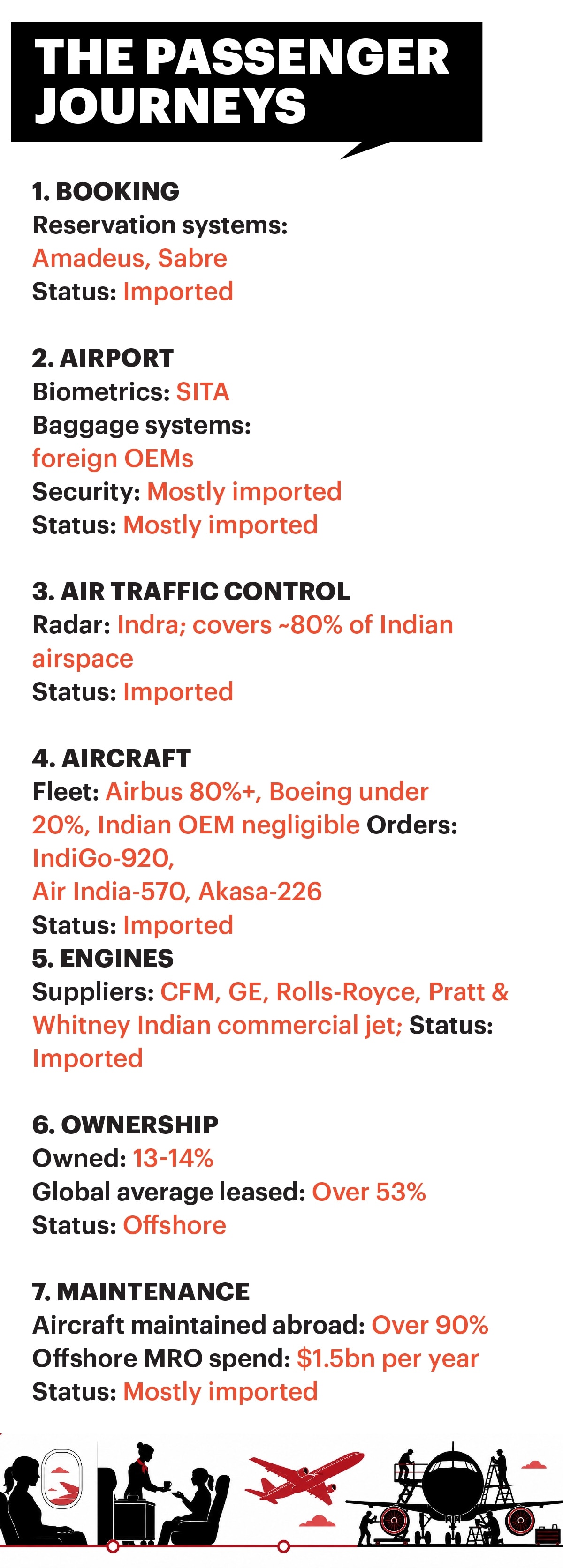

Walk into any Indian airport, and the baggage carousels you see are equipped with foreign-built systems. The Spanish company, Indra Sistemas, operates the radars that guide aircraft through India’s airspace. The biometric gate scanners are from a Swiss firm called SITA. The ticket that brought the passenger here was sold through either Amadeus, headquartered in Spain, or Sabre, incorporated in Texas.

It’s ironic that none of these products is made in India despite the fact that the components, engineering, and design used in these products are regularly outsourced to Indian manufacturers. No Indian-made aircraft serves mainstream commercial fleets either.

The contrast is clear. While Indian civil aviation is galloping and is now the world’s third-largest market, with 4.2% of global air traffic originating from India, according to the International Air Transport Association, very few aviation equipment items are manufactured here, even as Indian firms now build complex aerostructures and components for almost every Airbus and Boeing platform.

ICRA projects that on a combined basis, Indian carriers will serve between 210 and 215 million passengers this financial year. Each year, the expansion of the fleets continues apace. In 2023, Indian airlines had placed orders for 1,100 aircraft. Within two years, according to a reply in the Rajya Sabha in July 2025, the order book had swelled to around 2,026 aircraft, all from three domestic carriers, namely Air India Group, IndiGo, and Akasa Air.

