Retail investors have been flocking to mutual funds, especially equity funds, over the past two-three years. This is thanks partly to campaigns such as Mutual Fund Sahi Hai by the Association of Mutual Funds in India or AMFI. Their preferred route has been systematic investment plans or SIPs. "Between April 2016 - when AMFI started disclosing monthly SIP contributions - and June 2019, the route helped rake in a whopping Rs 2.3 lakh crore. That is nearly 19 per cent of the Rs 11.9 lakh crore increase in assets under management (AUM) of the industry," says a Crisil-AMFI report.

"The surge has come on the back of scores of new retail investors joining the ranks, too, as reflected in the almost 3x growth in the number of SIP accounts to 27.3 million from 10 million over this period," says the report.

However, SIP registrations have slowed down this year. AMFI data shows that last year, monthly SIP investments grew 16 per cent between April and September from Rs 6,690 crore to Rs 7,985 crore, while in 2019, the growth during the period was a marginal 0.30 per cent. This can be partially due to the performance of equity markets. Equity markets have been range-bound over the past two years.

This has hit the enthusiasm of investors. The average return given by diversified funds in the year to September 30, 2019, was around 4 per cent. The large-cap funds gave 6 per cent while the small-cap funds returned minus 3 per cent. However, a few funds have done exceptionally well. Axis Small Cap fund delivered 18 per cent. The second best performing fund in the category, ICICI Prudential Smallcap, returned 8.30 per cent.

The best large-cap fund, Axis Bluechip, gave 17 per cent. In the diversified category, multi-cap funds delivered the best performance, albeit by a small margin. The category average return was around 6 per cent. The best performing fund, IIFL Focused Equity, delivered around 20 per cent.

Passive Investing

Equity funds have lagged their benchmarks in the recent past. Ninety per cent large-cap funds underperformed the S&P BSE Sensex Total Return Index in one year to September 30. This has again ignited the debate whether passive investing - where a fund follows an index and so fund management costs are minuscule - is better than active investing. So far, in India, equity funds meant only active funds. As active funds have lagged their benchmarks over the past couple of years, a section of investors has started questioning the need to pay extra to fund managers. In fact, in the large-cap category, two of the five funds that have delivered the highest SIP returns over five years are index funds or exchange traded funds.

Experts say this is due to the uneven market rally in which only a few stocks have risen and say that this is only a short-term trend. "One of the key factors responsible for shrinking alpha in the short term, especially in actively managed equity funds, is the polarisation seen in the recent market rally. However, we are of the view that this is not a permanent phenomenon, as this was seen in 1999 and 2007 also. We believe that the alpha created by active funds is likely to return once this polarisation subsides," says Nimesh Shah, MD & CEO, ICICI Prudential AMC.

However, Radhika Gupta, CEO, Edelweiss AMC, says it will be difficult for large-cap funds to generate alpha due to structural changes. The Securities and Exchange Board of India, or Sebi, has standardised definitions of equity and debt mutual funds across categories. This has left no scope for funds to deviate from their mandate even slightly in order to generate alpha. For example, large-cap funds can invest only in top 100 stocks by market capitalisation. "Structurally, active fund management will find it difficult to generate alpha, but there will be years where there is no alpha generation and years which will compensate and see good alpha generation. Multicap, midcap and smallcap spaces will continue to generate healthy alpha in coming years," she says.

Also, equity funds are now benchmarked against the total return index, whose returns are higher than the standalone index. So, their performance may look less attractive compared with what the benchmarks have delivered.

Recovery in Sight?

The sluggish market performance is in line with the current economic slowdown. Indias GDP grew 5 per cent in the June quarter, the lowest in over six years. The government has implemented a number of reforms to revive the economy such as reducing the corporate tax rate. Stock markets rose sharply after the announcements. Experts say they may recover in the medium to long term on the basis of earnings growth and add the government needs to carry out reforms that increase consumption demand.

"Stock markets have responded positively to big announcements such as tax cuts but sustainable earnings growth is a key driver for markets. They are still waiting for clarity on this front. Earnings growth is a function of economic growth and recovery of the economy is taking time. Though recent initiatives will help revive investments over the medium term, the markets are waiting for more steps from the government to revive consumption and address liquidity issues arising out of the NBFC crisis. On the consumption side, the government has to do a tough job of striking a balance between fiscal discipline and ensuring that people have more disposable incomes," says Srinivas Rao Ravuri, CIO-Equity, PGIM India Mutual Fund.

