In a fast-changing digital-first world, even nostalgia has a shorter time frame. It was only a few years ago that Indians had started warming up to the idea of giving up on the age-old and unreliable cable TV connections and terrestrial TV that came with a cumbersome antenna setup, in favour of direct-to home (DTH) satellite TV service. In 2006, when Tata Sky launched its DTH service, the company had a clear motive: give Indians a taste of premium viewing with services such as 24x7 customer support, digital video recording (DVR), high-definition picture quality, etc. Today, at least for a few, even pay TV is fast becoming nostalgia because of the onslaught of OTT and a looming bugbear called DD Free Dish.

To counter that, India’s largest DTH operator, which is a joint venture between the Tata group and Sky TV (then owned by Rupert Murdoch and now owned globally by The Walt Disney Company), has donned a new name—Tata Play—and a new look. Its brand colours blue and red are now white and pink. But the brand’s basic ethos remains unchanged. “We have the same philosophy, same ethos and same obsession for the customer which is what got us here,” says Harit Nagpal, MD & CEO, Tata Play. “The only thing that changed a couple of years back was that people started watching beyond television, and we thought since we’re distributors of content, we should be medium-agnostic and become aggregators for OTT (over-the-top) content as well.” Tata Sky acted as a distributor/aggregator of just television content while Tata Play offers bundled packs where as a family, someone can watch TV content, someone can watch OTT content and someone can watch the same content on their phone. They will be billed as a family for their entertainment needs from the same vendor instead of 10 different individual subscriptions to keep track of.

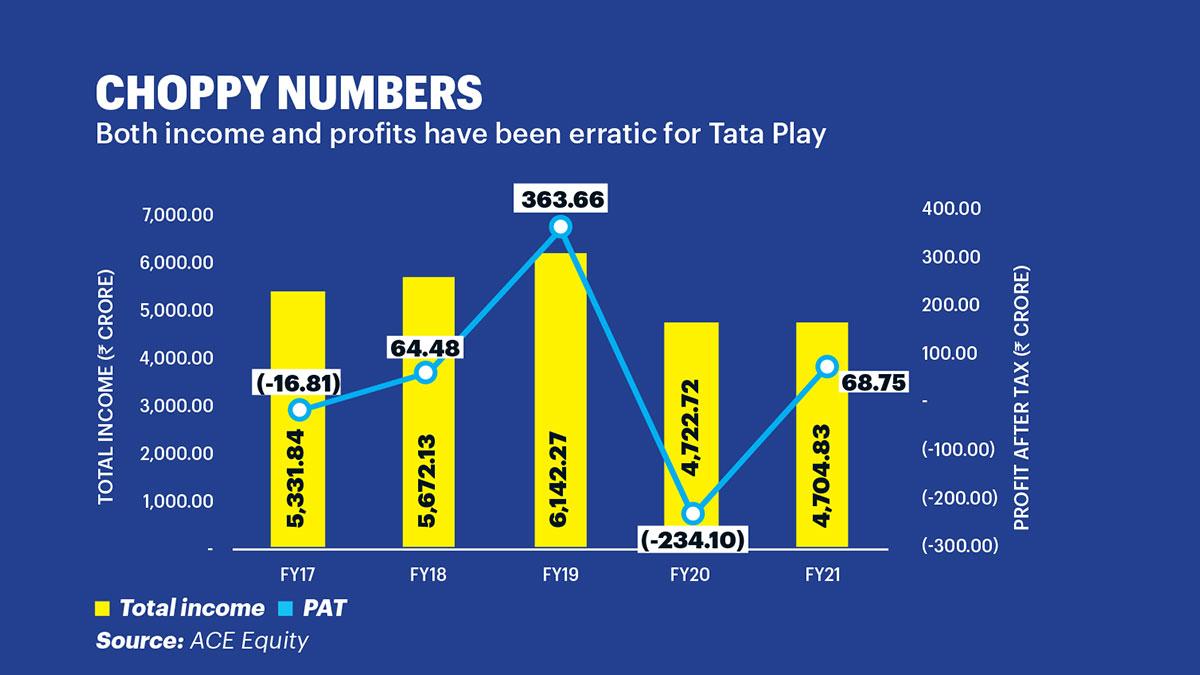

In 2019, the company made a foray into OTT with the launch of ‘Tata Sky Binge’, a platform that brings digital content from multiple apps into TV, but because of its strong DTH brand recall, people would still associate it with just TV. “We realised we needed to do a refresh for the brand so that people start believing that we’re distributors of content and not just distributors of TV content,” Nagpal explains. In FY19, the company’s consolidated profit after tax (PAT) grew 463 per cent to Rs 364 crore from Rs 64 crore in FY18. Partially offset by the pandemic, the growth couldn’t sustain for too long. In FY21, it reported Rs 69 crore PAT—marginally crossing its 2017-18 numbers. That’s why the name change was probably more survivalist than symbolic.