The Imported Aircraft

The numbers are real. The growth is real. And nearly none of the infrastructure driving that growth is Indian.

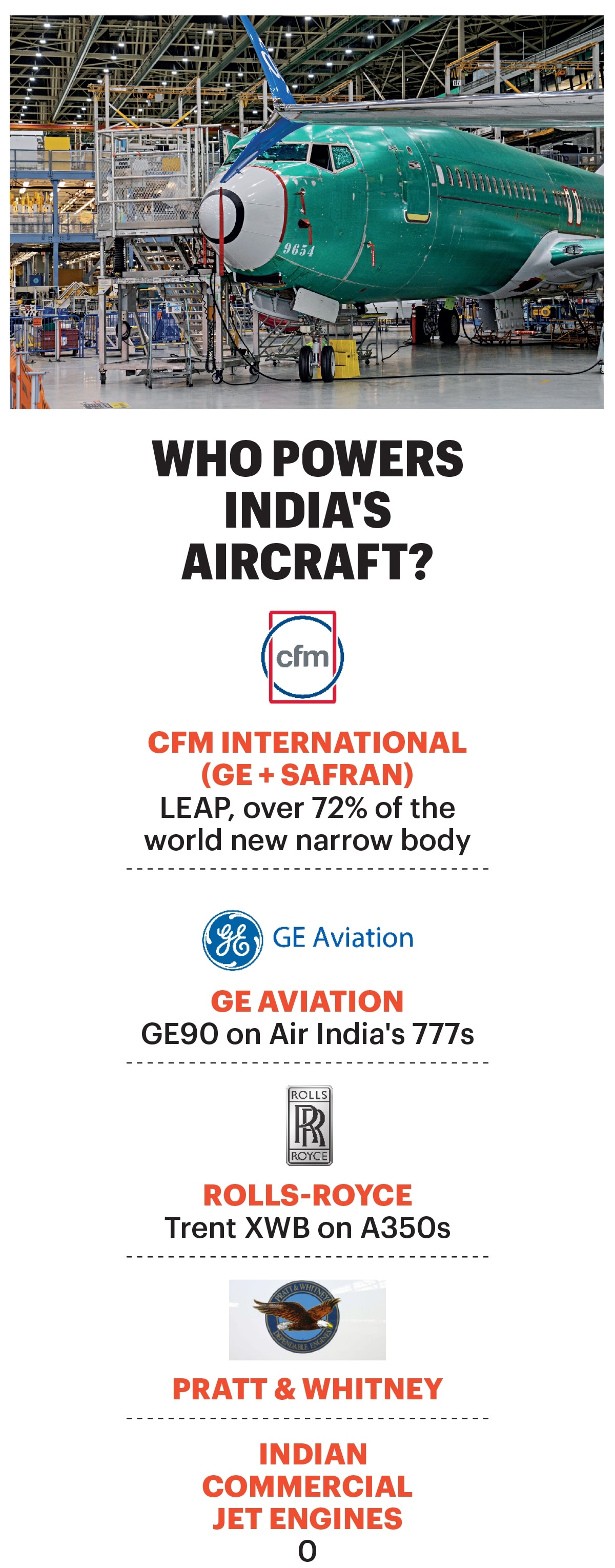

Every narrow-body—the backbone of Indian aviation—is either an Airbus A320 family jet that is built at assembly plants in in Toulouse, Hamburg, or Tianjin, or a Boeing 737 MAX assembled in Renton, Washington. Airbus accounts for more than 80% of the domestic Indian market by seats. IndiGo, which handles 61.9% of all domestic passengers, operates a fleet that is predominantly Airbus. Nearly 90% of Air India’s long-haul capacity is supplied by Boeing. This concentration locks Indian carriers into foreign maintenance, spare-part, pilot-training, and software ecosystems for decades.

