Think of the most iconic or prominent office parks and commercial hubs across Mumbai, Bengaluru, the National Capital Region (NCR), Hyderabad, Chennai, Ahmedabad, or Kolkata, and chances are that these are run by one of the many real estate investment trusts (REITs).

REITs have emerged as key custodians of the country’s premium commercial real estate. Players such as Embassy Office, Knowledge Realty, Mindspace Business, Brookfield India, and Bagmane Prime manage some of the most prestigious and sought-after commercial real estate assets that house leading companies and businesses in the top Indian cities. Nexus Select Trust, meanwhile, mostly runs mall spaces.

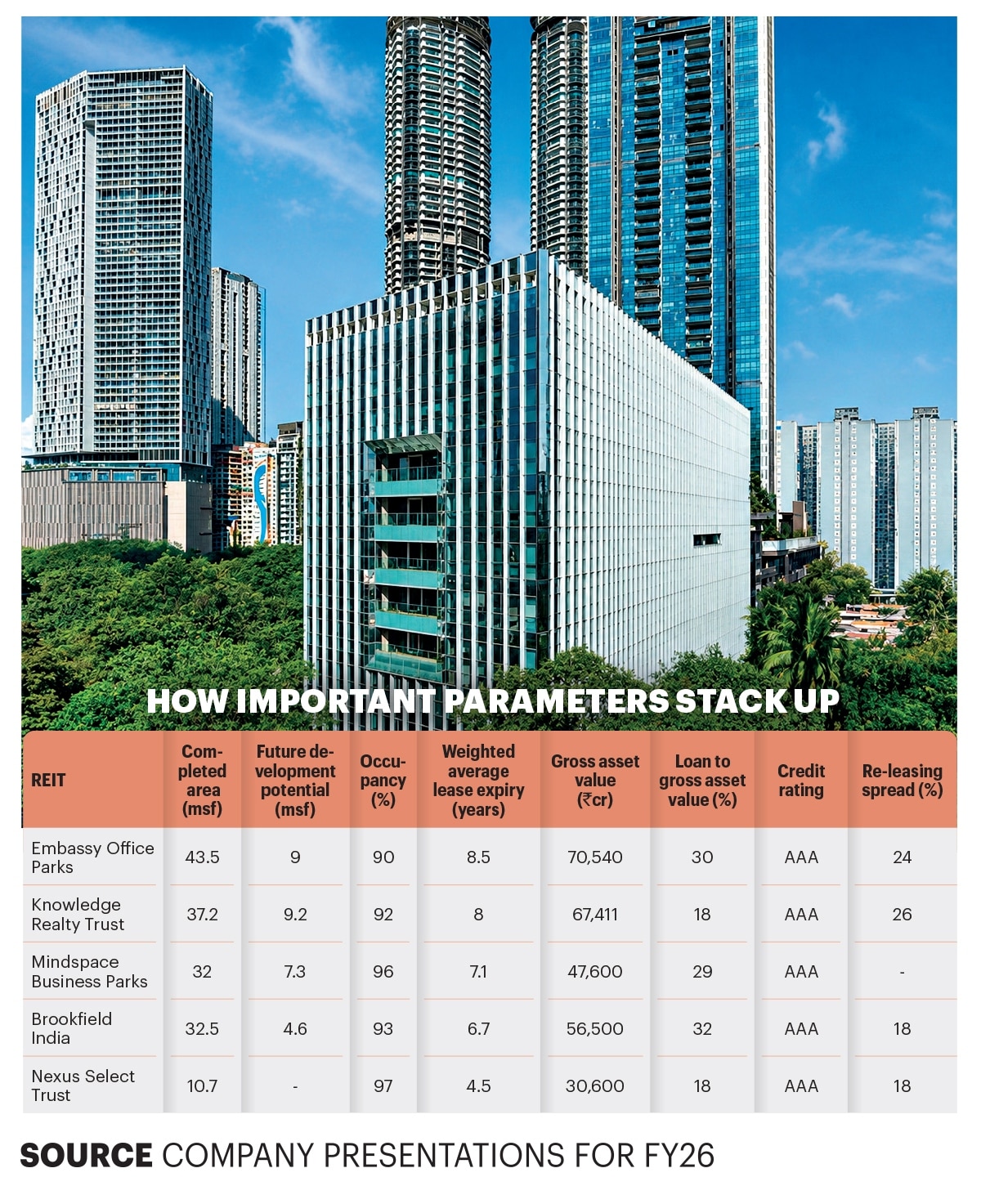

Together, India’s REITs command a gross asset value (GAV) of more than Rs 3.12 lakh crore, reflecting the combined total market value of all properties and cash assets held under their management.

