential and are re-investing to grow these brands," says Nandini Piramal, Ajay's daughter, and Executive Director of PEL.

Healthcare accounted for 80 per cent of PEL's Rs 2,009-crore revenues in 2010/11, which has fallen to 54 per cent of Rs 6,610 crore by FY16, thanks to its forays into financial services (28 per cent) and IM (18 per cent).

Time for Professionals

Critics have often attacked Piramal for his reliance on family members, rather than professionals, in running businesses. He disagrees: "No other company board can boast six Padma awardees." The PEL board includes Siddharth (Bobby) Mehta, former president and CEO of Transunion; Deepak Satwalekar, former MD and CEO of HDFC Standard Life; Blackstone senior executive Gautam Banerjee; former ICICI chairman N. Vaghul; former HUL chairman Keki Dadiseth; scientists R.A. Mashelkar and Goverdhan Mehta; and S. Ramadorai, former vice-chairman of TCS. In addition, Swati Piramal, Nandini, and Vijay Shah, who has been with the group for 25 years, are also on the board.

Following the sale of the formulations business, Ajay Piramal had formed a strategic management council (SCM) and floated a company, IndUS Growth Partners, for investing the Rs 15,000 crore in various businesses. Since the investments are now done, IndUS Growth Partners has folded into DRG, with its MD Jonathan Sandler taking over as CEO of DRG and Vivek Sharma becoming the CEO of pharma solutions business. There is Jijina, too, who has been with the group for over 14 years.

Besides, Piramal has floated independent informal boards for each business. Healthcare has a pharma operations board; real estate lending, real estate asset management, and special situation transactions have independent investment committees with experts and one or two board members. Similarly, IM has an information management board, with people like PwC Partner Ashish Dalal, former HDFC senior executive Harish Engineer, former Warburg Pincus MD Rajesh Khanna, HDFC Securities Chairman Bharat D. Shah, among others.

Shah says Piramal Glass is back on track, posting over Rs 2,000 crore revenues. Piramal says the group's expansion in India will be restricted to OTC, financial services, real estate and one more sector (cement); contract manufacturing, critical care and IM will be powered by Europe and the US. "In the past five years, we created a value of Rs 18,000 crore. From 1988, we have created value Y-o-Y of 28.5 per cent," says Piramal. "There are not many stocks in which you invested Rs 1 lakh in 1988 that gives you Rs 11 crore today."

After the sale to Abbott, Piramal had the time and resources to buy mansions, yachts or private jets. Or, hang up his boots and retire on a private island. But the youthful-at-61 Piramal believes he has a long way to go. "Our belief is to create maximum shareholder returns and in the process earn our share as the largest promoter," he says.

The only luxury he allowed himself was buying a mansion from the King of Sangli at Mahabaleshwar, which the Piramals use as their weekend getaway. He is also building a new house for himself - a four-storied bungalow - on the Worli sea face in Mumbai. Piramal Realty had acquired the plot from HUL a few years ago. Sure, the vast ballroom in the ground floor of the corporate headquarters, Piramal Towers, has been modified and a velvet room awaits his guests, but his eyes are on quadrupling the group's valuation to $20 billion in four years. Manoeuvring such a portfolio will be a herculean task. It's nothing like anything he has done before but Piramal is convinced he has found the method in the madness, even if the analysts couldn't.