Arvind Melligeri, the Executive Chairman and CEO of Aequs, a Belagavi-based maker of aerospace products for both Boeing and Airbus, and the operator of India’s first Aerospace SEZ , understands the architecture from inside. “It is worth noting that globally, the sector is dominated by a few players, irrespective of the segment. For instance, while there may be 26 airframers on paper, the reality is a duopoly, with Airbus and Boeing accounting for 88% of the market. In aircraft manufacturing, there is a reason only a few major players exist. Making aeroplanes is highly complex, with development timelines stretching up to 15 years and platform lifecycles exceeding 20 years. New programmes are therefore rare, even if multiple concepts exist on drawing boards,” says Melligeri.

No aviation economy, however large, is fully self-contained. Even the United States and Europe depend on globally distributed supply chains for engines, avionics, materials, and components. Airbus sources extensively outside Europe, while Boeing’s supplier ecosystem spans multiple continents. The question, therefore, is not whether India should be dependent—aviation by design is interdependent—but where it sits in that chain and how much of the value, technology, and strategic control it owns.

Group Captain Venkatesh Chari (Retd), Assistant Vice President (Operations), HoD & SME (Aviation Safety & Quality) at Laminaar Aviation Infotech, who has analysed India’s aerospace dependency in depth, identifies the material constraints that underpin this reality. "India currently lacks adequate expertise in manufacturing aerospace-grade materials — especially titanium and aluminium superalloys, as well as advanced composite materials used in aircraft structures,” he says.

He explains that these materials require high precision, quality control, and specialised industrial ecosystems, which are still evolving domestically.

Karthik Kudkuli, Assistant Professor of Aviation and Aerospace Management at CMS Business School, JAIN (Deemed-to-be University), frames the systemic gap. According to him, India is not short of aerospace talent, but it still lacks a fully mature end-to-end aviation ecosystem. The real issue is fragmented capabilities in R&D, test infrastructure, certified suppliers, materials, and industrial coordination.