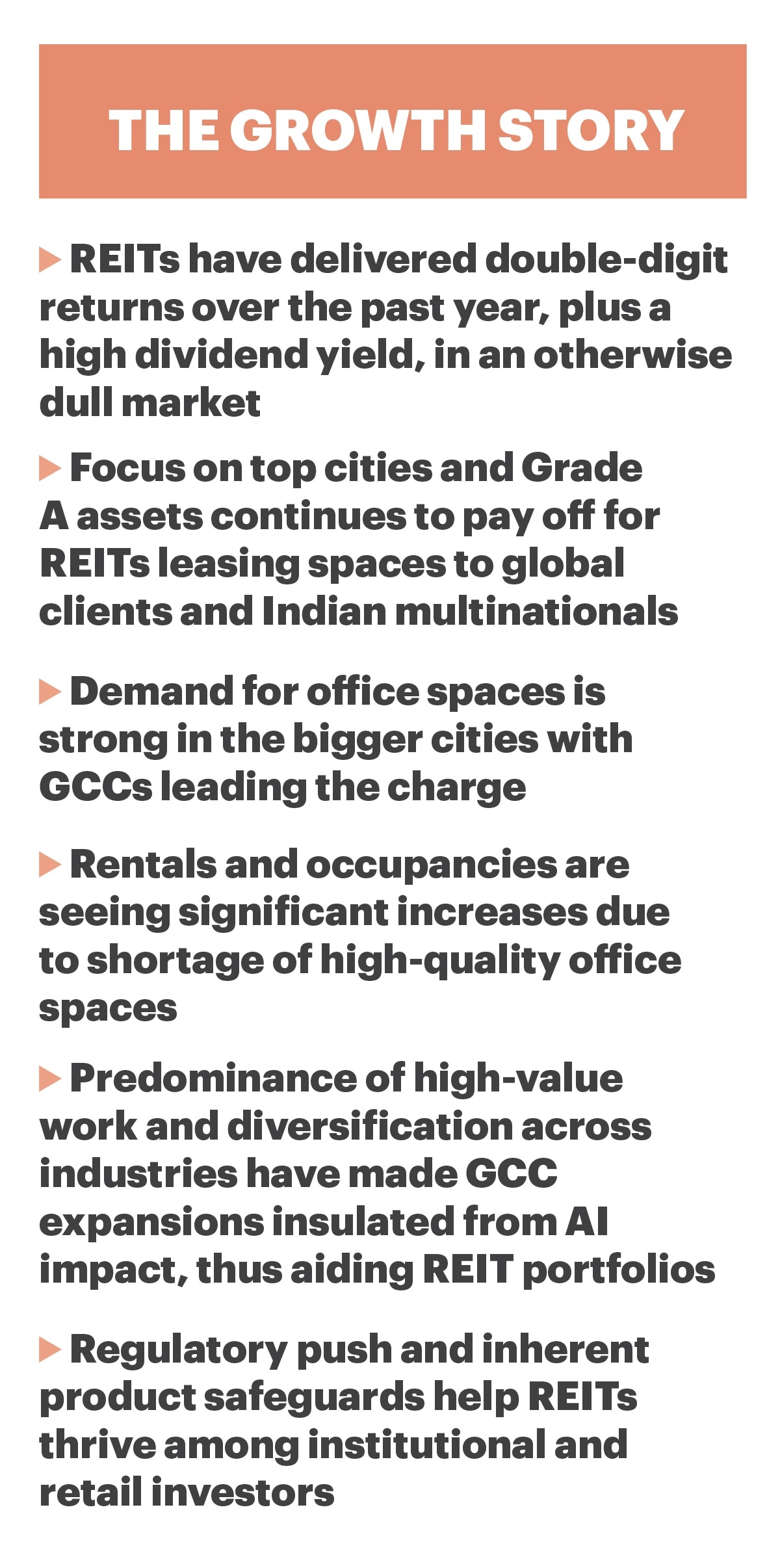

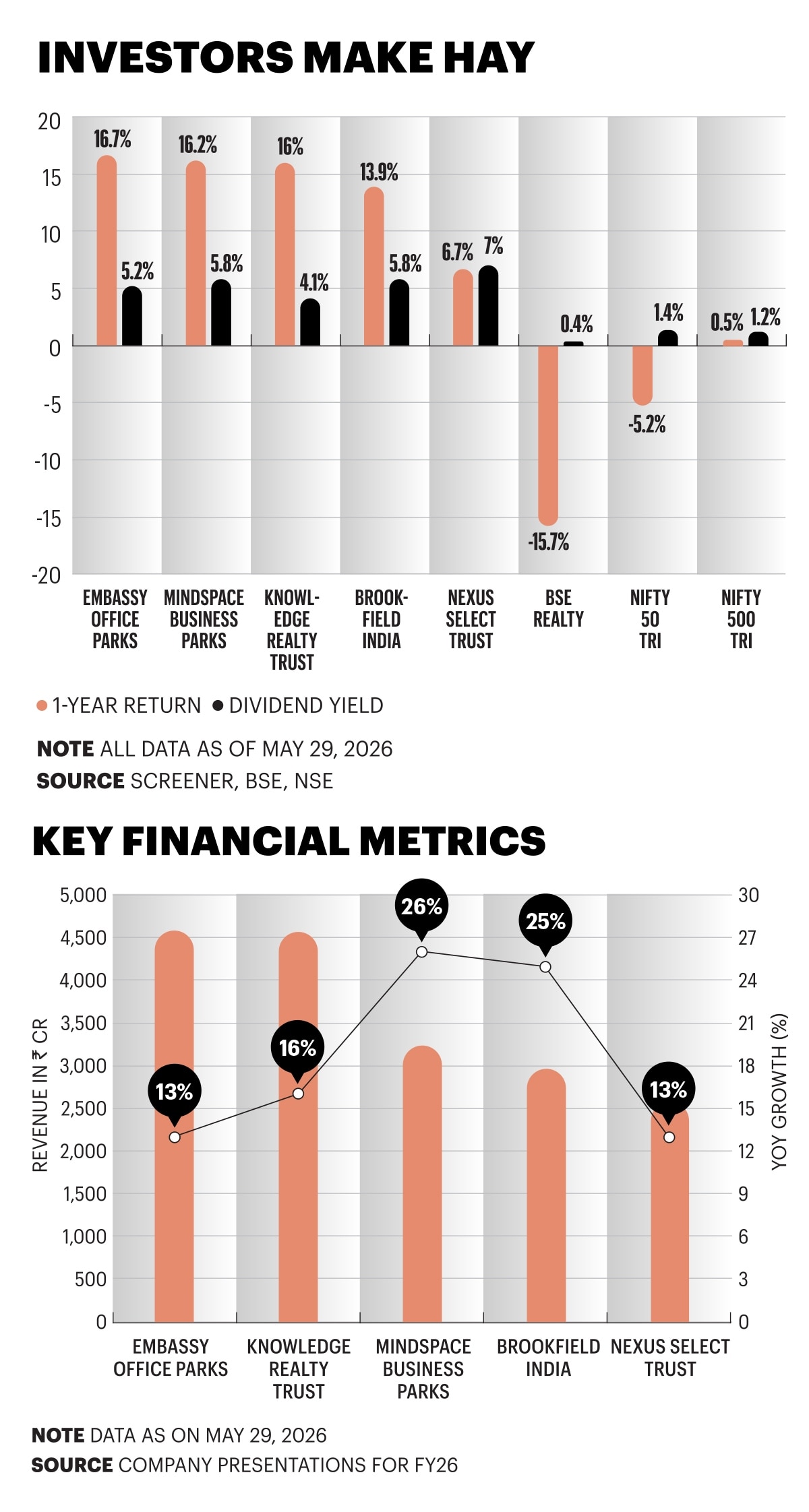

These REITs have been in the spotlight over the past year or so, with their robust showing in the markets after a three-four-year period of lull with low single-digit returns. The turnaround has been impressive, with four of the five listed REITs giving returns ranging between 13.9% and 16.2% in the last year as of May 29, 2026 (from May 29, 2025 levels). And they have topped it by dividends, with yields ranging from 4% to 7%.

The combination of capital appreciation and attractive income has brought REITs firmly back into investors’ focus, making them one of the more compelling opportunities in the market today. This has been achieved in a period during which equity markets have been turbulent and mostly on a negative trajectory, thanks to wars, penal trade tariffs, energy supply and price disruptions.

The BSE Realty index declined by over 15%, the benchmark Nifty 50 Total Return Index (TRI) fell over 5% and the broader Nifty 500 TRI was almost unchanged in the one-year timeframe mentioned earlier. And their dividend yields have been much lower.

Indian REITs now command a market capitalisation of over Rs 2.16 lakh crore. This figure includes the market capitalisation of Bagmane Prime that listed just a few weeks back. These five REITs have collectively distributed a whopping Rs 8,907 crore to the 4,25,000-unit holders in FY26 as dividends. Riding the seemingly insatiable demand