You are young and healthy. You do not worry about the future. You like splurging and partying. You want to spend today than save for tomorrow. After all, who knows what future has in store for us. It's all fine until you realise one day that retirement is not far and you need to start saving for it.

You sit with your financial planner. He discusses your goals and advises you to start saving at least 80 per cent of your salary to maintain your current lifestyle after retirement. You are in for a shock. Saving 80 per cent salary looks impossible at this stage as you also have to pay your children's college fees.

ALSO READ: Five advantages of investing through systematic investment plans

You realise how saving even small amounts during earlier years could have made your future comfortable. There is no harm in living life to the fullest. But by starting saving at an early age, no matter how small the amounts are, you can definitely take off the pressure when you are close to retirement.

ALSO READ: 7 things to know about money before you turn 30

Let's assume you want Rs 1 crore when you retire. You can reach the target by investing just Rs 2,000 every month, provided you start saving at 25 and manage to earn 12% returns. Now, let's see what happens if you start at 45. To reach Rs 1 crore in 15 years, you will have to save at least Rs 21,000 every month.

ALSO READ: Go direct & online to buy a Mutual fund

We tell you the most common money mistakes people commit when they are young.

ALSO READ: Planning to buy an expensive phone or car on EMI? This is how you can get trapped

1. NOT STARTING SIP

Ruhi Tewari, 30, started investing in a systematic investment plan (SIP) of a mutual fund five years ago. She invested Rs 2,000 every month for three years. She stopped after this but did not take out the money. One day her agent informed her that the investment of Rs 72,000 over three years had grown to Rs 1.8 lakh. "I had causally started the SIP on advice of one of my friends. I was surprised to fi nd that my money grew at such a fast rate," she says.

Today, Ruhi has two more SIPs that help her take advantage of rupee cost averaging (you buy at market highs as well as lows, averaging out your risk as well as returns). She acknowledges that since the amounts get invested automatically at fixed intervals, the chances of continuing the investment for a longer period are higher. SIP enables you to invest in a disciplined manner.

There are, however, a few things you need to keep in mind while designing a SIP portfolio. First, decide the asset allocation, that is, how much money will go into what kinds funds. There are basically three types of funds - large-cap, small/mid-cap, and debt funds. Srikanth Meenakshi, Founder and Director, fundsIndia.com, says, "A typical allocation would be 50 per cent in large-cap funds, 20-30 per cent in small & mid-cap funds, and the rest in debt funds."

Second, decide the number of schemes in the portfolio. Avoid clutter. According to experts, a portfolio should ideally have three-five schemes. It is important to know that there are times when a SIP investment could disappoint. SIPs tend to underperform in a consistently rising market.

Consider the period from 2004 to 2008, when the Nifty moved up from 2,000 to 6,000. Had you invested Rs 5,000 every month from January 2004 to December 2007, your investment would have been worth Rs 5.75 lakh. In comparison, if you had invested Rs 2.4 lakh (Rs 5,000x48 months) as a lump sum in January 2004, your money would have grown to Rs 7.8 lakh. However, in 2008, when the Nifty fell from 6,000 to 2,500 levels, a lump-sum investor would have lost a lot more money than a SIP investor. Another advantage of SIP is that one does not have to time the market.

2. NOT OPENING A PPF ACCOUNT

Public Provident Fund, or PPF, is one of the best retirement tools. It gives triple tax benefits. First, you can claim deduction under Section 80C for contributions. Second, the interest income is tax-free. Third, the lump sum received at the end of the tenure is also tax-free. There is no other financial instrument, except the employee provident fund, or EPF, that gives all these benefits. It currently offers an interest rate of 8.7 per cent.