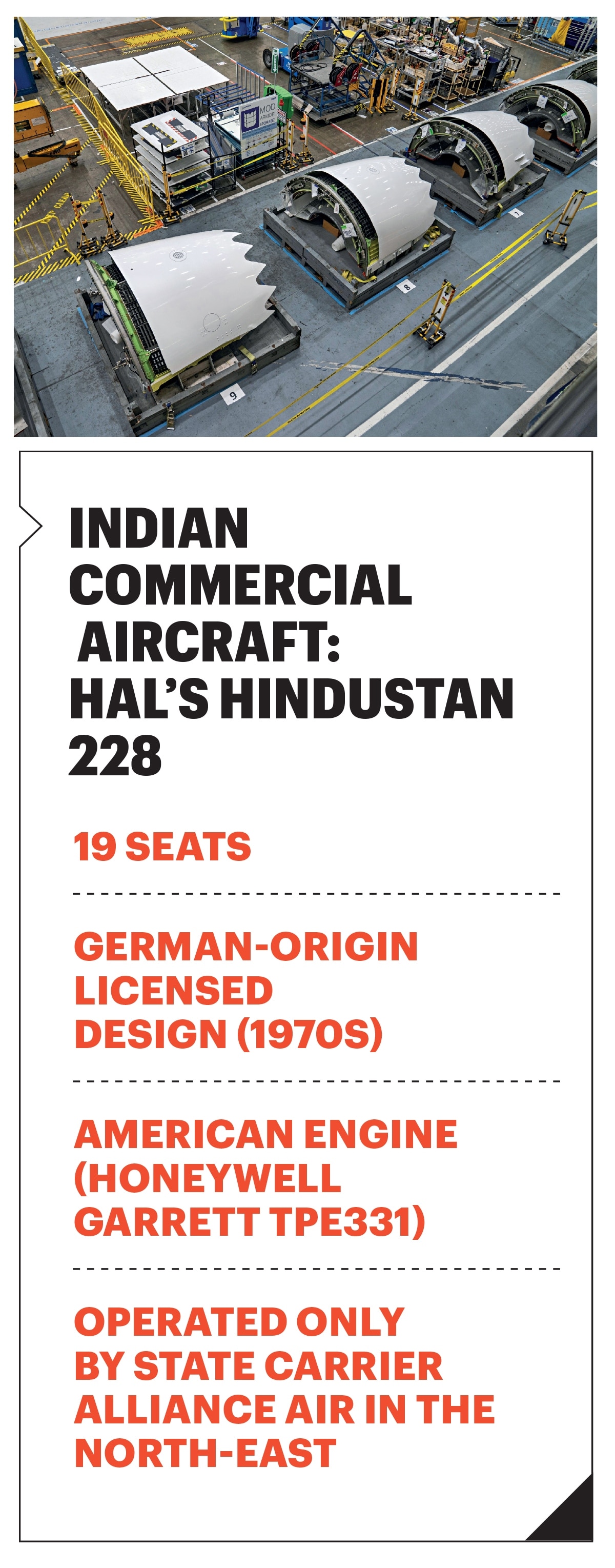

The HAL Hindustan-228 — a 19-seater turboprop certified under a licence from Germany in the 1970s — is India’s only commercially certified, domestically manufactured aircraft. The airline that operated its first scheduled commercial flight, Alliance Air, remains a state-owned regional carrier. Even the Hindustan-228’s engine is foreign: a Honeywell Garrett TPE331, designed in the United States.

A committed order book extends this import dependence for a generation. Air India has orders for 570 aircraft from Airbus and Boeing. IndiGo has 920 on order, the largest single-airline backlog in the world. Akasa Air has placed an order for 226 Boeing 737 MAXs. The three carriers’ backlogs together total roughly 1,716 aircraft with a combined discounted value of $88–107 billion, every rupee of which flows to Toulouse and Seattle.