The free dish onslaught

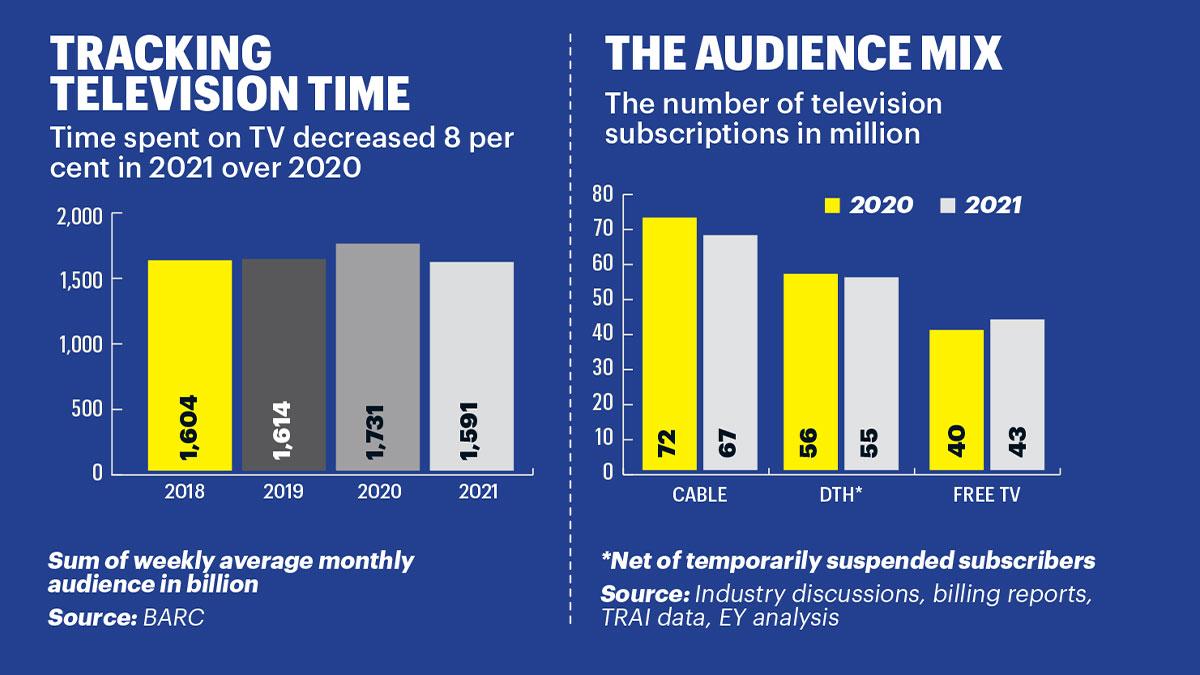

India’s DTH industry is facing a two-pronged attack from DD Free Dish on one side and OTT on the other, and the challenge is bigger from Free Dish, which is a free-to-air DTH service owned by public service broadcaster Prasar Bharati with around 52 million users in India, according to Media Partners Asia, a research, advisory and consulting firm. With more than 100 TV channels on board, Free Dish, launched in 2004, has a growing presence in rural households despite a massive shift towards online streaming platforms. During the pandemic, millions of DTH customers dropped their subscriptions. But Nagpal believes that was not because of OTT’s surge. “Our data shows that it’s not the person subscribing to Netflix who has switched off his TV subscription. Service-sector employees from villages who had lower-end plans were intermittently switching on during the pandemic to economise on their expenses,” says Nagpal.

Free Dish has long been a growth deterrent for DTH players like Tata Sky and Airtel, but many believe that it is an important tool for people at the lower end of the spectrum to start with free TV, get into the content-watching habit, and then upgrade to better quality pay TV. “There are around 125 million households that don’t even have a TV today. It’s a very nice pool for us to poach from and get 3-5 million subscribers every year. The bigger this pool gets, the better it is for us. Free-to-air does the job of making people buy TVs. It’s a step-wise transition. It’s not competition but a source of customers for us,” says Nagpal.

Utkarsh Sinha, Managing Director of advisory firm Bexley Advisors, says India is a leapfrog nation and might not evolve linearly like it’s been expected. “One of the biggest manifestations of this is in the OTT space. Given the fact that India became a mobile-first country, the entertainment wallet is limited. There are a lot of content companies vying for the same audience. Millions who still don’t have access to TV might go straight to mobile. Tata Play’s DTH and OTT bundle is good, but it totally depends on how it is priced,” says Sinha.

