The lower interest rate regime is here to stay for the time being and it brings in a lot of relief to existing home loan customers

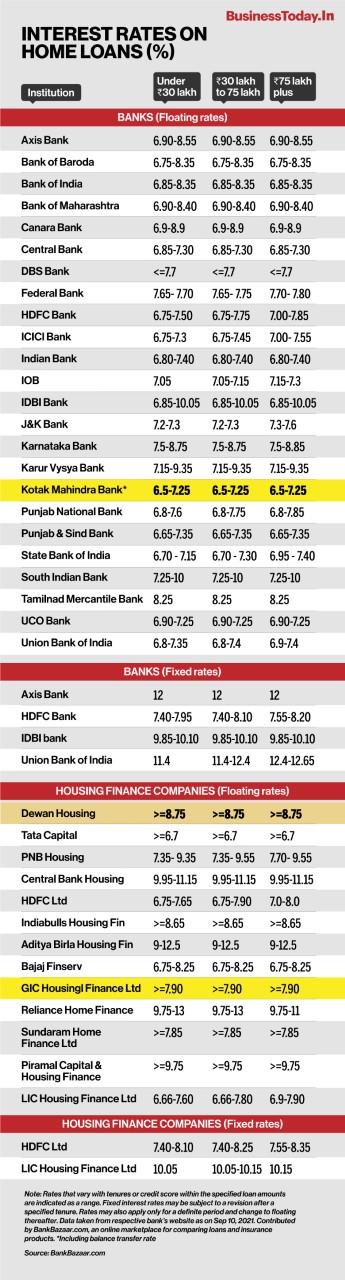

The lower interest rate regime is here to stay for the time being and it brings in a lot of relief to existing home loan customersThe COVID-19 pandemic has completely changed our traditional thinking. It has made all of us realise the importance of having our own home, especially when one considers working-from-home as the new norm across industries. The pandemic had rippling effects of softening interest rates and increased liquidity in the banking system. Kotak Mahindra Bank has recently slashed its home loan interest rates from 6.65 per cent to 6.5 per cent as a festive season offer. The reduced interest rates will be valid till November 8, 2021.

Other banks are expected to follow Kotak Mahindra Bank's footsteps as well. The lower interest rate regime is here to stay for the time being and it brings in a lot of relief to existing home loan customers.

In fact, banks across the country have steadily slashed home loan interest rates since the last quarter of 2020, passing on rate benefits to customers, which has revved up the sagging demand for housing loans. While property developers witnessed increased housing sales on the back of lower interest rates post the relaxation in the lockdown last year, people are also on the lookout for bigger homes since the home has become the centre of our lives.

Also read: India Post Payments Bank, LIC Housing Finance tie up to provide home loan products

Several other domestic top-notch commercial banks such as the State Bank of India, HDFC, ICICI Bank, Axis Bank, LIC Housing Finance, etc, among others, have slashed their home loan interest rates in 2020, with further cuts in 2021, with rates now ranging from 6.65 per cent to 6.95.

Given the current economic condition, it is best to opt for floating rates as one can take advantage of the low-interest regime. Given the liquidity in the system, home loan rates are unlikely to see a sharp rise in the near future. Of course, one can’t rule out the same later on if interest rates start increasing. Hence, existing home loan customers can take this opportunity to transfer their balance loans.

Low credit interest is an opportunity for some of the existing individuals to switch their home loans to lower rates. Lower interest rates would help existing customers in trimming their EMI outgo.

Also read: Low-cost Housing to Drive Growth

What should existing home loan borrowers do?

You should first contact your existing lender and ask for a rate concession basis your existing relationship and repayment track record. Moreover, individuals do not require documents to initiate requests with the current lender. You can contact your bank online and share your request, a little forcefully, i.e., share competitive market information. Also, if you are servicing a fixed rate variant or an old MCLR linked loan, switching to an external benchmark such as repo linked rate will cut down the rate of interest. The lender will charge a nominal fee for switching and the new rates will be assigned as per the prevailing repo linked rate. Re-negotiating with an existing lender is always the priority option.

However, if the request for rate concession has not been entertained by your existing bank, search for a suitable alternate lender. Look for post disbursement services and responsive digital customer service besides the lower interest rate. With your new lender, clearly communicate your loan terms and requirements. A fresh loan agreement will be furnished and a processing fee and administration charges will be applied. So, do the calculations first and then inform the lender about your intent, i.e., whether you are seeking EMI reduction and tenor extension, or top-up for debt consolidation, or principal reduction.

Also read: Kotak Bank cuts home loan interest rates to 6.5% ahead of festive season

Mahadev betting app case: ED arrests EBIX Chairman Vikas Garg

Mahadev betting app case: ED arrests EBIX Chairman Vikas Garg ‘Protecting a very rich portion of the world’: Trump wants to be reimbursed for guarding Hormuz

‘Protecting a very rich portion of the world’: Trump wants to be reimbursed for guarding Hormuz SBI Funds Management IPO: Should you subscribe? Check price band, issue size, GMP & more

SBI Funds Management IPO: Should you subscribe? Check price band, issue size, GMP & more Anthropic introduces India pricing for Claude AI plans; Pricing starts at…

Anthropic introduces India pricing for Claude AI plans; Pricing starts at… HCL Tech share price targets by CLSA, JPMorgan, Morgan Stanley, Citi, UBS, HSBC, Nomura, Investec, 12 others

HCL Tech share price targets by CLSA, JPMorgan, Morgan Stanley, Citi, UBS, HSBC, Nomura, Investec, 12 others Coforge, Persistent, M&M & More: Avinash Gorakshakar's Top Picks For Q1 Earnings

Coforge, Persistent, M&M & More: Avinash Gorakshakar's Top Picks For Q1 Earnings Trump Defends Iran Strikes, Says U.S. Stopped Tehran From Building Nuclear Bomb

Trump Defends Iran Strikes, Says U.S. Stopped Tehran From Building Nuclear Bomb EAM Jaishankar Launches India's UNSC Campaign: Can India Defeat OIC-Backed Tajikistan?

EAM Jaishankar Launches India's UNSC Campaign: Can India Defeat OIC-Backed Tajikistan? GoPro Mission 1 Pro Unboxing & First Look | Is This The Ultimate Cinema Action Camera?

GoPro Mission 1 Pro Unboxing & First Look | Is This The Ultimate Cinema Action Camera? Indian I.T. Stocks Face AI Disruption: Why Growth, Margins And PE Multiples May Fall

Indian I.T. Stocks Face AI Disruption: Why Growth, Margins And PE Multiples May Fall Waaree Energies stock gets downgrade from UBS; brokerage cuts rating, price target

Waaree Energies stock gets downgrade from UBS; brokerage cuts rating, price target Stock to buy: Smallcap up 85% since March 30; Investec sees 18% upside, cites 'rare combination'

Stock to buy: Smallcap up 85% since March 30; Investec sees 18% upside, cites 'rare combination' Laser Power & Infra IPO: Check allotment status, odds of getting shares, fresh GMP & more

Laser Power & Infra IPO: Check allotment status, odds of getting shares, fresh GMP & more Alpine Texworld IPO opens today: Should subscribe or avoid? Here's what analysts say

Alpine Texworld IPO opens today: Should subscribe or avoid? Here's what analysts say Concor, Welspun Corp, PDS shares rallied up to 14% today; here's why

Concor, Welspun Corp, PDS shares rallied up to 14% today; here's why