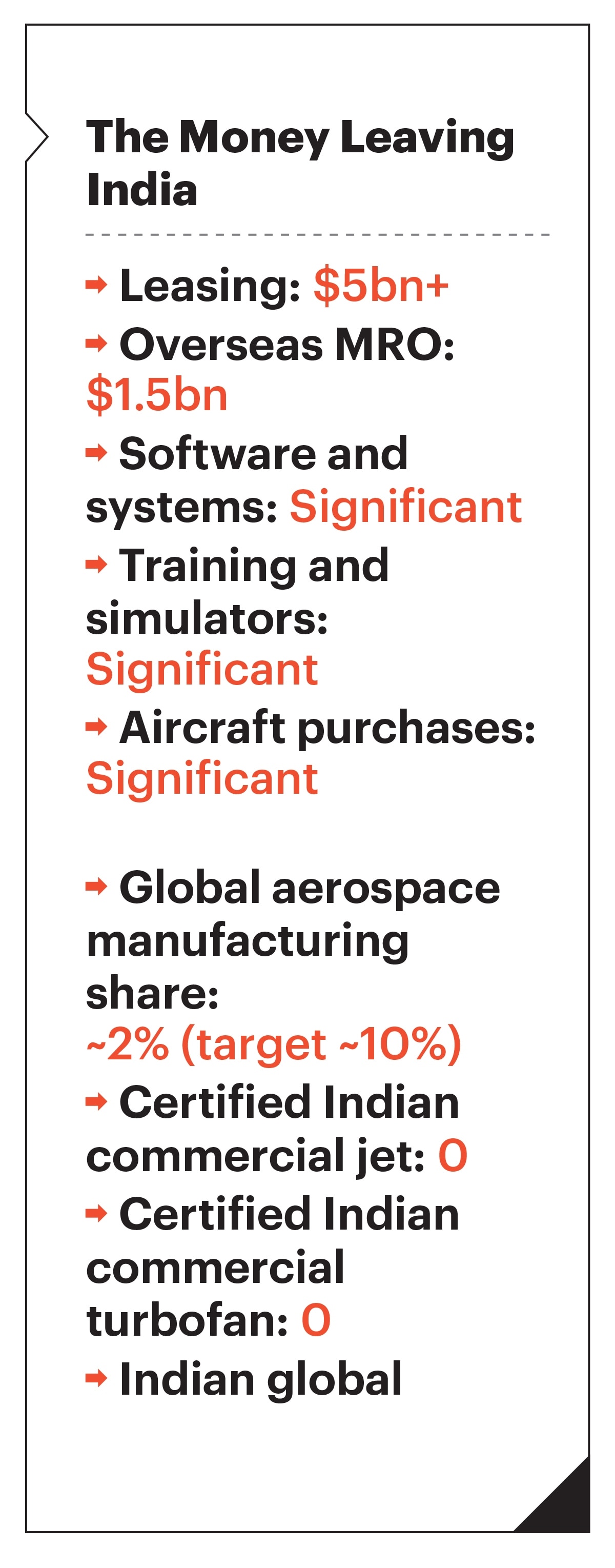

Melligeri is candid about the ceiling. “A fully indigenous aircraft is unlikely,” he says. “At best, it will be an ‘assembled in India’ aircraft with design, engines, and key systems sourced from global OEMs and partners, perhaps through joint ventures.” India currently accounts for about 2% of the global aerospace components manufacturing market, with the industry targeting a 10% share. The ambition is real. The distance is very large.