Tata Play offers a 50-mbps speed plan at Rs 850 per month. However, users can bring the effective price below Rs 500 per month by choosing to pay for 12 months together. Rival JioFiber, Reliance Jio’s broadband service, comes with a base plan of Rs 399 per month, which offers 30-mbps speeds with a FUP (fair usage policy) limit of up to 3.3 TB. On the other hand, Airtel’s Xstream Fiber connection offers a ‘basic’ pack of 40 mbps at Rs 499 per month.

“In the DTH business, we have a presence in 18 million homes with an ARPU (average revenue per user) of Rs 146… Free Dish continues to disrupt the business model as good content continues to be offered for free in vast waves of the country. At the same time, the irony is that the opportunity to convert and upgrade from cable is massive. There is also a huge opportunity to monetise OTT content and deliver a unified connected experience through Airtel Xstream,” Gopal Vittal, CEO, Bharti Airtel, said in a recent investor call.

According to Media Partners Asia, the growth of pay TV and DTH has been hampered by Free Dish, which is outside the purview of the New Tariff Order. No fee needs to be paid for a free-to-air (FTA) channel by a distributor such as DD Free Dish while private DTH operators have to pay maximum retail price to the broadcasters to distribute these channels to subscribers. DTH players have called it discriminatory and unfair.

“We’re not questioning licence fees. We’re basically asking not to tax a technology if a cable operator is distributing the same technology at the same price with the same margin. Regulated by the same regulator, why am I paying 8 per cent and he’s paying zero per cent?” asks Nagpal. Mihir Shah, Vice President, Media Partners Asia, agrees. “Over the years, migration of increasing number of pay channels to FTA has strengthened the consumer proposition of Free Dish, making it challenging for private DPOs (distribution platform operators) to grow at the same pace,” he says, adding that the biggest challenge for DTH is the regulation itself. “There has to be a level playing field on regulations for traditional and new alternative modes of video distribution.”

Television still rules

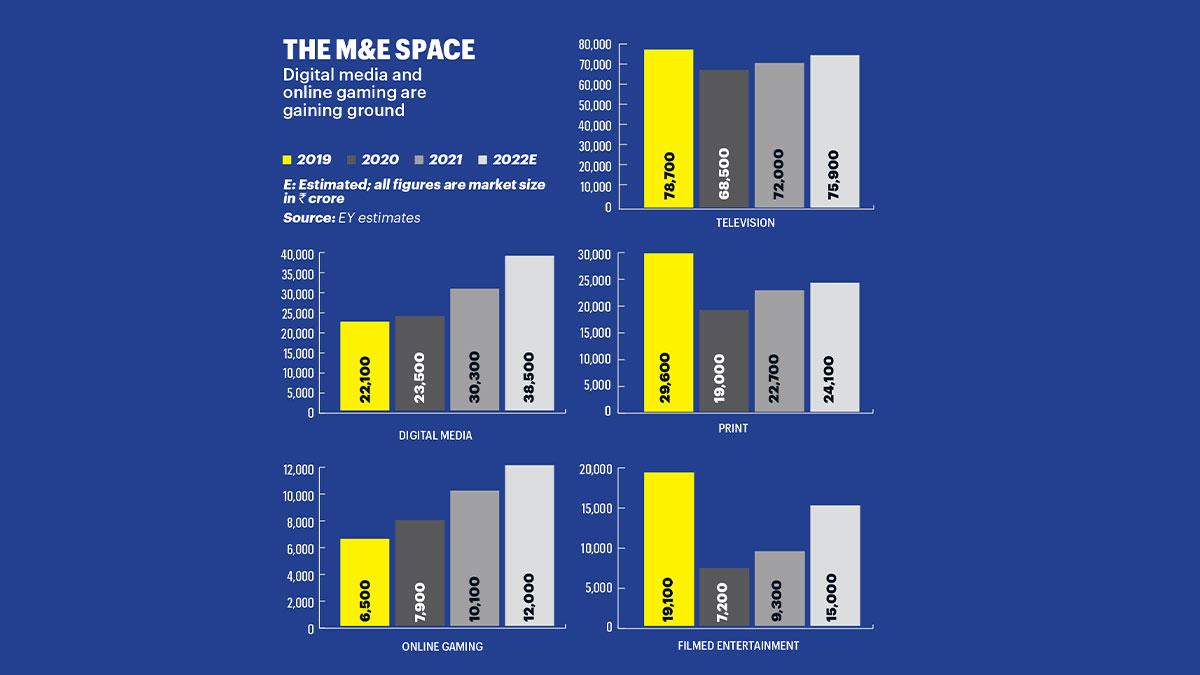

According to IBEF (Indian Brand Equity Foundation), television is one of the largest and fastest-growing segments. In 2020, the television market size stood at Rs 77,800 crore ($10.66 billion) and is estimated to stand at Rs 76,900 crore ($10.53 billion) by 2022. India’s television industry still has 120 million paying subscribers including cable, and players such as Tata Play are banking on nearly half of those who pay for cable TV to upgrade to pay TV at some point. “TV is not a written off industry. It’s our bread and butter. TV and OTT are the two industries that will grow. That’s why we’re distributors of both,” says Nagpal.