for office spaces and retail outlets in malls, REITs have seen their incomes and margins expand. Regulatory support from the Securities and Exchange Board of India (Sebi) in recognising these instruments as equity-like investments, along with favourable dividend taxation and inherent safeguards of REIT structures, have significantly boosted their appeal among investors.

While the geographical tension in West Asia and business disruptions due to the rapid adoption of Artificial Intelligence (AI), particularly in the technology sector, pose certain challenges, REITs seem well-positioned to navigate these headwinds.

Priming up

REITs mainly focus on Grade A assets that are premium, usually located in prime locations or central business districts of metros, with advanced technological infrastructure and energy-efficient sustainable buildings often adhering to ESG standards. Leading domestic companies, multinational firms, technology heavyweights, and global banking and financial services majors lease spaces in these Grade A offices.

A notable trend over the past five to seven years has been the rapid expansion of Global Capability Centres (GCCs) in India. These rank among the largest occupiers of Grade A office space in the country and have emerged as a significant source of rental income for India's listed REITs.

A report from commercial real estate services and investment firm CBRE indicates that by CY2028, the gross Grade A office spaces absorption would hit 100 million sqft, while the supply is likely to be only 79 million sqft.

“The Grade A demand appears to be durable, not frothy. ANAROCK reports net absorption was 58.2 million sq ft in 2025 and rentals grew 6% to Rs 92 per sqft. At the same time, vacancy has declined to 15.5% in Q1, 2026,” says Peush Jain, Managing Director, Commercial Leasing & Advisory, ANAROCK Group.

A report by Nasscom-Zinnov predicts that the number of GCCs in India would increase from 1,700 in FY24 to 2,200 by FY30 and the market size would rise from $65 billion to $100 billion over the same period. Despite all these positive outlooks, could the disruption in businesses due to AI and potentially lower workforce intake affect demand for offices?

Ramesh Nair, CEO & MD, Mindspace REIT, does see AI affecting demand. “The AI narrative has been active for the last three years, but office demand has continued to grow during that period. We have also seen some of the companies driving AI adoption continue to take office space in India, and large IT services firms that gave up space during Covid come back and lease more space. We believe AI is more likely to accelerate the flight to quality than create broad-based office demand destruction,” says Nair.

Peush Jain of Anarock adds, “Tech layoffs should bring only limited near-term headwinds for REITs. Demand is no longer tech only, and GCCs lead India’s Grade A office market with 47% of gross leasing in Q1, 2026, up from 36% in Q4, 2024.”