Leasing Architecture

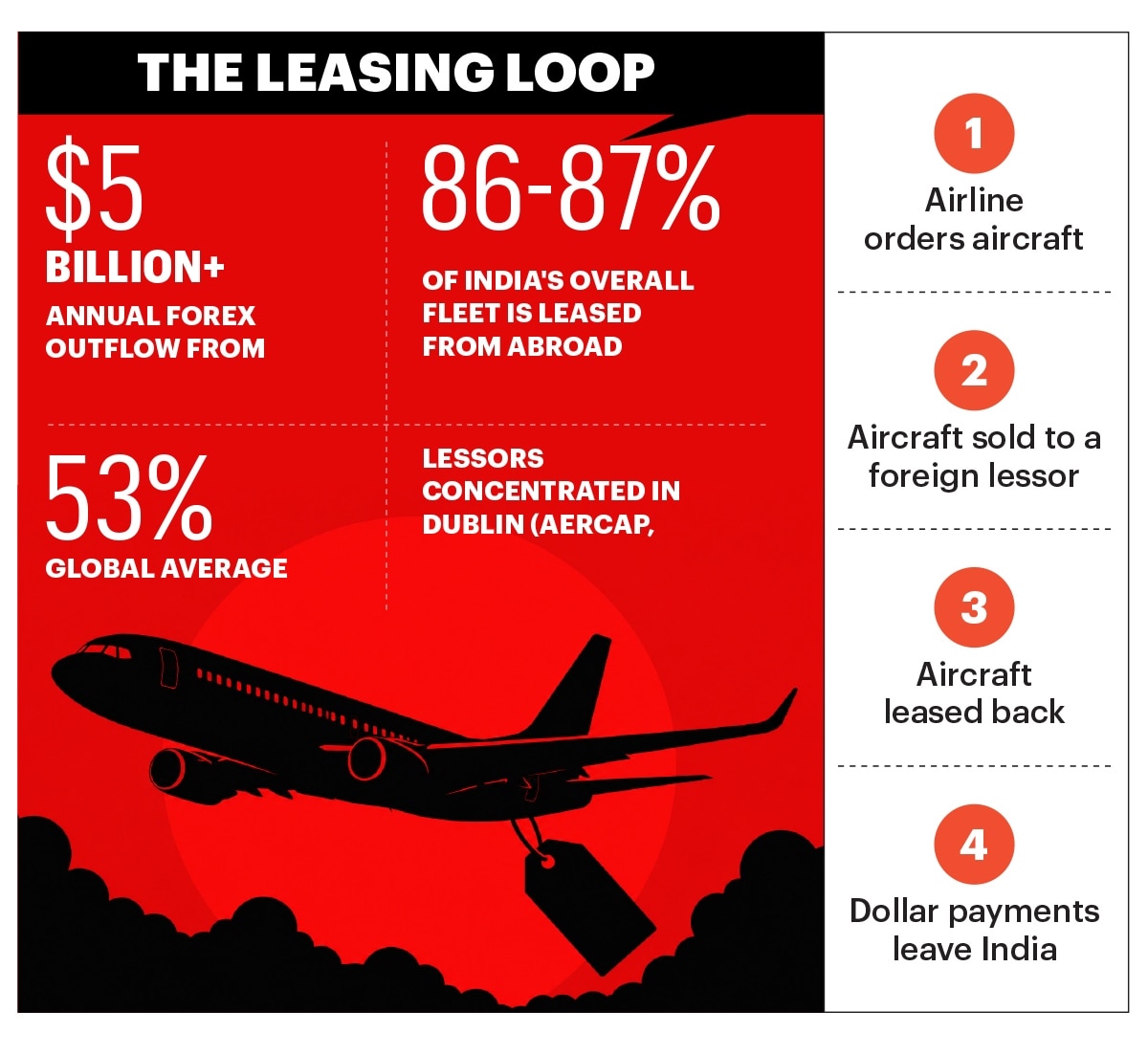

Of India's 860-plus commercial aircraft, 86–87% are leased from foreign entities—compared with a global average of around 53%. The leasing industry is concentrated in Dublin, where AerCap, the world’s largest lessor with a portfolio of 1,669 aircraft valued at nearly $62 billion, maintains its headquarters alongside Avolon and SMBC Aviation Capital. Together, these three companies controlled approximately 30% of the global commercial fleet in 2024, according to Mordor Intelligence.

The IMPRI Impact and Policy Research Institute estimates that India’s dependence on offshore leasing costs it “in excess of $5 billion annually in foreign exchange.” Group Captain Chari puts the overall industry annual forex outflow—leasing, maintenance, repair, and operations (MRO), software, parts, and pilot costs combined—at $18–20 billion. Projected lease-related outflows alone are expected to reach approximately $3.6 billion annually by 2040 as the order book converts to deliveries. These are not speculative projections. They are the contractual consequence of 2,026 aircraft already on order, almost all of which are being paid for in dollars.

When IndiGo disclosed its balance sheet as of June 2024, its capitalised operating lease liability stood at approximately $5.4 billion—owed almost entirely in US dollars. In Q2 of FY26, IndiGo posted a net loss of Rs 2,582 crore despite revenue growing by more than 10%. The airline's Chief Financial Officer Gaurav Negi, was explicit: “60% of the airline’s costs are in US dollars, including fuel and maintenance.”

A rupee depreciation of just 1.7% in that single quarter produced a foreign exchange loss amounting to Rs 2,892 crore, roughly $340 million. ICRA’s 2024 aviation industry report captured the structural exposure: “Approximately 35-50% of total airline operating expenses are denominated in dollar terms, making airlines highly vulnerable to currency depreciation.”

Airports & Boarding Gates

Adani Airport Holdings Ltd (AAHL), which operates seven of India’s major airports, has made a deliberate effort against the grain. “Adani Airports is committed to using Made in India technology and solutions wherever possible,” says an AAHL spokesperson. “We were one of the first airport operators to deploy Made in India baggage security screening machines. We have also developed an in-house automation platform — Aviio—to automate entire operations.”

It remains an exception in a landscape where the overwhelming architecture—from ATM radars to biometric boarding systems—is sourced from abroad.

M.V. Nahusharaj, former Global Head of Recruitment and Management Development with Air India, explains why the pattern of foreign dominance at ground level is not accidental. “Indian airports utilise foreign ground handlers primarily to manage rapid growth, bringing in expertise in safety and complex logistics management,” he says. According to Nahusharaj, the government also encourages foreign direct investment, and hence more services are being offered by foreign ground support companies.