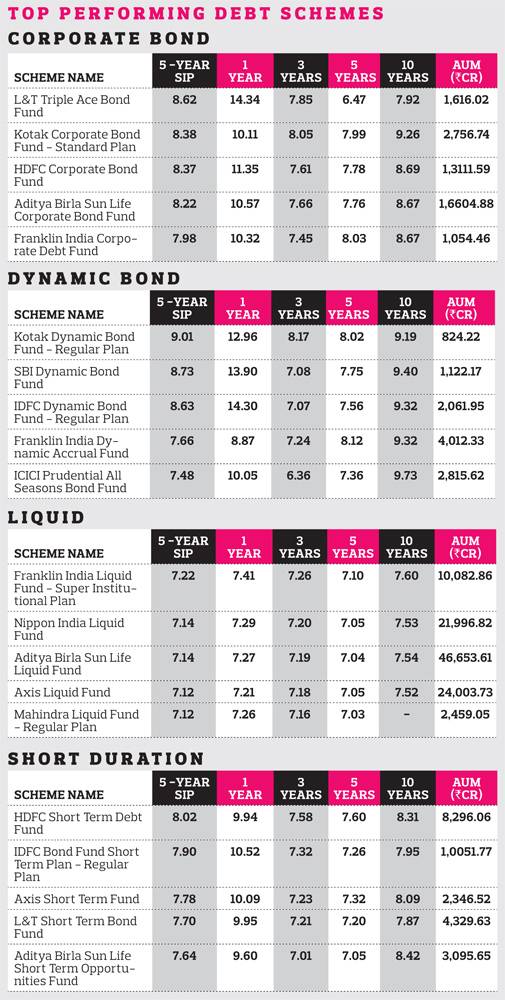

Debt Fund Fiasco

Debt funds were considered less risky than equity funds till last year when IL&FS defaulted on loans. This led to a liquidity crisis with people avoiding debt papers fearing more defaults and downgrades and a consequent fall in NAVs of debt funds. Fund houses had to resort to desperate measures such as allowing only part redemption in fixed maturity plans and rollovers and unilateral agreements with promoters to not sell pledged shares for some time. For investors, the experience of the past few months has been shocking.

Should one write off debt funds completely?: The developments highlighted the inherent risk in debt funds, including credit risk and interest rate risk, which investors need to be aware of. Credit risk is the risk of default while interest rate risk is the risk of fall in prices of debt papers due to change in interest rates. Credit risk can be managed by owning a diversified portfolio and investing in higher rated papers but can't be avoided. "It's hard to say if all the troubles are behind us but it seems that most large stressed assets are known. That is not to say that newer names can't come to light but they could be potentially smaller in the overall scheme of things," says Kaustubh Belapurkar, Director Manager Research, Morningstar Investment Adviser India.

However, the debt defaults and fall in NAVs of debt funds have been a lesson for both investors and fund houses. "The biggest outcome of the crisis is better focus on risk management and portfolio diversification. These events have highlighted that just as volatility is an integral part of equity investments, rating upgrades and downgrades are part and parcel of credit investments," says Nimesh Shah.

Regulations Tightened: Sebi has brought in a series of regulations to make debt funds more transparent and less risky. Among other things, it has allowed mutual funds to do side pocketing in case a debt asset falls below investment grade. This allows funds to segregate good and bad investments. The investors are issued units of both the portfolio. This helps investors benefit from any future recovery and doesn't impact the rest of the portfolio. Also, Sebi has asked debt funds to mark-to-market debt instruments with maturity over 30 days.

Till now, instruments with maturity up to 60 days were valued on an amortisation basis. Under this, the difference in the price of the debt instrument at the time of purchase and redemption is spread evenly across the tenure of the paper. This results in a linear increase in the NAV of the fund and makes it less volatile. "Mark-to-market will ensure that bonds are always fairly valued. It will ensure that investors get a fair NAV," says Kaustubh Belapurkar of Morningstar India.

Sebi has also brought in graded exit load for liquid mutual funds. Now, exit load will start at between 0.0070 and 0.0045 per cent up to the first six days, reducing by .0005 by every day. This means those investing for one-two days will shift to overnight funds. "Money being invested in liquid funds for less than seven days can move to overnight funds and other options. Liquid funds will continue to get money for greater than seven days but liquid funds' AUM volatility will come down," says Kaustubh.

Liquid funds have also been asked to hold at least 20 per cent assets in cash and receivables or government securities to ensure liquidity. Sebi has also capped exposure of debt funds to unlisted non-convertible debenture at 10 per cent and unrated debt papers at 5 per cent; earlier, the cap was 25 per cent.

What Should Investors Do

Debt funds carry risk and there is nothing called a guaranteed return. In order to avoid a negative surprise, investors should make an informed decision. "They should be aware of the duration risk (volatility risk) and credit risk (default risk) in debt funds. The longer the portfolio maturity, the higher is the duration risk. The better a portfolios credit rating (AAA / A1+), the lower is the credit risk. Investors should be aware of the risks," says Joydeep Sen, Founder, Wiseinvestor.in. "They should choose fund categories that match their risk profile and investment horizon," says Kaustubh.

Still, debt funds have the potential to deliver better returns than bank fixed deposits, especially in a falling interest rate scenario when fixed deposits may not be the best choice. Long-term debt funds have delivered double-digit returns this year as the RBI cut interest rates by 135 basis points (100 basis points is equal to one per cent). They are also more tax efficient due to indexation benefit if you remain invested for more than three years. This significantly reduces the tax liability.

On the equity front, stay invested and continue with SIPs to benefit from volatility (a depressed market means a lower NAV, which means you will get more units). Stick to your asset allocation. "It is important to stay invested not only in equity but also in debt. Within equity, if an investor is ready to stay put for over five years, he can consider investing in mid-caps and small-caps and value and multi-caps in a systematic manner. This is because of the relative attractive valuations in these pockets," says Nimesh Shah of ICICI Prudential AMC.