According to a recent report by CII-BCG, India grew to 70-80 million paid subscribers of OTT platforms at the end of 2021 from just 0.5 million in 2014-15. During the pandemic, OTT became the online avenue for new movie releases and the industry has seen a 4x jump in the number of OTT services in the past six years.

Seeing the massive growth potential of the OTT industry, Tata Play, which is known to be one of the first to introduce innovations like Hindi language EPG (electronic programme guide), DVRs, HD STBs (set-top boxes), etc., sees a customer need while growing its current business as a result of the spillover from Free Dish and cable TV users. “Our differentiation is not on pricing but on process. We won’t throw apps at people. When people sit down to watch TV, they don’t watch to watch Hotstar, or Zee5 or [Amazon] Prime [Video]. They’re looking for content in a particular genre or a show that everybody’s talking about,” says Nagpal.

Tata Play took two years to build a front end that allows users to differentiate based on tastes rather than platforms. Nagpal is targeting this new offering towards families. “The household subscribes for TV like it subscribes to electricity. Now, when one person has started watching OTT, why should that subscription be individual?” he argues. “You have only one electricity connection in the house. You don’t pay by room. Then why should content not be a shared cost for the family?” he asks.

Tata Play wants to turn an STB into an OTT box. “Tata is well-positioned to compete in that space. As far as entertainment consumption goes, the next generation will be cord-cutters. But there’s a lot of life left in TV especially because news is such a big deal in India. That’s the biggest thing that keeps DTH sticky,” says Sinha of Bexley Advisors.

The Indian market has four major pay DTH providers—Videocon d2h, Tata Play, Airtel, and Sun Direct. According to a FICCI-EY report, pay TV will continue to grow as states such as Uttar Pradesh, Bihar, Rajasthan and West Bengal get electrified. However, more new users will enter the free TV market as the Free Dish channel count increases to around 200 by 2022 (from 164 in 2021), providing a low-cost advertising opportunity to marketers, despite the decision of large broadcasters to take their content off the platform in February 2022.

Tata Play’s closest competitor, Airtel, also offers the Xstream Premium box with over 5,000 pre-loaded apps at Rs 4,798. While large telecom companies like Jio have launched a similar product portfolio at a much more aggressive price point, players like Tata Play and Airtel have used product innovation such as bundling OTT with television to differentiate themselves. “These product innovations will not only keep churn under check but also enable the platforms to expand their ARPU in the long run. Tata Play caters to those discerning urban audiences who want to watch the best of both worlds,” says Shah.

He believes that India might skip the multi-TV stage that was seen in several mature markets. “Several developed markets had the time to evolve and see the growth and maturity of pay TV. While India just attained its TV digitalisation objectives, the simultaneous mobile data boom in the country will make it skip the multi-TV monetisation phase. Today 95 per cent of the homes in India are single TV. Many members of the family may prefer moving to mobile or tablets for more personalised viewing,” says Shah.

He argues that Tata Play’s new proposition will work well in urban centres with many of them adopting connected TV solutions. Many of these DTH players that aim for growth from multiple streams see India more like a continent than a country. “There are many Indias within India. Thus, for a national player, you need to have horses for courses catering to varied audience cohorts having a wide range of viewing preferences,” adds Shah.

The India way

India is at about 55 per cent TV household penetration versus the Asian average of around 85 per cent. With the western markets such as the UK and the US having had a good breathing time for TV to evolve, Indian media are at different stages of evolution, affordability, and consumer choice, where every form of media seems to be growing manifold. KPMG says DTH broadcasting accounts for 37 per cent of the total television subscribers in India and is estimated at approximately Rs 22,000 crore ($3 billion) in 2020-21 as against 34 per cent in 2018-19.

Even digital subscriptions, on the back of growing user adoption, continued to rise strongly at 47 per cent in 2020-21, although there was some resistance due to the combined factors of OTT video players increasing their package prices and the sales impact of a slowing economy, according to a KPMG report.

Experts point out that since India has been at the rock bottom in terms of data pricing and internet bandwidth costs, Tata Play’s aggregated proposition will make much more sense in the OTT market as it matures further.

But why launch now? “We’ve realised that there’s a need in the market. How many subscriptions will people keep a tab on? There’s a need gap,” Nagpal says.

He makes his point on the viability of multiple media in a unique way. “The purpose of any transport mechanism is to transfer you from point A to B. Now, convenience costs more money. TV is like the bus or the train. It’s by appointment. OTT is like the car. Just because a car has been invented doesn’t mean people will stop travelling on buses or trains,” he says.

Well said, but over time, whether or not the cars outpace the trains and buses because of their convenience, remains to be seen.

@PLidhoo