Another key aspect is that many global companies are increasingly carrying out high-end work from Indian office spaces, and are not just focused on software services.

“Contrary to the fears around AI, we are seeing the work done from India go up the value chain. GCCs undertake high-end high-quality work and give us 45% of our gross rentals. Also, another 31% of our rentals come from front office assets that are client-facing. These are insulated from AI impact,” says Shirish Godbole, CEO, Knowledge Realty Trust.

The war in West Asia and spiralling energy prices, too, do not seem to have done any serious harm to occupancy and leasing decisions.

“There have been some near-term challenges. We have seen travel disruptions and airspace constraints affect transaction timelines in the market, and there are cases where occupiers have become more cautious about capex deployment or slowed decision-making. Demand fundamentals remain intact. In one case, a 200,000 sq. ft GCC requirement in Hyderabad was paused due to the war, but the same space was leased to another GCC within 15 days at a higher rental,” adds Nair.

“Office completions in Q1 2026 fell 18% YoY, partly due to disruptions linked to West Asia. This suggests occupiers and investors have largely ridden out the shock, particularly in prime stock,” adds Peush Jain.

In a recent conference call with analysts, Alok Aggarwal, CEO & MD of Brookfield REIT, said war will not impact GCC decisions to relocate to India.

While the demand for office spaces is well-established, what about mall spaces?

“Leading domestic and international brands continue to prioritise high productivity malls that offer scale, visibility and consistent consumption catchments. This is also translating into healthy leasing momentum and rental growth for quality assets, even as the broader market remains selective,” says Pratik Dantara, Head of Strategy at Nexus Select Trust.

“Organised retail continues to gain share, premiumisation trends are strengthening across categories,” says Dantara.

Catering to investors

At their core, REITs are like mutual funds in the way they function. These real estate trusts invest in rent-yielding commercial spaces. REITs usually tend to own and operate these properties via special purpose vehicles (SPVs). Each SPV that is subsidiary of a REIT tends to manage one specific property. Usually, there are several SPVs functioning under most listed REITs.

The Sebi has mandatory clauses for the functioning of REITs that act as guardrails for investors. At least 80% of the assets that a REIT owns must be invested in income-generating commercial real estate.

These entities are also expected to distribute a minimum of 90% of their net distributable cash flow (NDCF) on a quarterly or at least annual basis. NDCF is roughly the income earned via rentals, less the expenses incurred to operate the assets. Most listed REITs tend to distribute well above this limit to unitholders.

REITs also aren’t allowed to borrow beyond 49% of their GAV. Any further debt requires shareholder approval. The loans to GAV ratio is 18% to 32% for the five listed REITs as of FY26, well below the regulatory threshold. And all listed REITs have the highest ‘AAA’ credit rating.

Sebi reclassified REITs as equities with effect from January 1, 2026. They enjoy equity taxation – gains made from the sale of units held for more than one year are taxed at 12.5%. Portions of dividends paid to unitholders under certain heads, such as repayment of loan are tax-efficient. Typically, 70-90% of the dividends are tax-efficient. These are not taxed until those payouts exceed the acquisition price of the REIT.

“Sebi’s move to classify REITs can encourage participation by mutual funds and specialised investment funds, improve liquidity and deepen price discovery by bringing them closer to mainstream portfolio allocation. It also strips away the ‘alternative asset’ perception for retail investors,” says Peush Jain.

Rahul Jain, Head of Public Markets, Alt (an alternative assets investment platform) says, “This decision brings India in line with the global best practices of including REITs within equities. A few REITs already meet the criteria to be included in the Mid-cap index, Nifty 500, etc. Once included, it will also lead to inflows from passive funds and ETFs tracking these indices.”

Overall, REITs stand on a firm wicket for the foreseeable future. As a testimony to this, India’s largest value-driven mutual fund scheme with Rs 1.41 lakh crore assets under management, Parag Parikh Flexi Cap, has a solid 4.1% exposure to REITs.