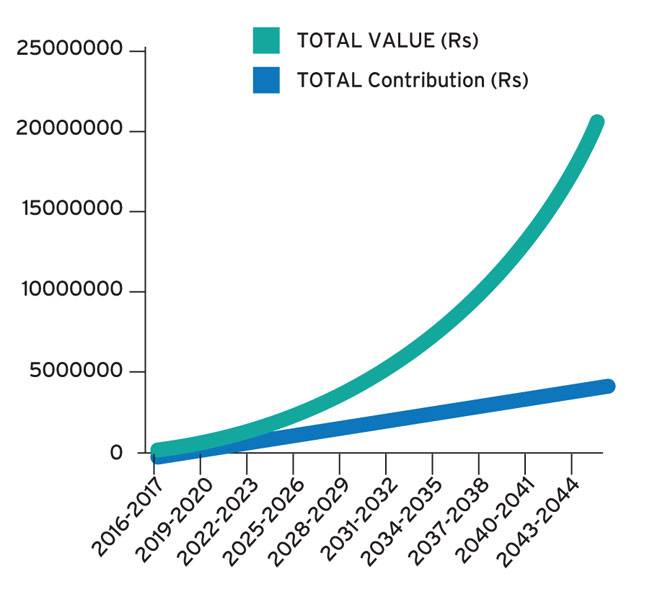

The maximum investment is Rs 1.5 lakh in a year. By investing Rs 1.5 lakh every year, you can save Rs 46.75 lakh over a period of 15 years. In 30 years, the corpus will grow to Rs 2.10 crore (See graphic). One of the best things about PPF is that the account can be continued after 15 years till you apply for closure. You can apply for a five-year extension by submitting a letter within one year of maturity. You are free to apply for as many extensions as you want.

You can also use the PPF account to create a regular stream of income after retirement as after completing 15 years you are free to withdraw every year. The best part is that this income is not taxable. There are, however, a few points to remember. You can open an account with Rs 5 but have to deposit at least Rs 500 in a financial year. The account also gives you liquidity options as withdrawal is permissible every year from the 7th financial year from the year the account is opened. A loan facility is also available from the 3rd financial year. So, don't wait, open a PPF account as soon as possible.

3. NOT BUYING TERM INSURANCE

If you have dependents, buy a term plan immediately. It is the cheapest life cover. For example, a cover of Rs 1 crore for a 25-year-old is available for Rs 8,000-10,000 a year. Other policies such as unit-linked and endowment that combine life cover and investment involve charges such as premium allocation and policy administration fees, making them costlier than pure term plans. However, in term plans, you do not get anything on maturity.

You pay premiums so that if something happens to you the insurance company pays the pre-determined sum to your family. So, while term plans provide pure protection at a very low cost, endowment plans and investment plans are basically investment avenues. But the question is, when to buy the cover? Naval Goel, Founder and Chief Executive Officer, PolicyX.com, an insurance comparison portal, says, "Generally, a person should buy a term plan at the age of 25, which is when he starts earning.

The ideal term should be 60, which is retirement age in most cases, minus the current age." At 35, when the person is earning more, he can buy an extra cover. But which insurer should one choose? "You will be shocked to know that the premium for a similar plan, for the same sum assured, everything else such as smoking habits and age being the same, varies from Rs 5,000 to Rs 15,000 per year. That is kind of difference we are looking at. So, you can easily save up to 50 per cent on your premium if you compare plans from different com

4. NOT BUYING HEALTH INSURANCE

A sudden hospitalisation can wipe out your savings in a single blow. Medical inflation is rising faster than general inflation at 15 per cent. Advanced technology and super-specialty hospitals have also made medical care expensive like never before. Experts say the trend is likely to continue in the foreseeable future. While costs have been rising steadily, health covers are inadequate. A lot of people who have full-time jobs appear to believe that the coverage provided by their employers is enough and doesn't need to be supplemented.

BigDecisions.com, a platform for personal finance advice, recently released its 2015 health research report that said 95 per cent middle-class Indians do not have enough insurance to cover some of the most common ailments.

Surprisingly, those above 45, who are at a higher risk of health problems and closer to retirement, are least prepared for emergencies as they are underinsured by 69 per cent on an average.

Manish Shah, Co-Founder and CEO, BigDecisions, says, "While it is no surprise that typical treatment costs in the US are sometimes more than 10 times higher than those in India, they are more than twice as much in countries closer home such as Malaysia and Thailand. This means Indians could soon be paying more." The report says consumers are paying large sums out of pocket as a result of being under-insured. So, it is advisable to buy health insurance at a young age when premium is low. Decide the cover by looking at the size of your family, lifestyle and medical costs in your city.