The radar network overseeing aircraft through Indian airspace is the product of Indra Sistemas, a Spanish aerospace company. Its network covers 80% of India's airspace—nine Monopulse Secondary Surveillance Radars, 38 tower automation systems at 38 airports, and the two most critical Area Control Centres, Delhi and Kolkata, according to its own documentation. In March 2023, AAI awarded Indra a contract worth more than €55 million to expand its operations into Mumbai, Hyderabad, Bangalore, Navi Mumbai, and Mopa.

India’s DigiYatra biometric boarding programme operates on SITA’s Swiss face-recognition hardware, supported by an app developed in partnership with the Indian company Data Evolve. In July 2023, SITA announced a landmark agreement with the AAI covering 43 airports and more than 2,700 passenger touchpoints.

The Corner Office

The pilot shortage in India is structural. The DGCA issues 1,200 to 1,500 commercial pilot licences a year. CAPA India forecasts that the sector will require around 10,900 new pilots by 2030. In December 2024, a Ministry of Civil Aviation report submitted to the Lok Sabha showed that Indian airlines had 236 foreign pilots, a number that had tripled from 67 in March 2023. Air India Express alone accounted for 144 of these, following the induction of 35 Boeing 737 MAX aircraft, for which there were far too few Indian commanders with type ratings. The Level D Full Flight Simulators, mandatory for type ratings, are dominated by foreign manufacturers such as CAE of Canada, L3Harris of the United States, and Thales of France.

The dependency does not stop at the cockpit. It extends to the corner office. Every one of the big Indian carriers has, for the better part of three decades, had a foreign national at the helm. Pieter Elbers, a former Dutch CEO of KLM, served as the CEO of IndiGo until his resignation in March 2026, following the December crisis that led to flight cancellations. Air India has been led by Campbell Wilson, a New Zealander with 26 years at Singapore Airlines, since its privatisation; he announced his resignation in 2026, with the board yet to name a successor. IndiGo’s incoming CEO, Willie Walsh—Irish and a former British Airways chief and most recently IATA Director General—will take over in August 2026. Before Wilson, the Tatas had initially offered the Air India role to Ilker Ayci, then chairman of Turkish Airlines, who turned it down amid controversies. The historical tally runs deeper: Wolfgang Prock-Schauer of Austria led both Jet Airways and GoAir; Nikos Kardassis, a Greek American, ran Jet Airways; Cornelis Vrieswijk, a Dutchman, headed GoAir; and Phee Teik Yeoh of Singapore led Vistara.

Captain G.R. Gopinath, who founded Air Deccan, remarks that “if Indians can be CEOs of the world’s largest companies abroad, how is it that our own airlines cannot find leaders at home? The answer is that while we have thousands of pilots and aviation engineers, we simply do not have a large pool of aerospace and airline management professionals, a field that is quite complex.”

Indigenisation

To address this dependence, experts bat for building indigenous capacity. However, that does not mean that a domestic commercial aircraft would compete against the A320. Group Captain Chari points out three conditions for any significant indigenisation: a certification framework equivalent to those of the FAA and EASA; a capital financing approach that can sustain development cycles of 12 to 15 years; and a materials manufacturing ecosystem that produces aerospace-grade titanium and aluminium at scale.

If the reform efforts that began in 2020 continue, the domestic MRO share could rise from 14% to 30–40% over the next decade. Safran’s LEAP engine MRO plant in Hyderabad, likely to go live by late 2026 with a capacity of 300 engine shop visits per annum, indicates that international OEMs have begun to invest in India’s depth rather than just profit from it.

Adesh Nandal, an advocate at Jotwani Associates who advises on aviation law and policy, argues that the rebalancing is already underway. “The move to reduce GST on domestic MRO services from 18% to 5%, and to introduce a uniform IGST rate of 5% for aircraft parts and engines, is not cosmetic reform but structural,” he says. “GIFT City entities have leased hundreds of planes so far. Minimum Indian content and technology-transfer obligations can be built into next-generation airport contracts.”

India’s aviation boom looks impressive, but it relies heavily on foreign systems and equipment. Although the government and airlines are aware of this dependence, current efforts to address it are not sufficient.

India’s skies are full of aircraft, but much of the financial and strategic control behind them belongs to others.