5. NOT UNDERSTANDING POWER OF COMPOUNDING

We keep delaying investing thinking it won't affect us much. This is a costly mistake. Experts say compounding grows your money much more as you earn further interest on your interest income.

Consider this: If you invest Rs 5,000 every month for 15 years your saving of Rs 9 lakh will be Rs 20 lakh at the end of the tenure assuming returns of 10 per cent. So, invest for the long term to get the benefits of compounding.

6. WRONG INVESTMENTS

We do not ask our agents the right questions at the time of investing and repent when we get to know about the high costs (such as fund management fee and agent's commission) of the products he has sold us. For every 1 per cent extra cost you end up losing Rs 3.5 lakh on an investment of Rs 10 lakh over 30 years. It is, therefore, imperative to ask the right questions at the right time.

Many people put money in savings accounts thinking that the 4 per cent return would be enough for all future needs. This could be one of your costliest mistakes as such a low return would not be able to beat inflation. Once you are convinced about investing, the next step is choosing the product.

At this stage, most people are confused between equities and real estate. History proves that equities have outsmarted real estate over long periods.

Surya Bhatia, a New-Delhi based financial planner, says what happens in real estate eventually is that your property worth Rs 1 crore rises by 10 times. But one must look at the IRR, which is what really matters. "So, a rise of 10 times over 20 years means just 14-15 per cent returns a year. Equities, on the other hand, have given a tax free return of 17-18 per cent over long periods. That 17 per cent is tax-free while the 14 per cent is taxable. Plus, there is convenience, transparency and liquidity. A property that has gone down in value is not liquid and will not find buyers. Keeping in mind these challenges, equity has a stronger case."

8. WITHDRAWING FROM EPF

Most of us withdraw EPF money with every job change. Companies also many times advise employees to withdraw the balance because of the long time and procedure involved in transferring money from one company to another. Well, with the government issuing universal account numbers, or UANs, to all EPF subscribers, this should not be a problem for you and your company. Unlike previously, now your PF number does not change with the change of job. The UAN is a 12-digit number allotted to each member. It has done away with the need to transfer funds. All you have to do is furnish your UAN and KYC details to the new employer.

Once the new employer verifies these, the money from the older account will get transferred to the new account. But for accounts opened before the allotment of UAN, you still have to apply either online or offline. It is a big step towards shifting EPF services online and making them more user-friendly. EPF is designed to provide financial security after retirement. It is a very useful instrument for retirement planning.

9. NOT CHANGING OLD HABITS

You should adapt new technologies to save time as well as money. For example, online insurance plans are much cheaper than the offline policies. Similarly, you can buy mutual funds online, saving money that would have otherwise gone to the agent as commission.

Similarly, you can earn reward points on bill payments through mobile wallets, which you can redeem on your next purchase. Mobile wallets work like electronic prepaid cards and can be used to pay for things from grocery to rail tickets without the need for swiping debit/credit cards. All you have to do is key in the username and password at the time of transaction. You can then load the wallet with money either through debit or credit card or net banking. After this, you can use it to transfer money, pay bills, book tickets and shop.

10. TAKING ON DEBT

Be careful while taking loans. Do not owe more than what you can pay. If you have an existing debt, pay it first. Get rid of loans on which the rate is the highest. Another reason to pay on time is that this affects your credit score. A low credit score can hit your eligibility for loans. If there is any amount outstanding against your name get rid of it immediately.

It doesn't matter how small the amount is. Always maintain the required balance in your bank account, particularly when an EMI is due. Unpaid loans affect your credit score badly.

11. IGNORING INFLATION

Assuming inflation at 7 per cent, Rs 1,00,000 today will be worth just Rs 13,000 after 30 years. This means that things will get costlier and you will be able to purchase less with the same amount of money. You need to plan your investments in such a manner that you beat inflation during pre- and post-retirement years.

Nilesh Shah, Managing Director, Kotak Mutual fund, says, "If we see the historical range of inflation, it's been 7-8 per cent a year. However, all of us want to live a better life. So, we need to provide for 10-12 per cent inflation, which takes care of one, nominal inflation, and second a little bit of upgrade, which we all as individuals desire. You need to generate returns of 12-14 per cent per annum so that we can take care of inflation as well as the upgrade." Do follow the above-mentioned advise for a happy financial life.